Academic Profile

Statistics

Similar Authors

Papers on arXiv

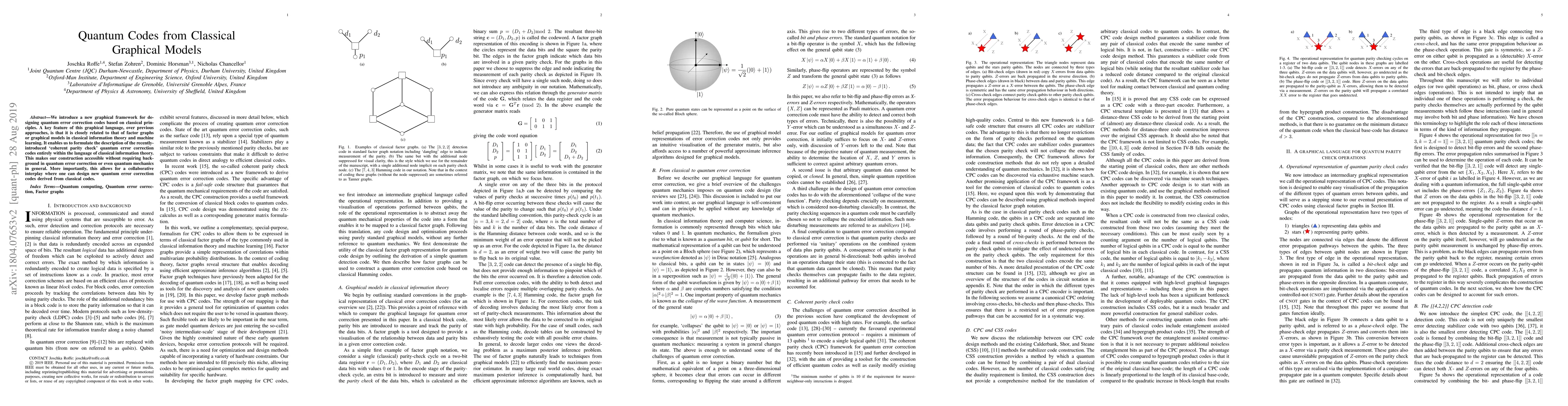

We introduce a high-level graphical framework for designing and analysing quantum error correcting codes, centred on what we term the coherent parity check (CPC). The graphical formulation is based ...

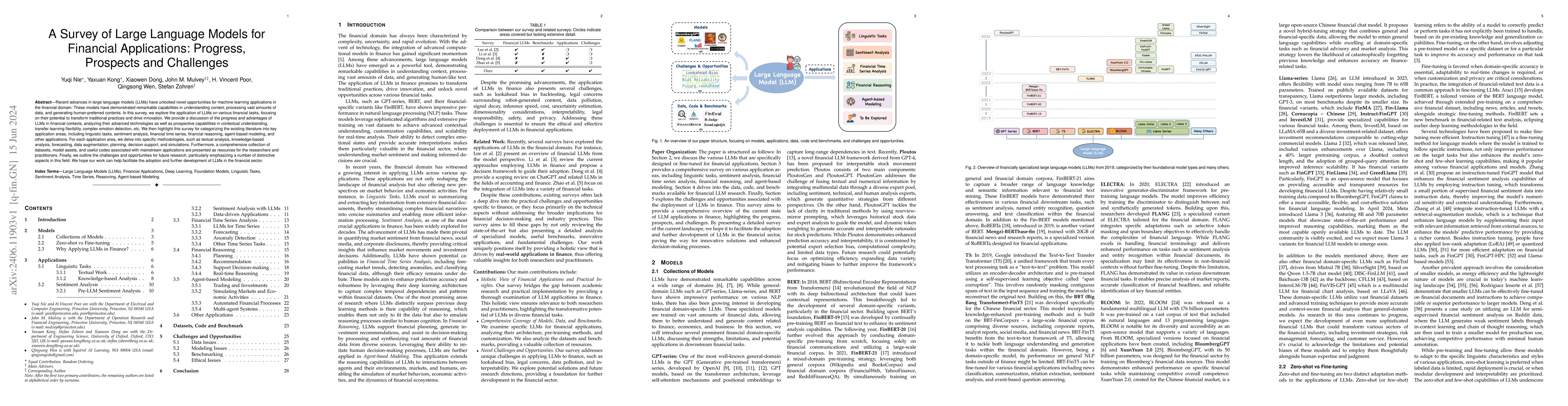

Recent advances in large language models (LLMs) have unlocked novel opportunities for machine learning applications in the financial domain. These models have demonstrated remarkable capabilities in...

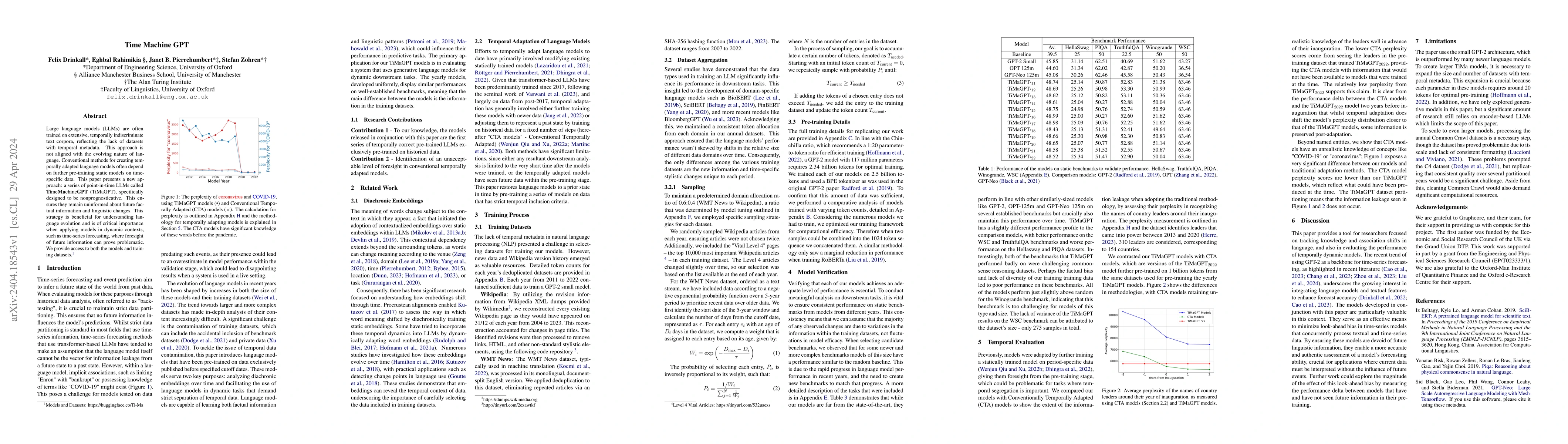

Large language models (LLMs) are often trained on extensive, temporally indiscriminate text corpora, reflecting the lack of datasets with temporal metadata. This approach is not aligned with the evo...

