Academic Profile

Statistics

Similar Authors

Papers on arXiv

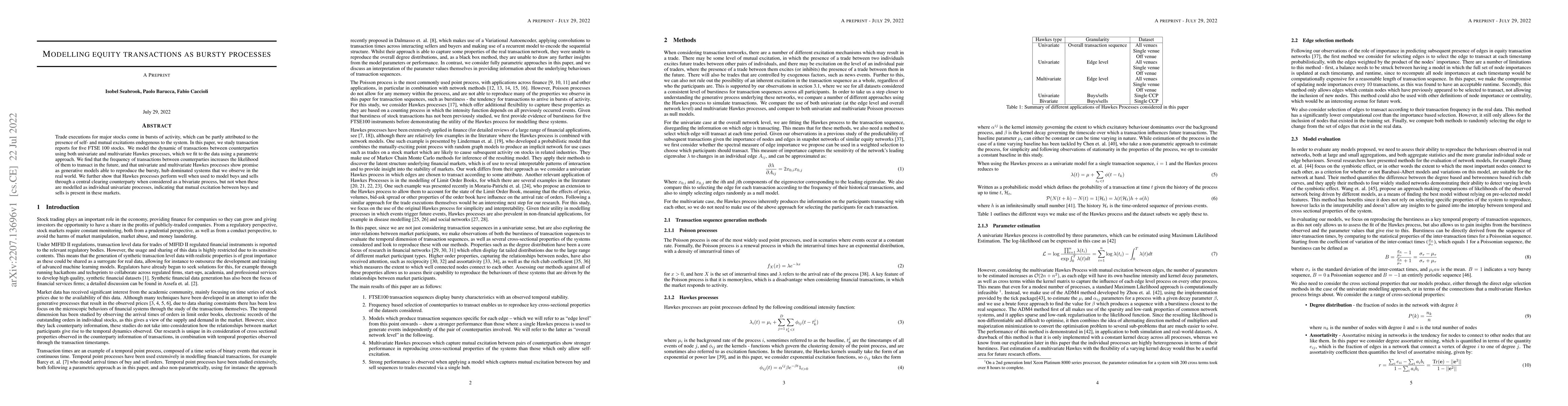

Trade executions for major stocks come in bursts of activity, which can be partly attributed to the presence of self- and mutual excitations endogenous to the system. In this paper, we study transac...

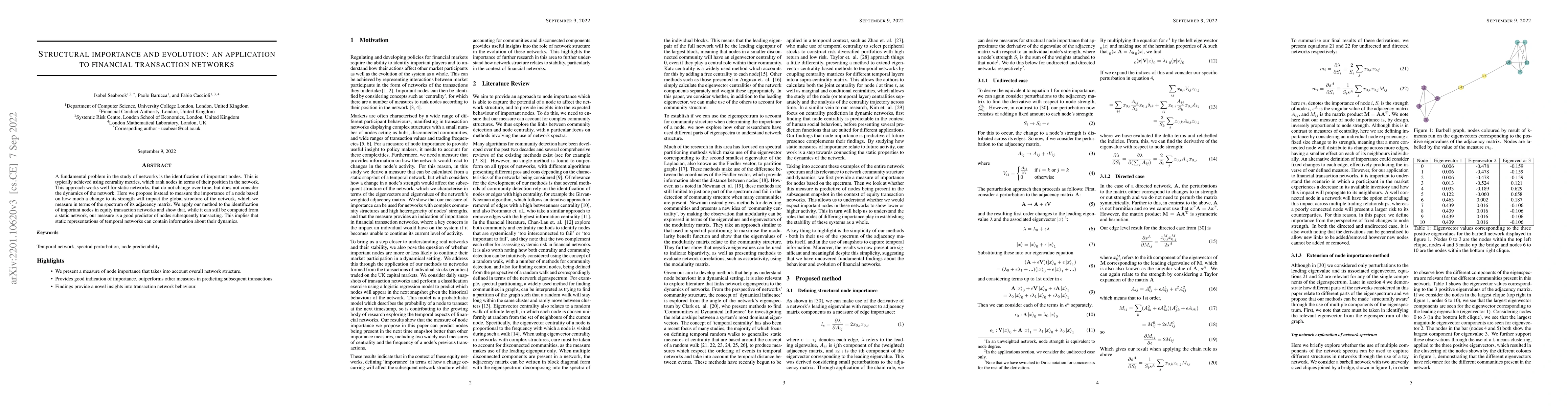

A fundamental problem in the study of networks is the identification of important nodes. This is typically achieved using centrality metrics, which rank nodes in terms of their position in the netwo...

We present a novel methodology to quantify the "impact" of and "response" to market shocks. We apply shocks to a group of stocks in a part of the market, and we quantify the effects in terms of aver...

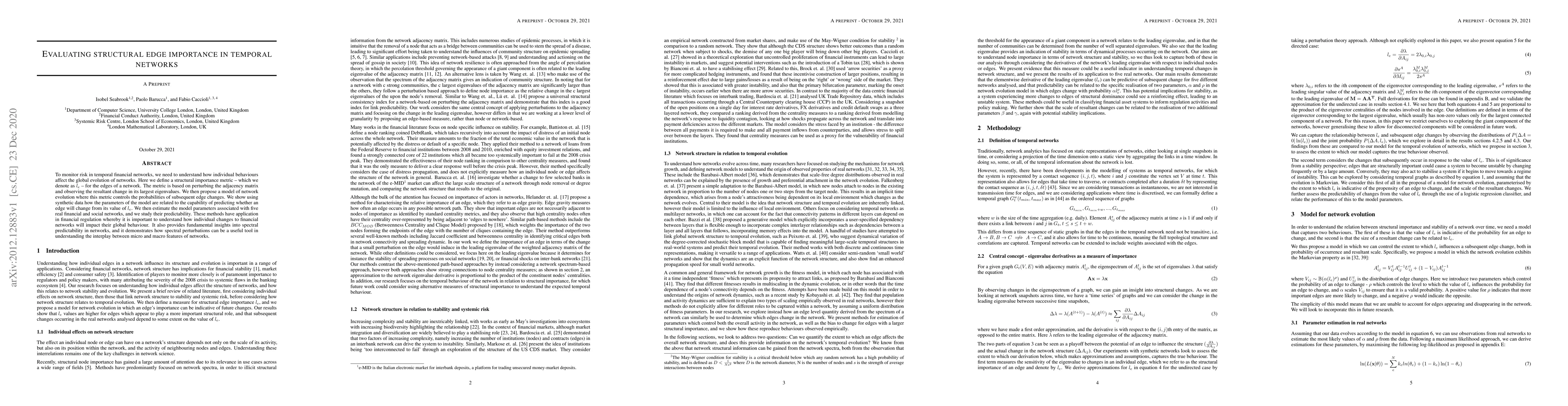

To monitor risk in temporal financial networks, we need to understand how individual behaviours affect the global evolution of networks. Here we define a structural importance metric - which we deno...