Academic Profile

Statistics

Similar Authors

Papers on arXiv

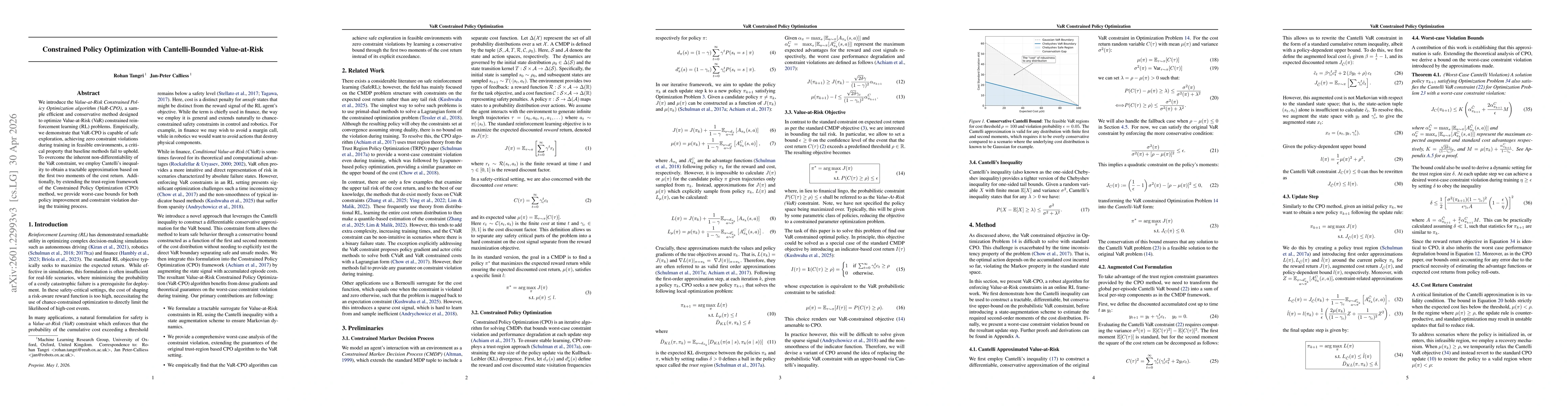

In Statistical Arbitrage (StatArb), classical mean reversion trading strategies typically hinge on asset-pricing or PCA based models to identify the mean of a synthetic asset. Once such a (linear) m...

This paper examines the asymptotic convergence properties of Lipschitz interpolation methods within the context of bounded stochastic noise. In the first part of the paper, we establish probabilisti...