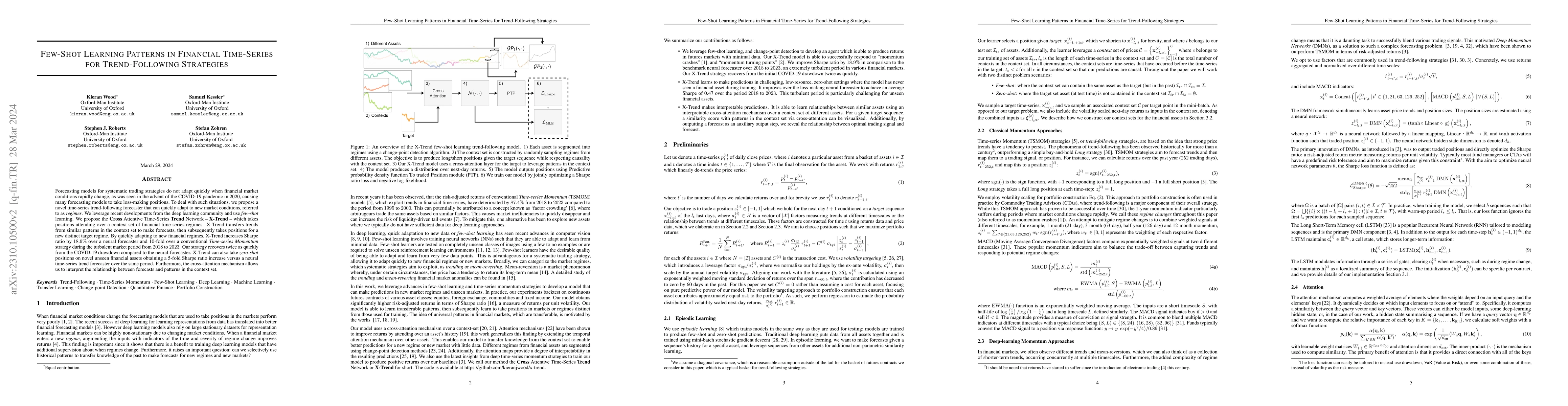

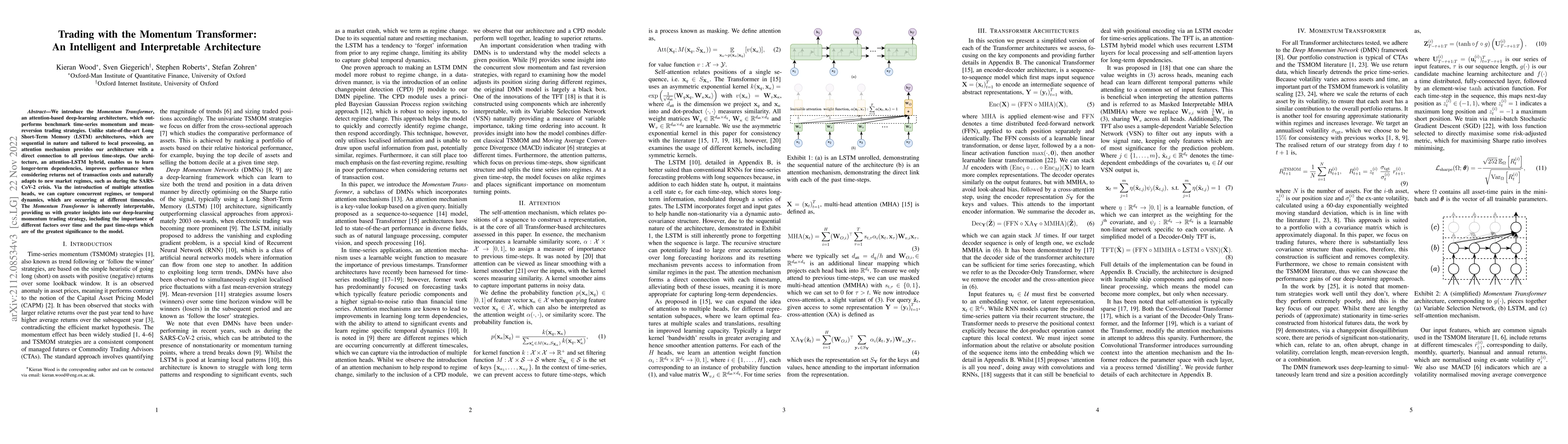

Forecasting models for systematic trading strategies do not adapt quickly when financial market conditions rapidly change, as was seen in the advent of the COVID-19 pandemic in 2020, causing many fo...

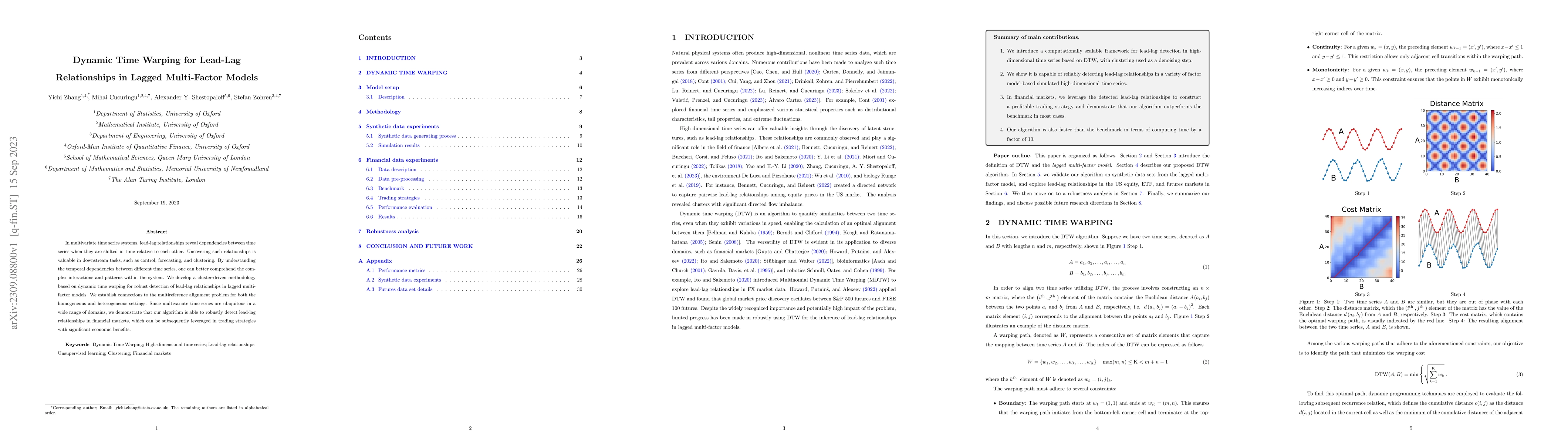

In multivariate time series systems, lead-lag relationships reveal dependencies between time series when they are shifted in time relative to each other. Uncovering such relationships is valuable in...

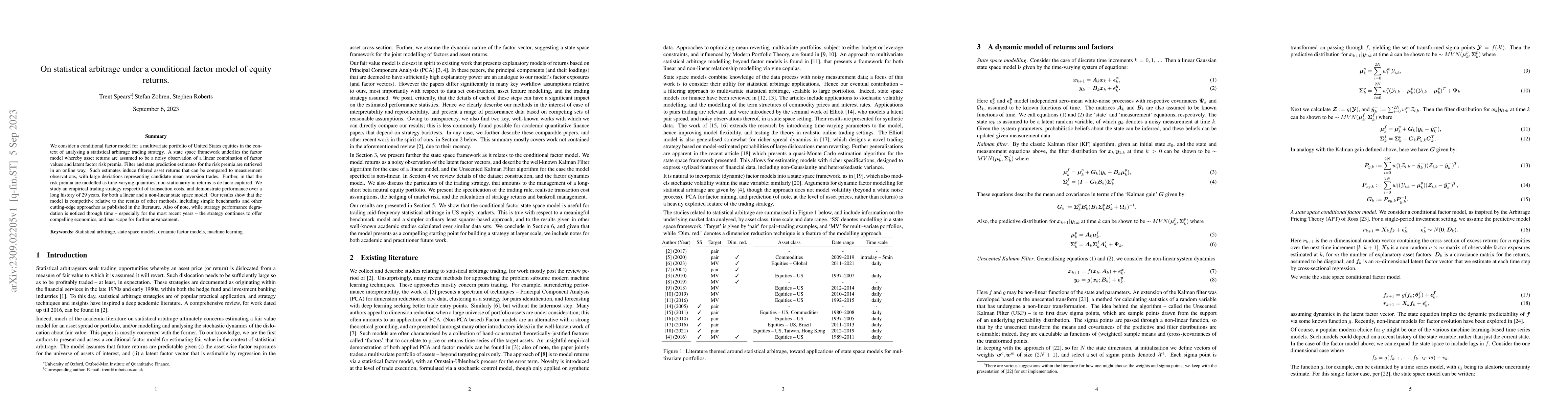

We consider a conditional factor model for a multivariate portfolio of United States equities in the context of analysing a statistical arbitrage trading strategy. A state space framework underlies ...

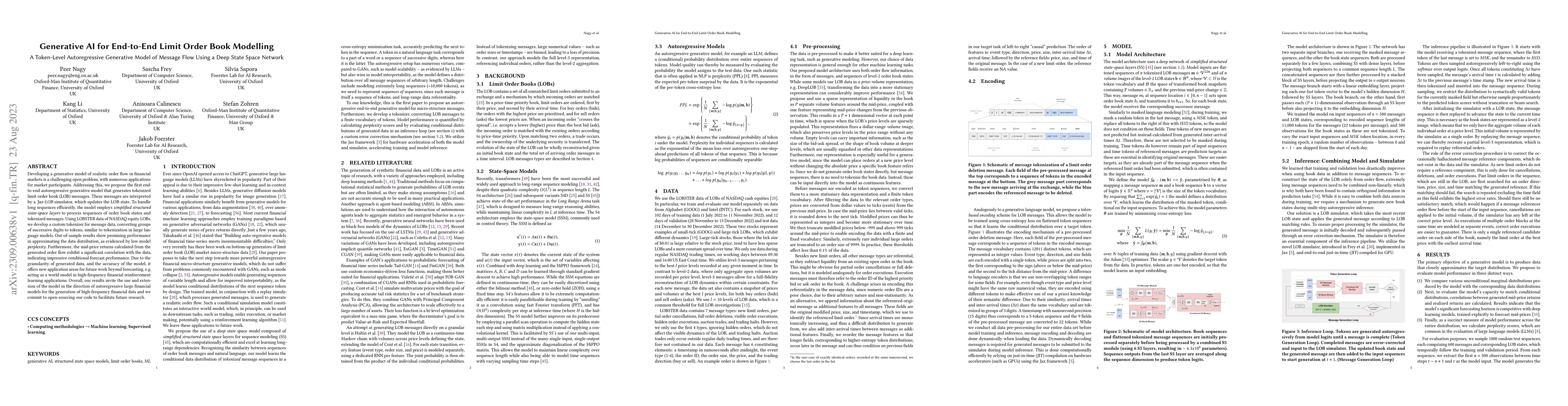

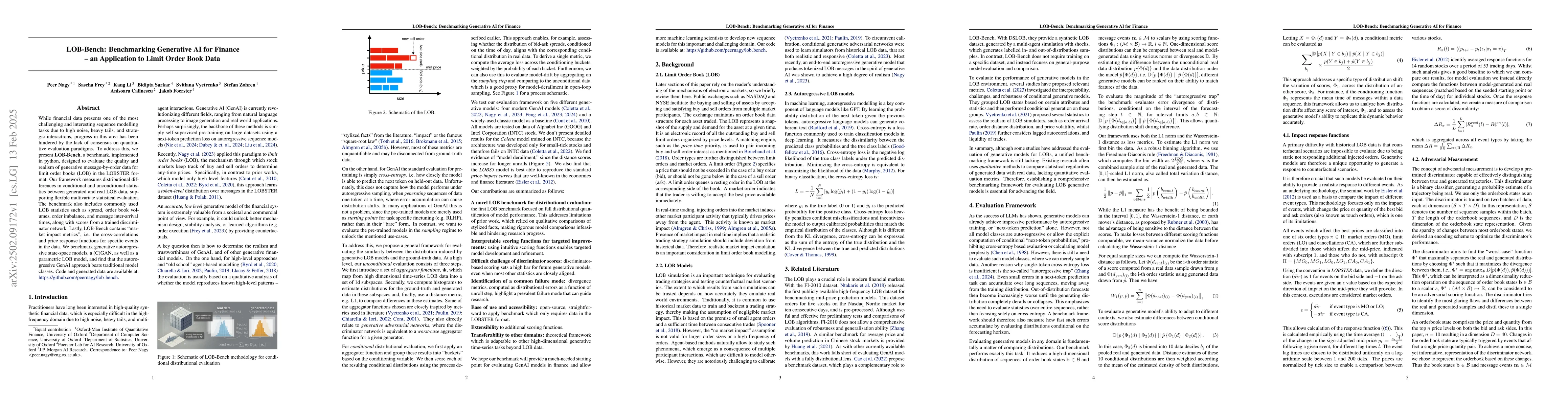

Developing a generative model of realistic order flow in financial markets is a challenging open problem, with numerous applications for market participants. Addressing this, we propose the first en...

