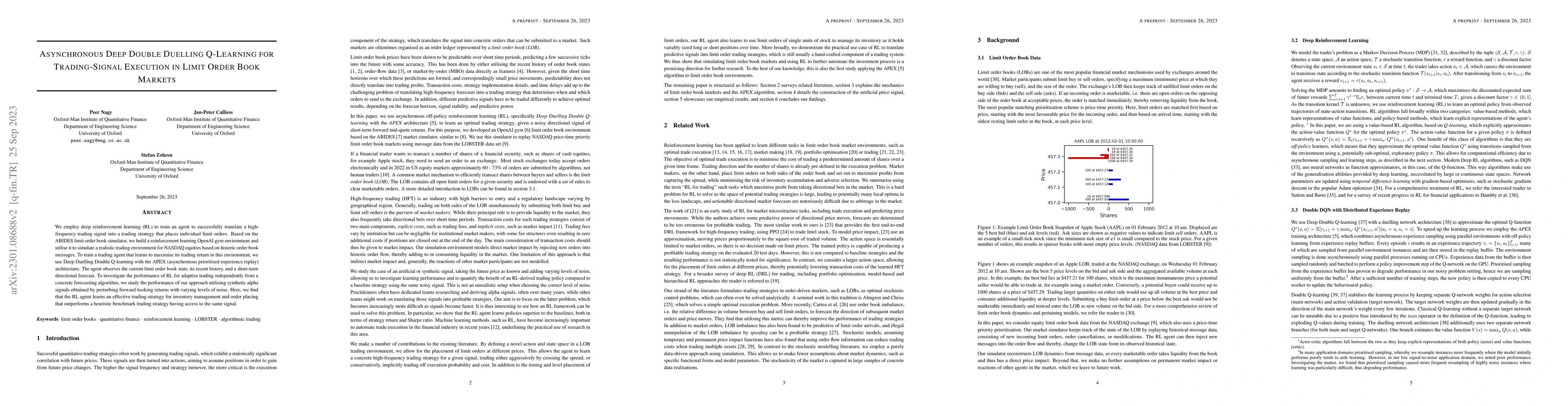

Asynchronous Deep Double Duelling Q-Learning for Trading-Signal Execution in Limit Order Book Markets

Publication

Metrics

AI Quick Summary

This paper uses deep reinforcement learning to develop a trading agent that translates high-frequency trading signals into limit order placements in a simulated NASDAQ environment. The agent employs Deep Double Duelling Q-learning with APEX architecture, achieving superior performance compared to a heuristic benchmark in managing inventory and placing orders.

Paper Preview

Abstract

We employ deep reinforcement learning (RL) to train an agent to successfully translate a high-frequency trading signal into a trading strategy that places individual limit orders. Based on the ABIDES limit order book simulator, we build a reinforcement learning OpenAI gym environment and utilise it to simulate a realistic trading environment for NASDAQ equities based on historic order book messages. To train a trading agent that learns to maximise its trading return in this environment, we use Deep Duelling Double Q-learning with the APEX (asynchronous prioritised experience replay) architecture. The agent observes the current limit order book state, its recent history, and a short-term directional forecast. To investigate the performance of RL for adaptive trading independently from a concrete forecasting algorithm, we study the performance of our approach utilising synthetic alpha signals obtained by perturbing forward-looking returns with varying levels of noise. Here, we find that the RL agent learns an effective trading strategy for inventory management and order placing that outperforms a heuristic benchmark trading strategy having access to the same signal.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0