Academic Profile

Statistics

Similar Authors

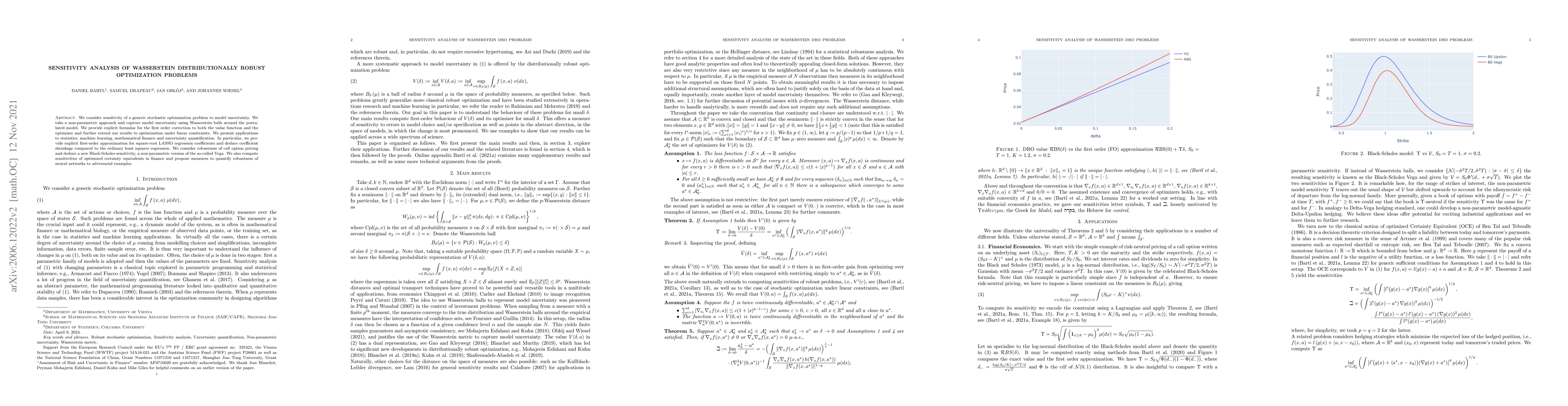

Papers on arXiv

The aim of this study is to find a generic method for generating a path of the solution of a given stochastic differential equation which is more efficient than the standard Euler-Maruyama scheme wi...

We introduce and study geometric Bass martingales. Bass martingales were introduced in \cite{Ba83} and studied recently in a series of works, including \cite{BaBeHuKa20,BaBeScTs23}, where they appea...

We contribute to the recent studies of the so-called Bass martingale. Backhoff-Veraguas et al. (2020) showed it is the solution to the martingale Benamou-Brenier (mBB) problem, i.e., among all marti...

We develop and implement a non-parametric method for joint exact calibration of a local volatility model and a correlated stochastic short rate model using semimartingale optimal transport. The meth...

Deep neural networks are known to be vulnerable to adversarial attacks (AA). For an image recognition task, this means that a small perturbation of the original can result in the image being misclas...

We develop a non-parametric, optimal transport driven, calibration methodology for local volatility models with stochastic interest rate. The method finds a fully calibrated model which is the close...

We provide a survey of recent results on model calibration by Optimal Transport. We present the general framework and then discuss the calibration of local, and local-stochastic, volatility models t...

We consider the optimal investment and marginal utility pricing problem of a risk averse agent and quantify their exposure to a small amount of model uncertainty. Specifically, we compute explicitly...

We develop an approach to solve Barberis (2012)'s casino gambling model in which a gambler whose preferences are specified by the cumulative prospect theory (CPT) must decide when to stop gambling b...

We consider sensitivity of a generic stochastic optimization problem to model uncertainty. We take a non-parametric approach and capture model uncertainty using Wasserstein balls around the postulat...

This paper addresses the joint calibration problem of SPX options and VIX options or futures. We show that the problem can be formulated as a semimartingale optimal transport problem under a finite ...

We consider statistical estimation of superhedging prices using historical stock returns in a frictionless market with d traded assets. We introduce a plugin estimator based on empirical measures an...

We study the causal distributionally robust optimization (DRO) in both discrete- and continuous- time settings. The framework captures model uncertainty, with potential models penalized in function of...

Design of adversarial attacks for deep neural networks, as well as methods of adversarial training against them, are subject of intense research. In this paper, we propose methods to train against dis...