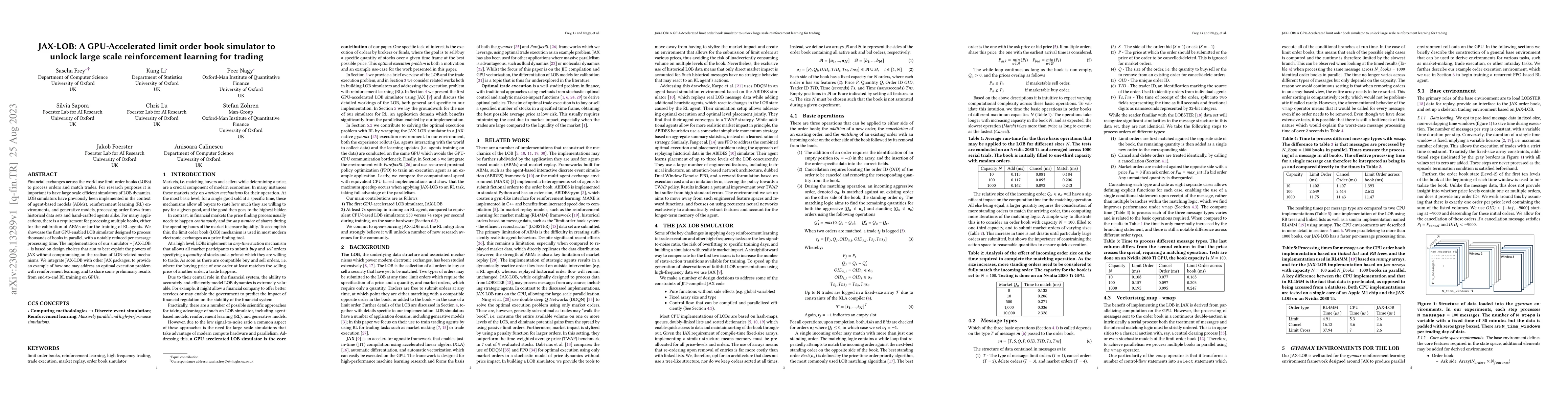

Financial exchanges across the world use limit order books (LOBs) to process orders and match trades. For research purposes it is important to have large scale efficient simulators of LOB dynamics. ...

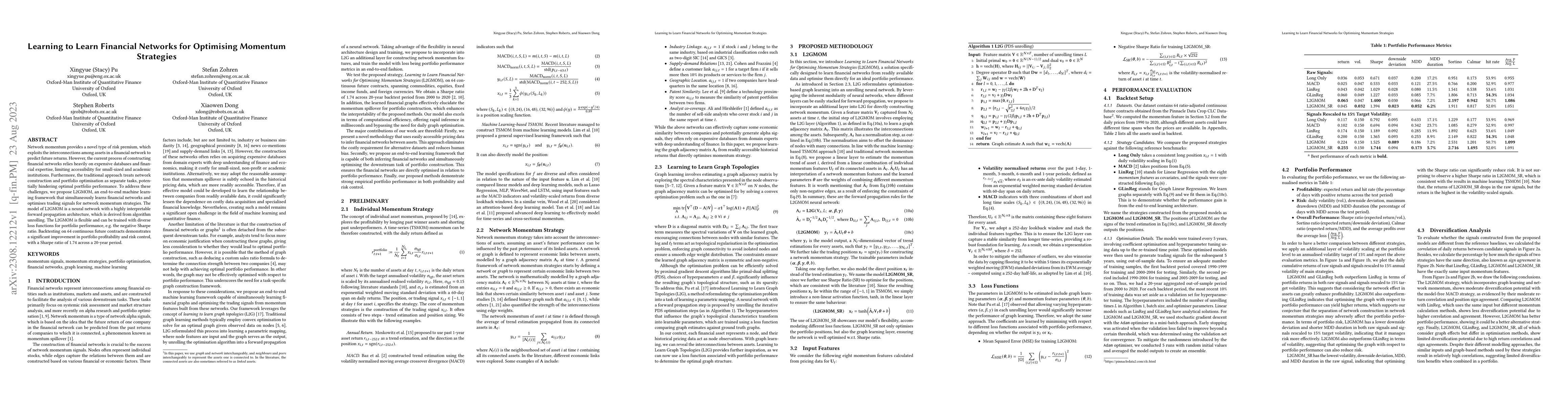

Network momentum provides a novel type of risk premium, which exploits the interconnections among assets in a financial network to predict future returns. However, the current process of constructin...

We investigate the concept of network momentum, a novel trading signal derived from momentum spillover across assets. Initially observed within the confines of pairwise economic and fundamental ties...

A trite yet fundamental question in economics is: What causes large asset price fluctuations? A tenfold rise in the price of GameStop equity, between the 22nd and 28th of January 2021, demonstrated ...

Cryptocurrency trading represents a nascent field of research, with growing adoption in industry. Aided by its decentralised nature, many metrics describing cryptocurrencies are accessible with a si...

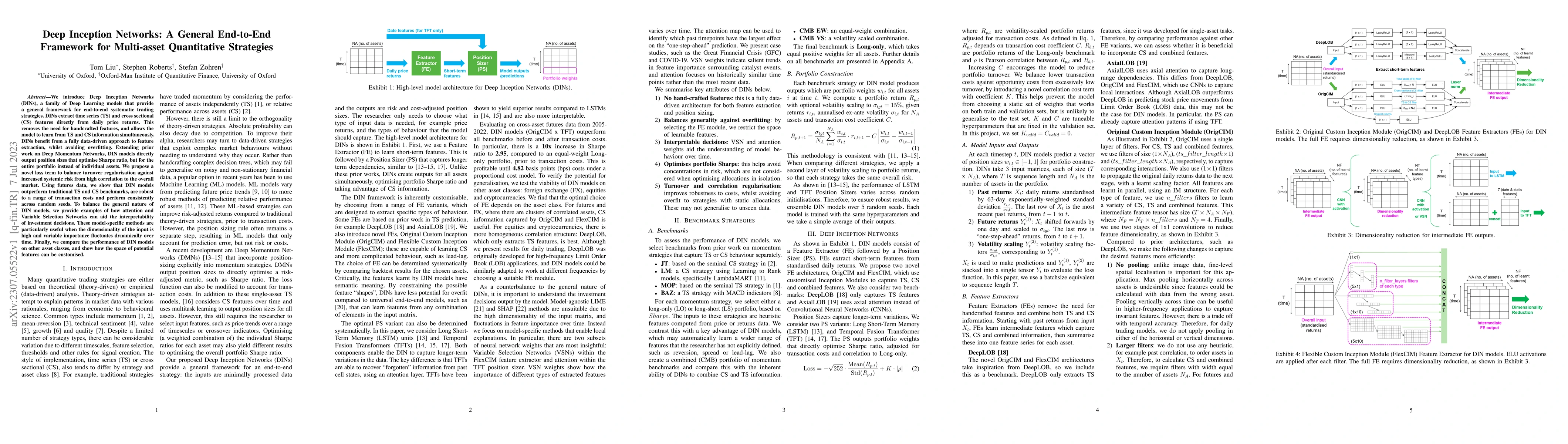

We introduce Deep Inception Networks (DINs), a family of Deep Learning models that provide a general framework for end-to-end systematic trading strategies. DINs extract time series (TS) and cross s...

One of the key decisions in execution strategies is the choice between a passive (liquidity providing) or an aggressive (liquidity taking) order to execute a trade in a limit order book (LOB). Essen...

In multivariate time series systems, key insights can be obtained by discovering lead-lag relationships inherent in the data, which refer to the dependence between two time series shifted in time re...

We introduce Spatio-Temporal Momentum strategies, a class of models that unify both time-series and cross-sectional momentum strategies by trading assets based on their cross-sectional momentum feat...

