Academic Profile

Statistics

Similar Authors

Papers on arXiv

We formulate quantum computing solutions to a large class of dynamic nonlinear asset pricing models using algorithms, in theory exponentially more efficient than classical ones, which leverage the q...

We present a classical enhancement to improve the accuracy of the Hybrid variant (Hybrid HHL) of the quantum algorithm for solving liner systems of equations proposed by Harrow, Hassidim, and Lloyd ...

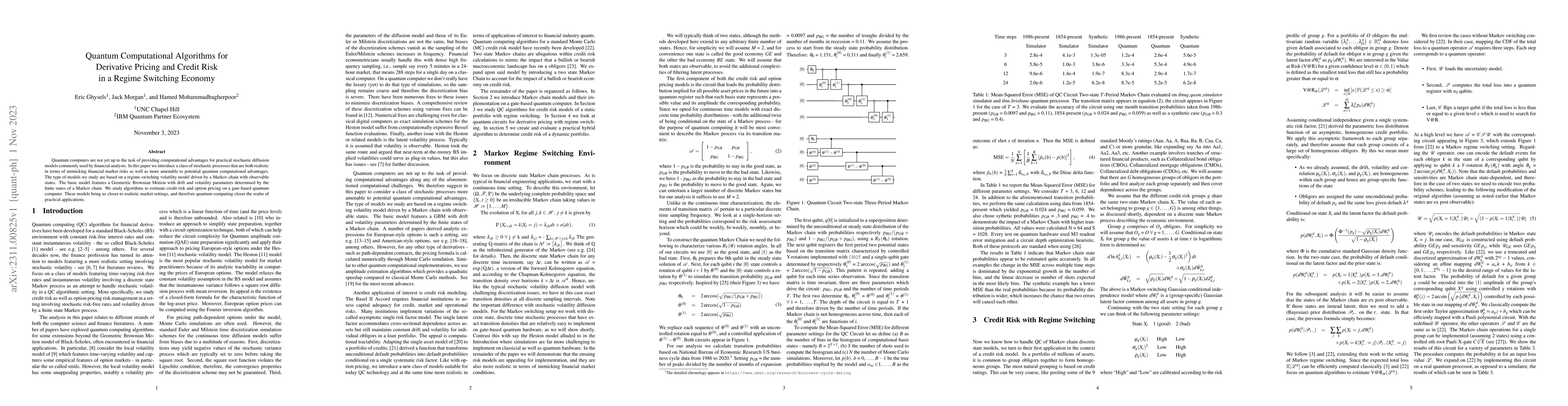

Quantum computers are not yet up to the task of providing computational advantages for practical stochastic diffusion models commonly used by financial analysts. In this paper we introduce a class o...

Stochastic volatility models are the backbone of financial engineering. We study both continuous time diffusions as well as discrete time models. We propose two novel approaches to estimating stochast...

Quantum machine learning holds promise for advancing time series forecasting. The Quantum Recurrent Neural Network (QRNN), inspired by classical RNNs, encodes temporal data into quantum states that ar...

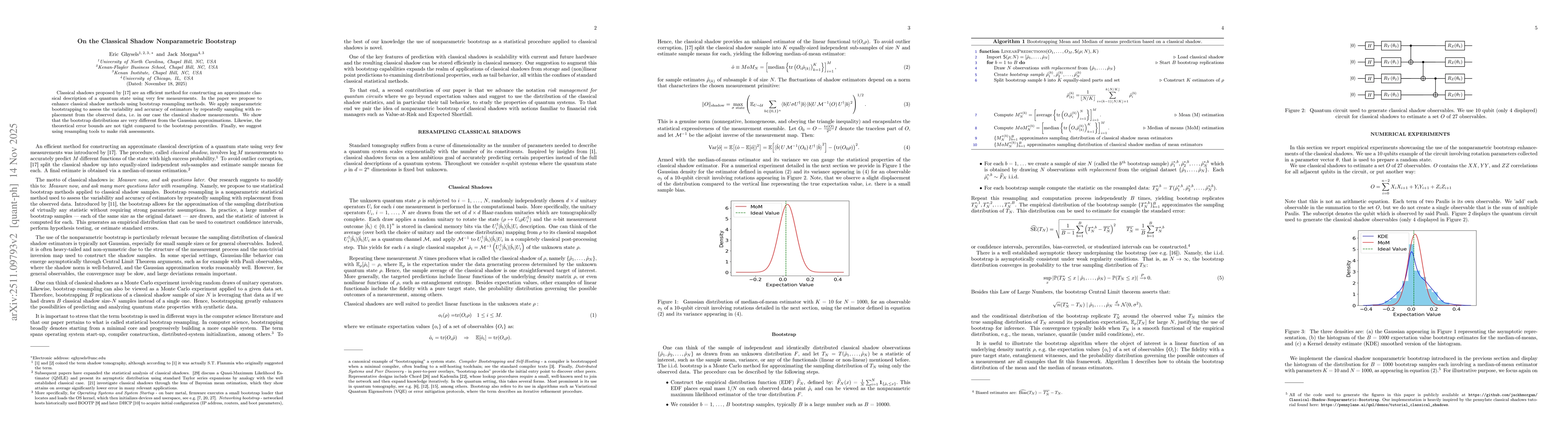

Classical shadows are an efficient method for constructing an approximate classical description of a quantum state using very few measurements. In the paper we propose to enhance classical shadow meth...