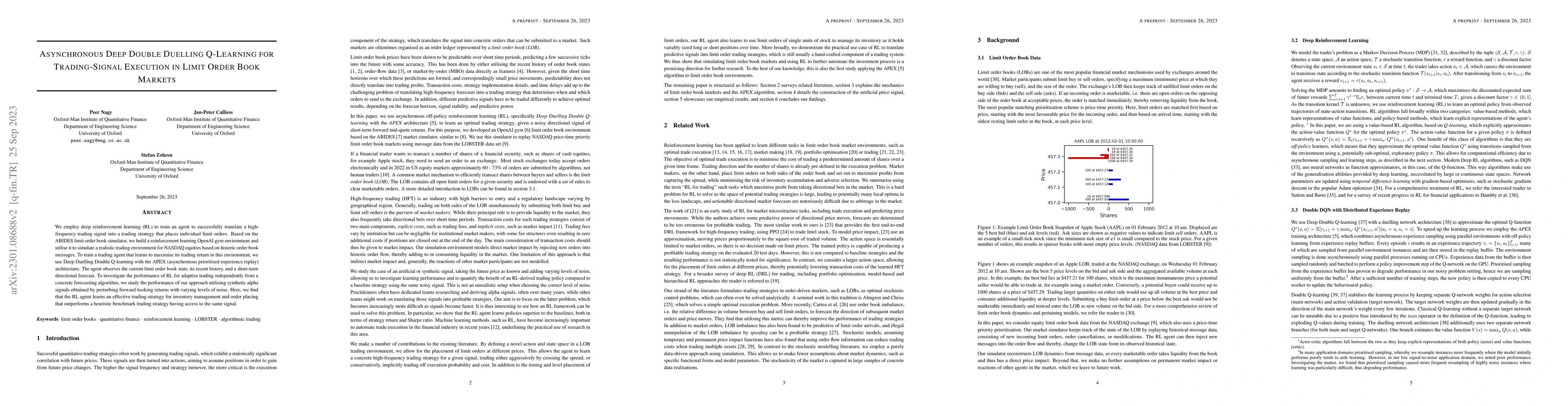

We employ deep reinforcement learning (RL) to train an agent to successfully translate a high-frequency trading signal into a trading strategy that places individual limit orders. Based on the ABIDE...

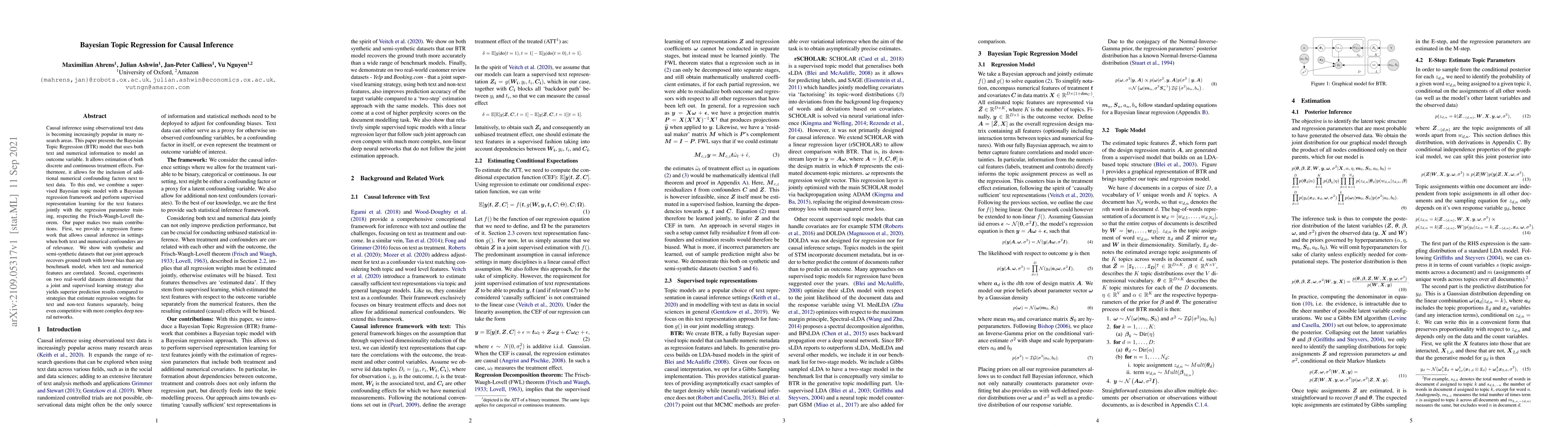

Causal inference using observational text data is becoming increasingly popular in many research areas. This paper presents the Bayesian Topic Regression (BTR) model that uses both text and numerica...