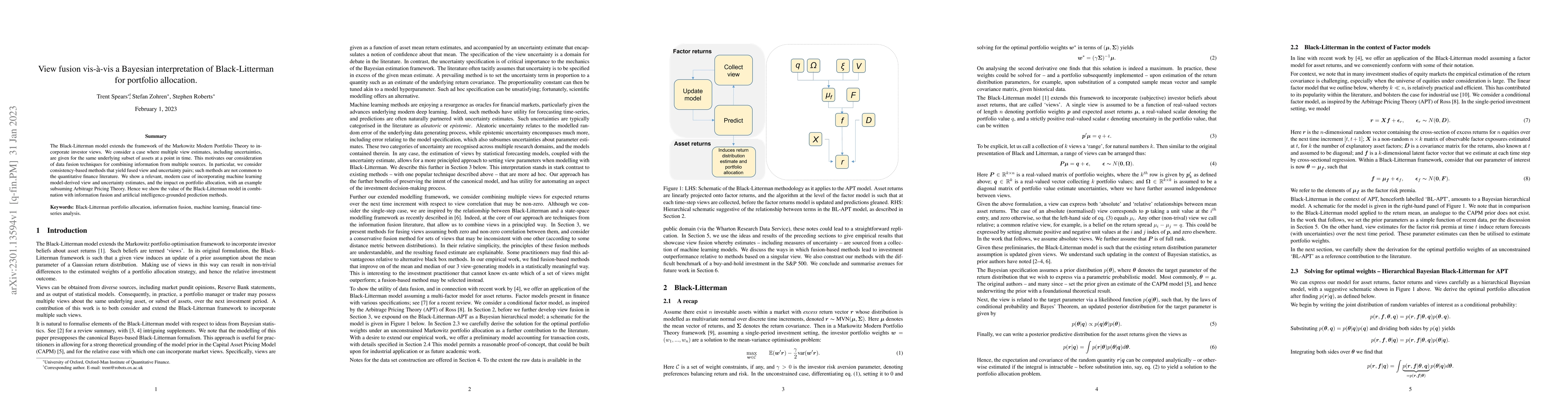

The Black-Litterman model extends the framework of the Markowitz Modern Portfolio Theory to incorporate investor views. We consider a case where multiple view estimates, including uncertainties, are...

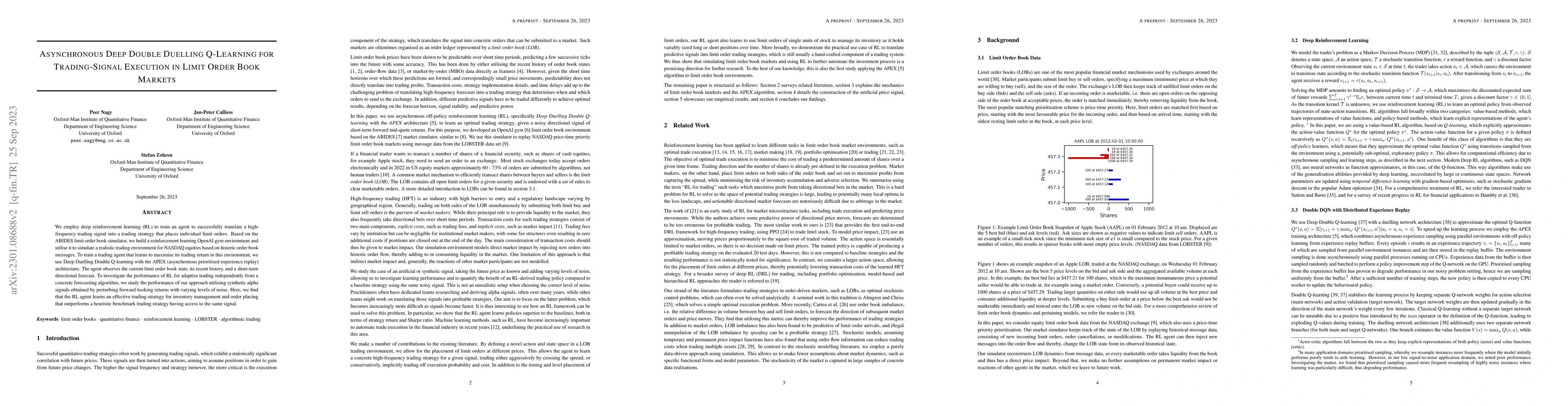

We employ deep reinforcement learning (RL) to train an agent to successfully translate a high-frequency trading signal into a trading strategy that places individual limit orders. Based on the ABIDE...

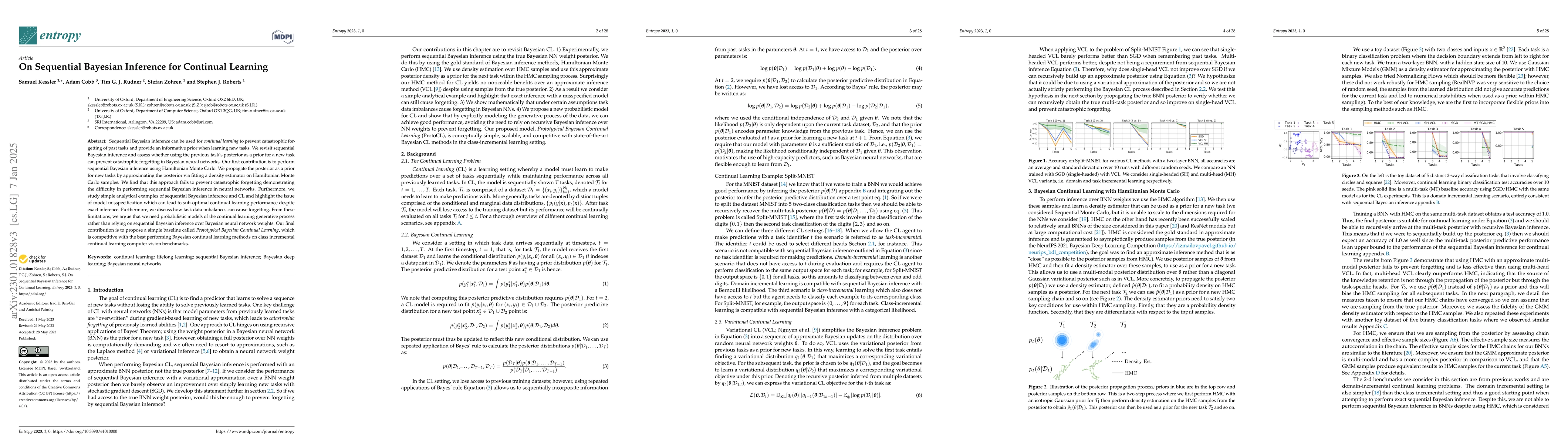

Sequential Bayesian inference can be used for continual learning to prevent catastrophic forgetting of past tasks and provide an informative prior when learning new tasks. We revisit sequential Baye...

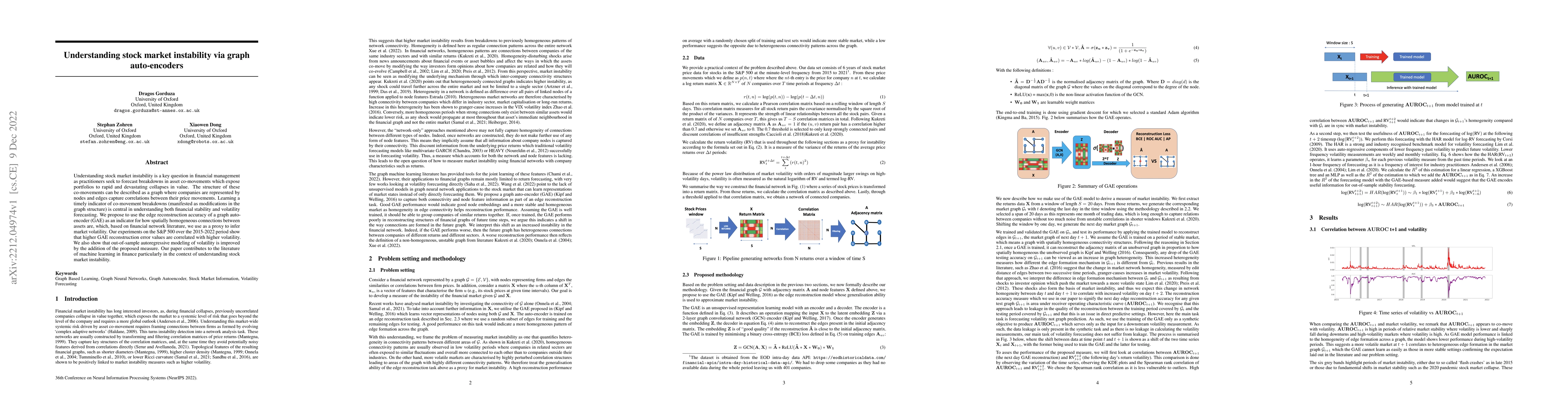

Understanding stock market instability is a key question in financial management as practitioners seek to forecast breakdowns in asset co-movements which expose portfolios to rapid and devastating c...

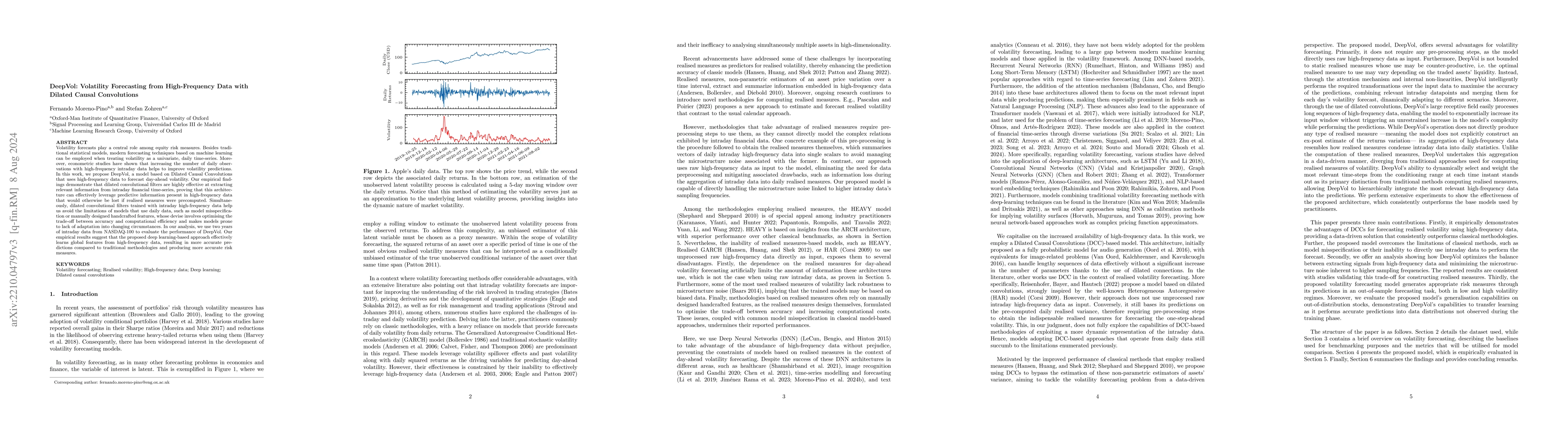

Volatility forecasts play a central role among equity risk measures. Besides traditional statistical models, modern forecasting techniques, based on machine learning, can readily be employed when tr...

Cross-sectional strategies are a classical and popular trading style, with recent high performing variants incorporating sophisticated neural architectures. While these strategies have been applied ...

We present a novel approach incorporating transformer-based language models into infectious disease modelling. Text-derived features are quantified by tracking high-density clusters of sentence-leve...

This paper presents a novel framework for analyzing the optimal asset and signal combination problem. Our approach builds upon the dynamic portfolio selection problem introduced by Brandt and Santa-...

We introduce the Momentum Transformer, an attention-based deep-learning architecture, which outperforms benchmark time-series momentum and mean-reversion trading strategies. Unlike state-of-the-art ...

We propose a universal end-to-end framework for portfolio optimization where asset distributions are directly obtained. The designed framework circumvents the traditional forecasting step and avoids...

This study develops FinText, a financial word embedding compiled from 15 years of business news archives. The results show that FinText produces substantially more accurate results than general word...

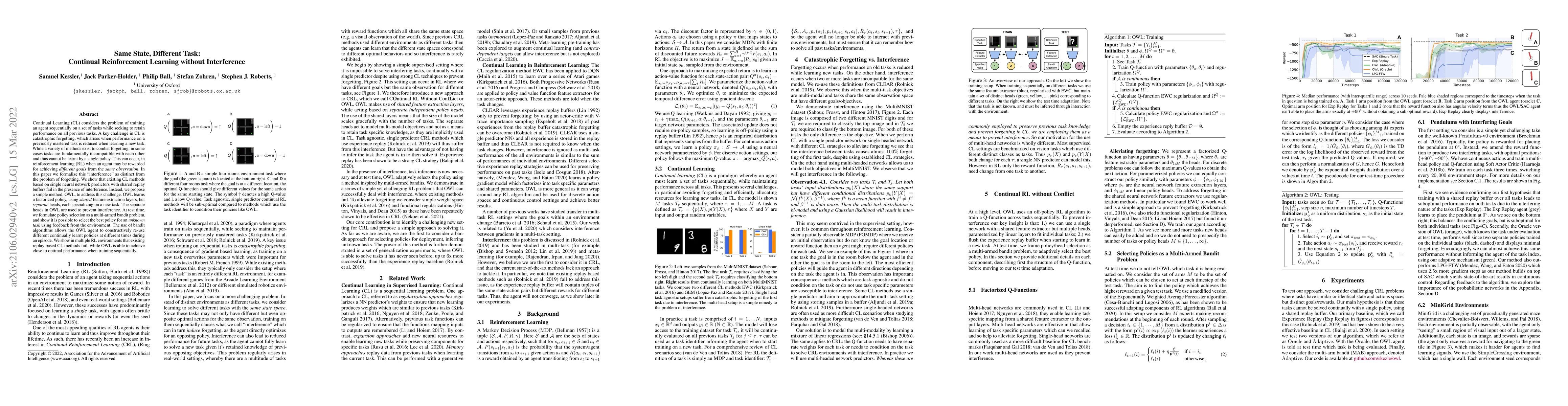

Continual Learning (CL) considers the problem of training an agent sequentially on a set of tasks while seeking to retain performance on all previous tasks. A key challenge in CL is catastrophic for...

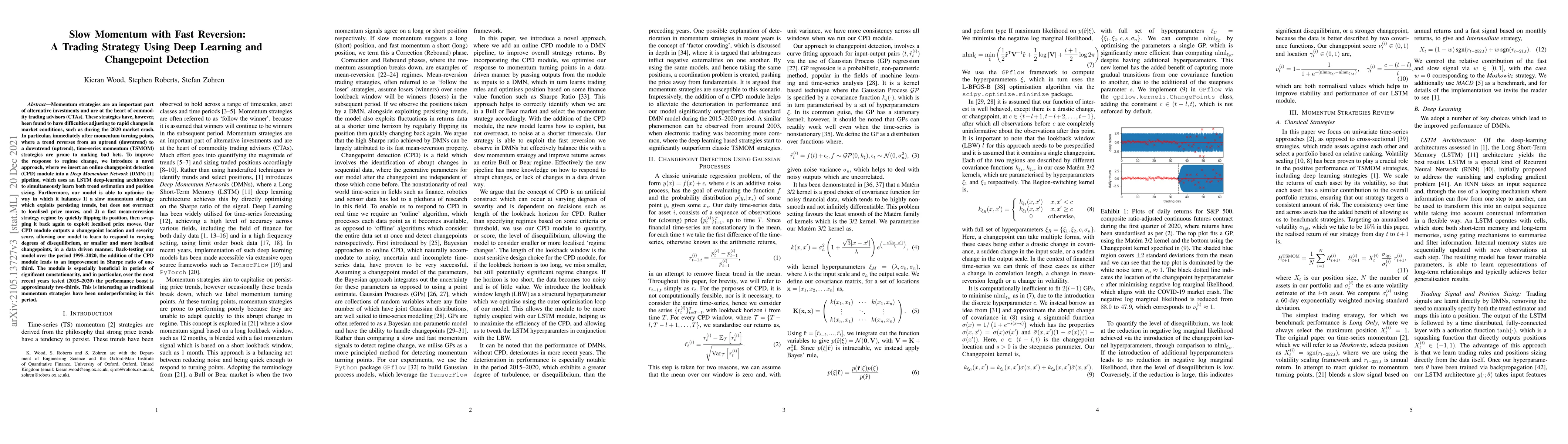

Momentum strategies are an important part of alternative investments and are at the heart of commodity trading advisors (CTAs). These strategies have, however, been found to have difficulties adjust...

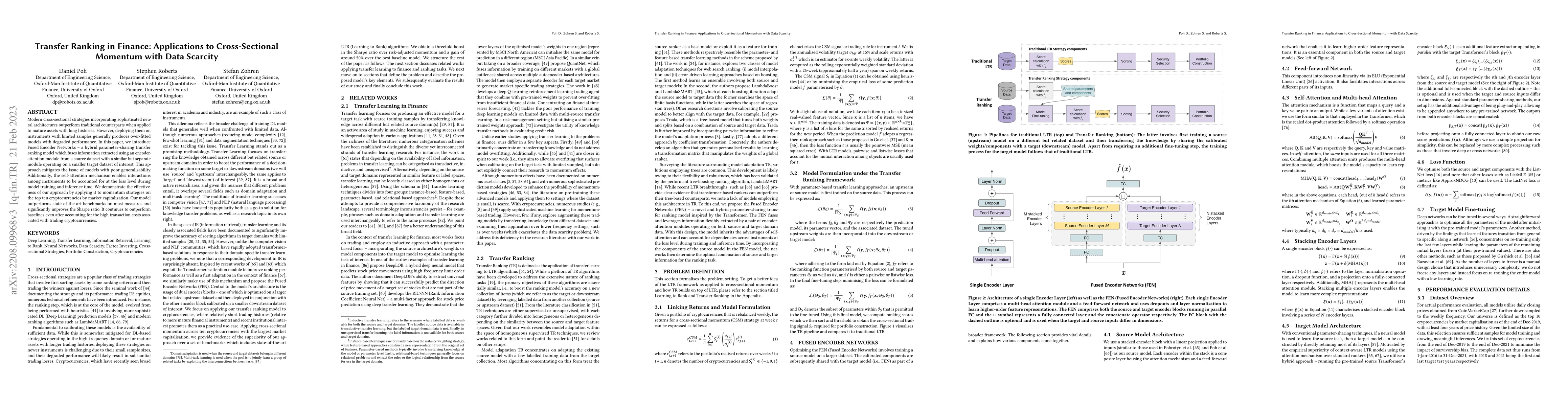

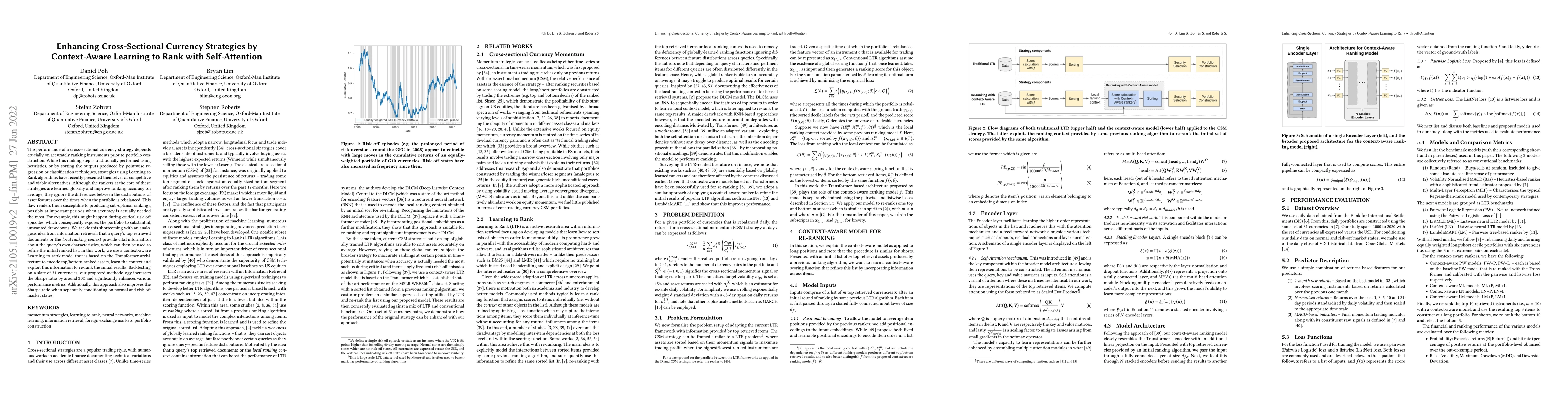

The performance of a cross-sectional currency strategy depends crucially on accurately ranking instruments prior to portfolio construction. While this ranking step is traditionally performed using h...