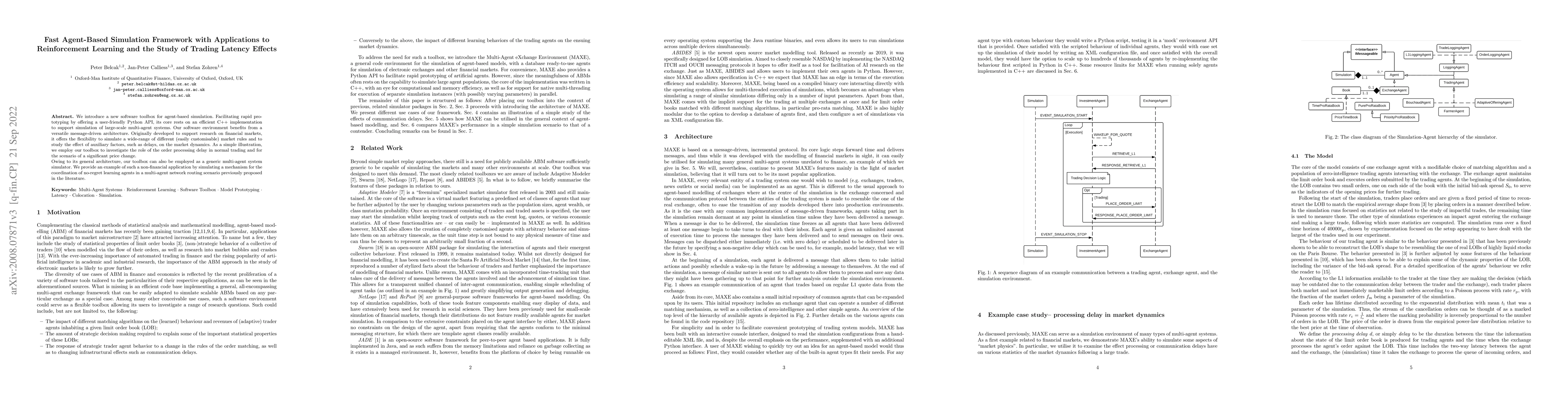

We introduce a new software toolbox for agent-based simulation. Facilitating rapid prototyping by offering a user-friendly Python API, its core rests on an efficient C++ implementation to support si...

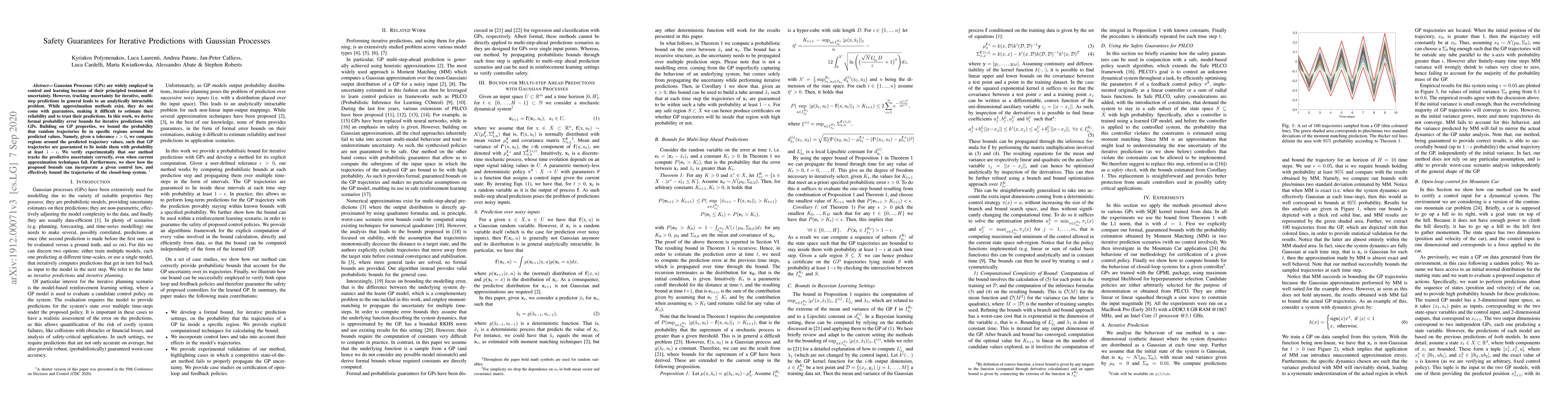

Gaussian Processes (GPs) are widely employed in control and learning because of their principled treatment of uncertainty. However, tracking uncertainty for iterative, multi-step predictions in gene...

We introduce the Value-at-Risk Constrained Policy Optimization algorithm (VaR-CPO), a sample efficient and conservative method designed to optimize Value-at-Risk (VaR) constraints directly. Empiricall...