Market by order (MBO) data - a detailed feed of individual trade instructions for a given stock on an exchange - is arguably one of the most granular sources of microstructure information. While lim...

The success of a cross-sectional systematic strategy depends critically on accurately ranking assets prior to portfolio construction. Contemporary techniques perform this ranking step either with si...

We introduce a novel covariance estimator for portfolio selection that adapts to the non-stationary or persistent heteroskedastic environments of financial time series by employing exponentially wei...

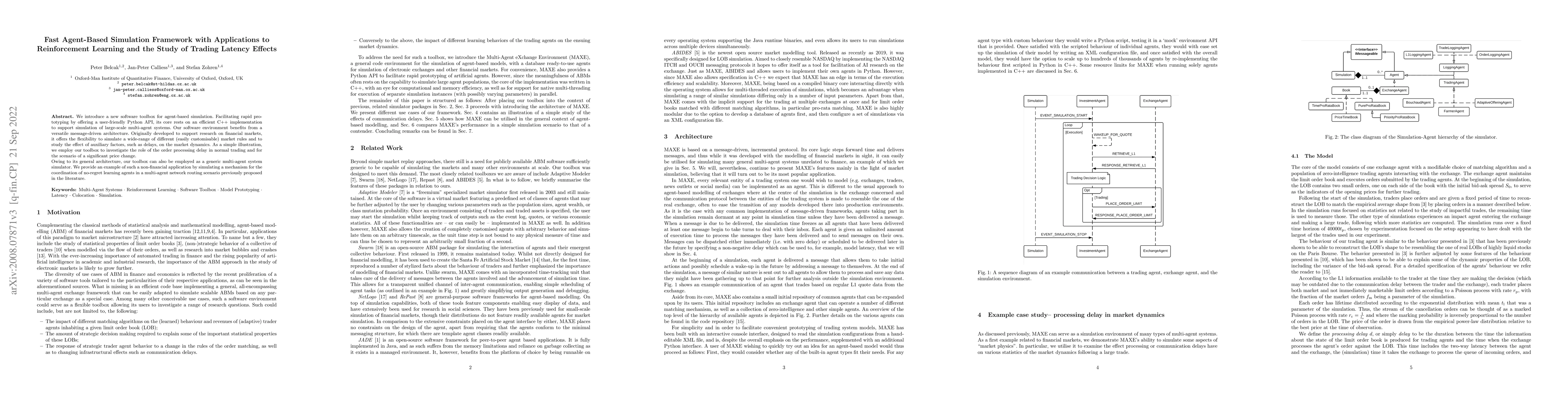

We introduce a new software toolbox for agent-based simulation. Facilitating rapid prototyping by offering a user-friendly Python API, its core rests on an efficient C++ implementation to support si...

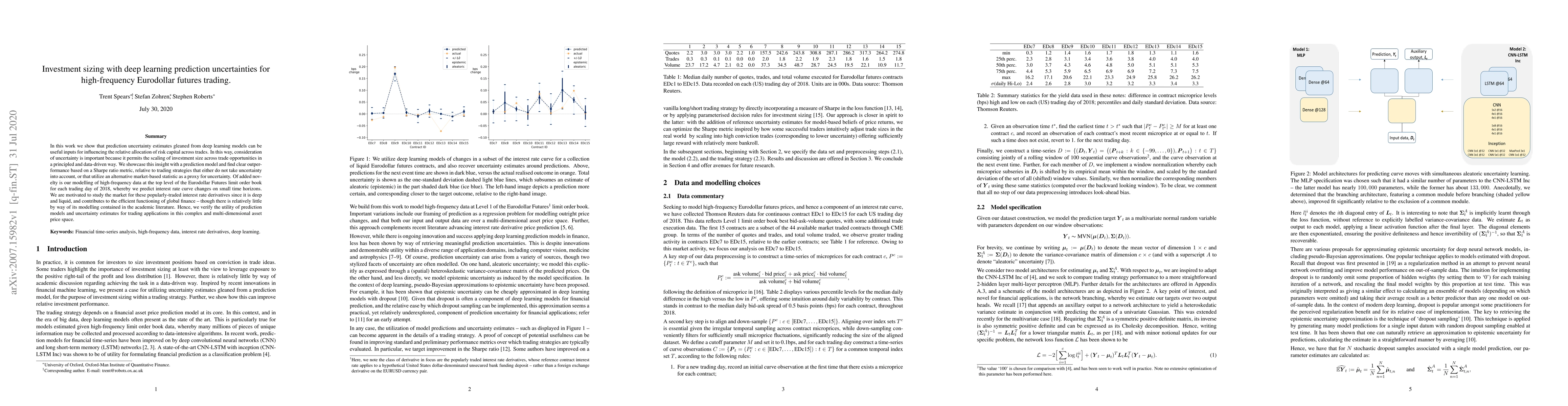

In this work we show that prediction uncertainty estimates gleaned from deep learning models can be useful inputs for influencing the relative allocation of risk capital across trades. In this way, ...

We study the effect of mini-batching on the loss landscape of deep neural networks using spiked, field-dependent random matrix theory. We demonstrate that the magnitude of the extremal values of the...

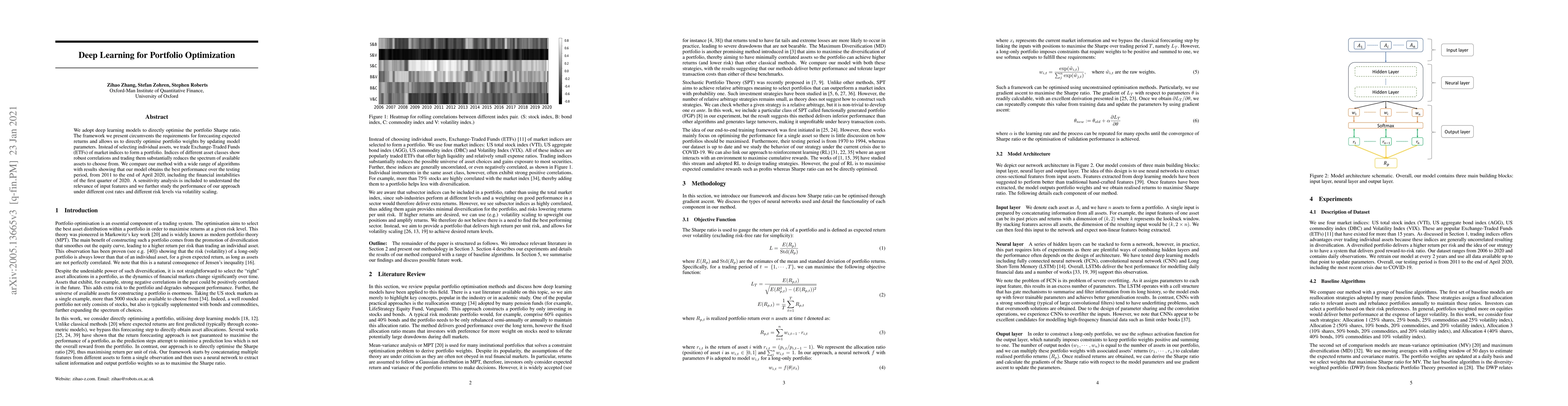

We adopt deep learning models to directly optimise the portfolio Sharpe ratio. The framework we present circumvents the requirements for forecasting expected returns and allows us to directly optimi...

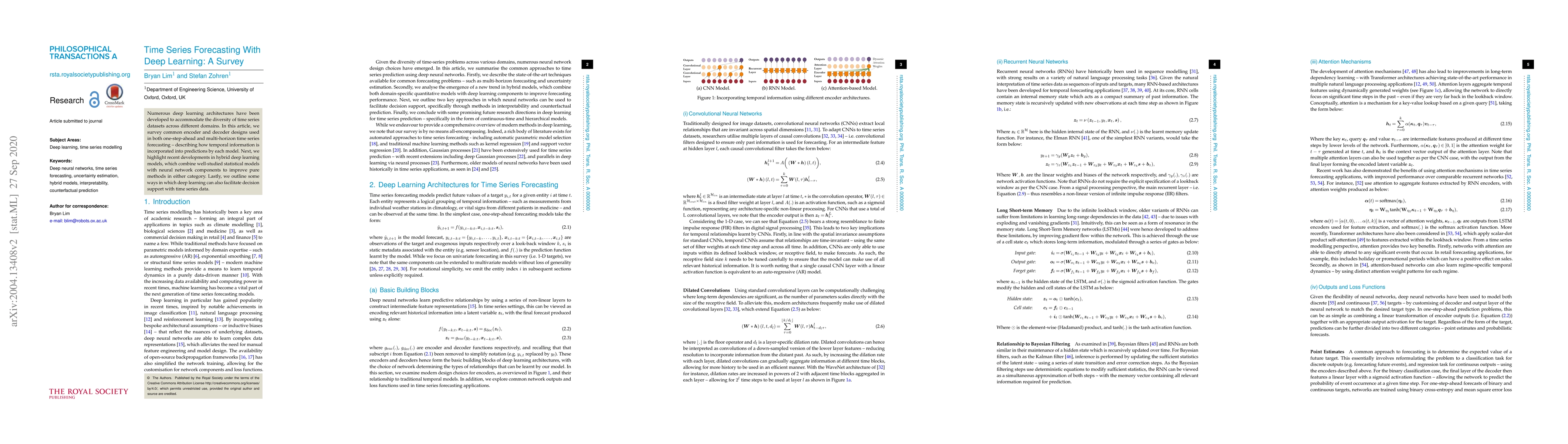

Numerous deep learning architectures have been developed to accommodate the diversity of time series datasets across different domains. In this article, we survey common encoder and decoder designs ...

Graph spectral techniques for measuring graph similarity, or for learning the cluster number, require kernel smoothing. The choice of kernel function and bandwidth are typically chosen in an ad-hoc ...

We adopt Deep Reinforcement Learning algorithms to design trading strategies for continuous futures contracts. Both discrete and continuous action spaces are considered and volatility scaling is inc...

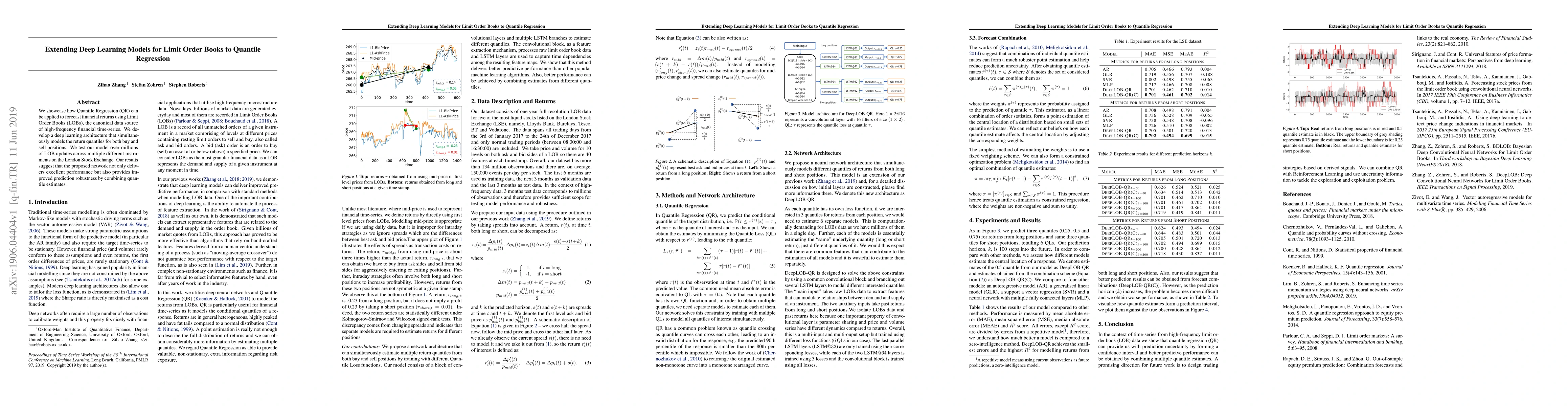

We showcase how Quantile Regression (QR) can be applied to forecast financial returns using Limit Order Books (LOBs), the canonical data source of high-frequency financial time-series. We develop a ...

Efficient approximation lies at the heart of large-scale machine learning problems. In this paper, we propose a novel, robust maximum entropy algorithm, which is capable of dealing with hundreds of ...

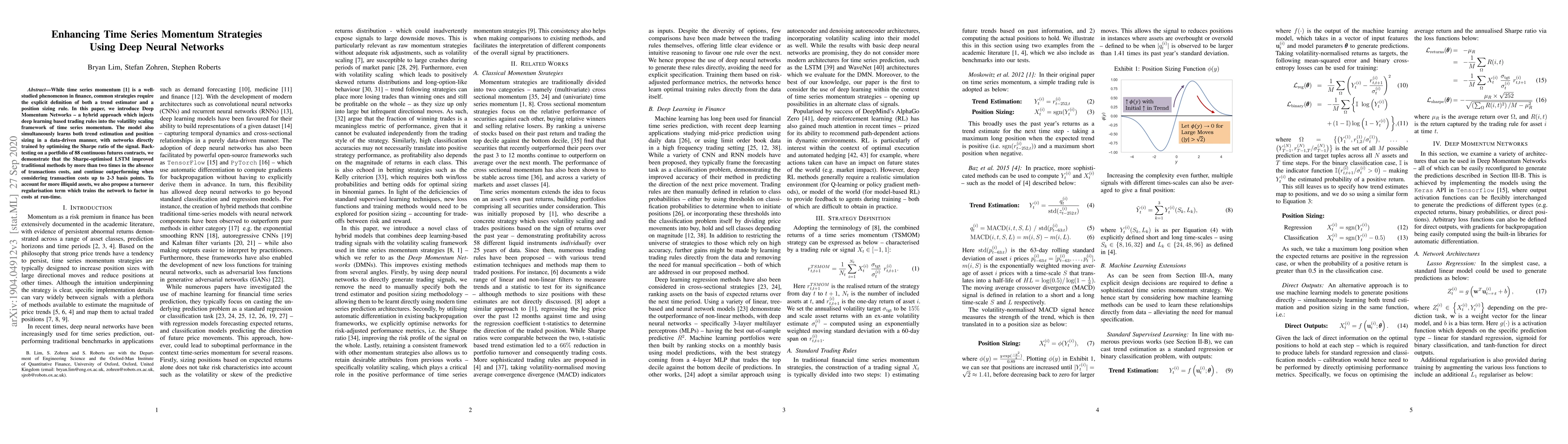

While time series momentum is a well-studied phenomenon in finance, common strategies require the explicit definition of both a trend estimator and a position sizing rule. In this paper, we introduc...

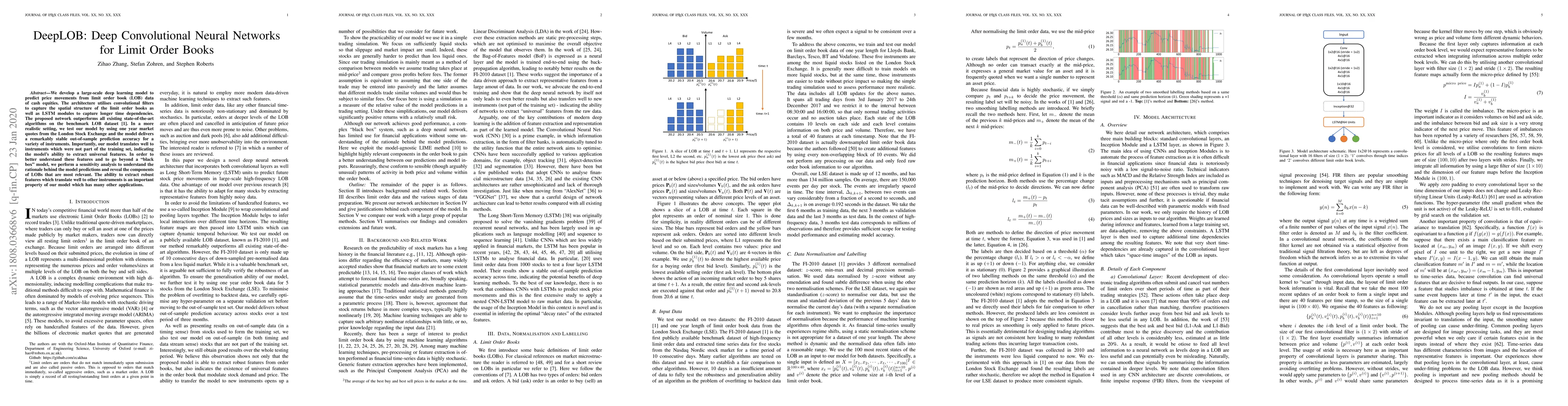

We develop a large-scale deep learning model to predict price movements from limit order book (LOB) data of cash equities. The architecture utilises convolutional filters to capture the spatial stru...

We introduce a new graphical framework for designing quantum error correction codes based on classical principles. A key feature of this graphical language, over previous approaches, is that it is c...

We introduce a novel approach to options trading strategies using a highly scalable and data-driven machine learning algorithm. In contrast to traditional approaches that often require specifications ...

Large Language Models (LLMs) have been shown to perform well for many downstream tasks. Transfer learning can enable LLMs to acquire skills that were not targeted during pre-training. In financial con...

In the era of rapid globalization and digitalization, accurate identification of similar stocks has become increasingly challenging due to the non-stationary nature of financial markets and the ambigu...

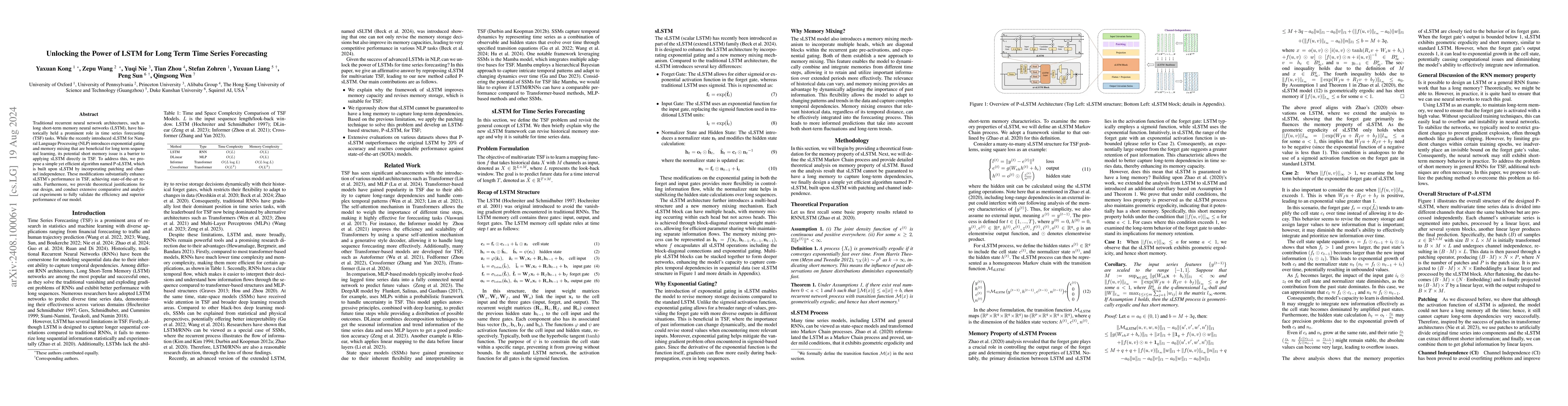

Traditional recurrent neural network architectures, such as long short-term memory neural networks (LSTM), have historically held a prominent role in time series forecasting (TSF) tasks. While the rec...

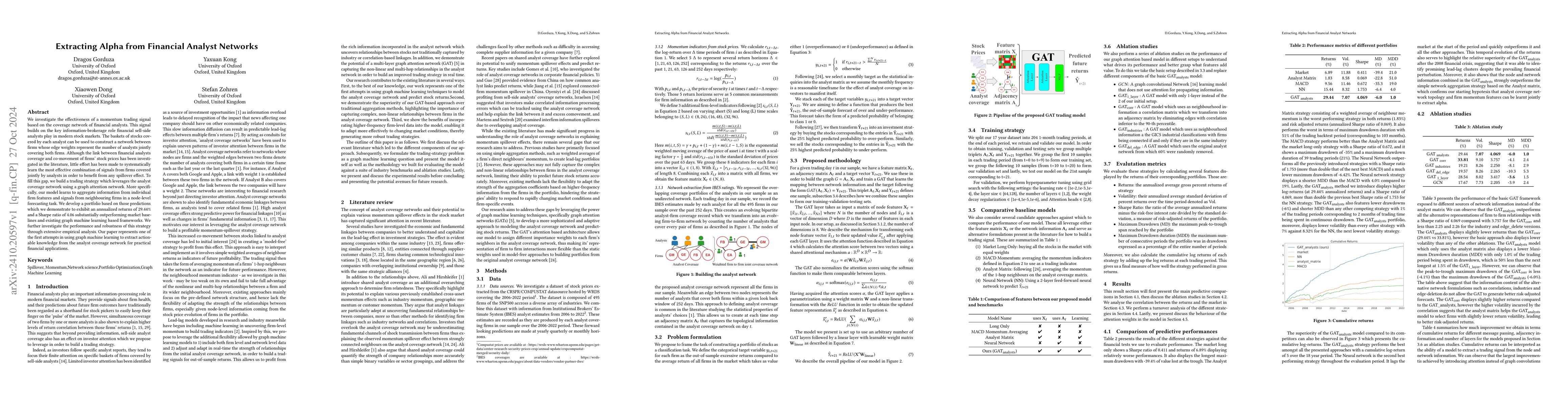

We investigate the effectiveness of a momentum trading signal based on the coverage network of financial analysts. This signal builds on the key information-brokerage role financial sell-side analysts...

While financial data presents one of the most challenging and interesting sequence modelling tasks due to high noise, heavy tails, and strategic interactions, progress in this area has been hindered b...

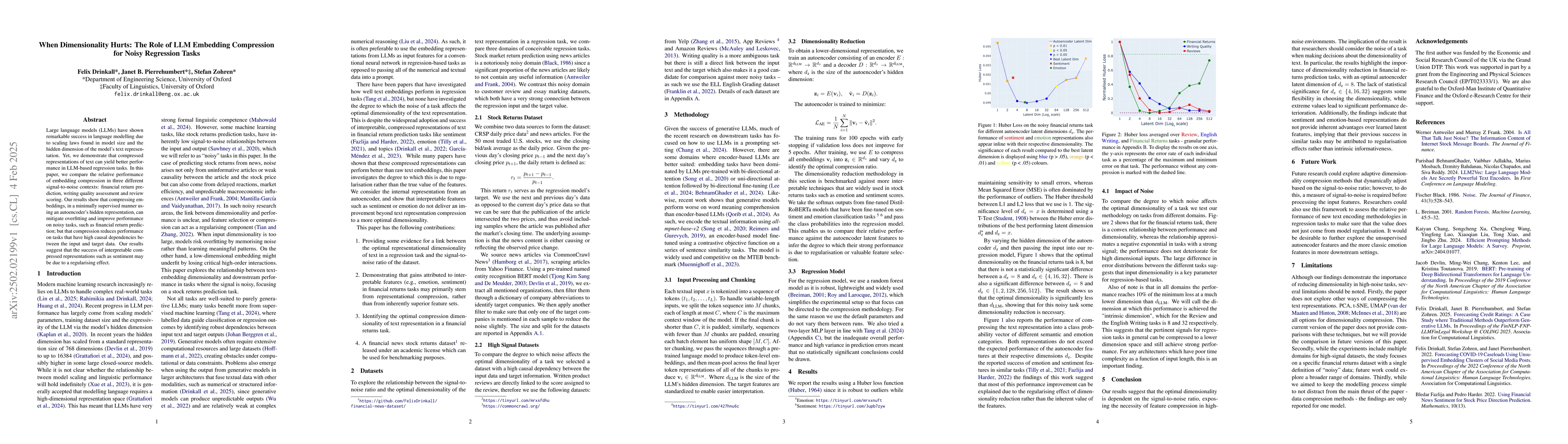

Large language models (LLMs) have shown remarkable success in language modelling due to scaling laws found in model size and the hidden dimension of the model's text representation. Yet, we demonstrat...

This paper addresses the critical disconnect between prediction and decision quality in portfolio optimization by integrating Large Language Models (LLMs) with decision-focused learning. We demonstrat...

Macroeconomic fluctuations and the narratives that shape them form a mutually reinforcing cycle: public discourse can spur behavioural changes leading to economic shifts, which then result in changes ...

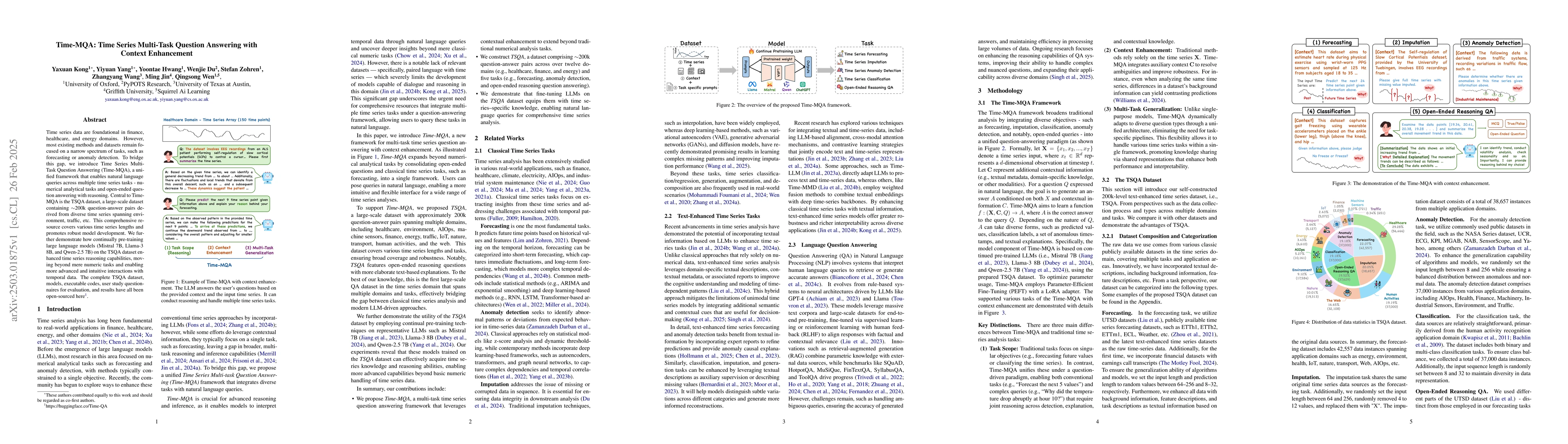

Time series data are foundational in finance, healthcare, and energy domains. However, most existing methods and datasets remain focused on a narrow spectrum of tasks, such as forecasting or anomaly d...

In the rapidly evolving world of financial markets, understanding the dynamics of limit order book (LOB) is crucial for unraveling market microstructure and participant behavior. We introduce ClusterL...

A principal concern in the optimisation of parametrised quantum circuits is the presence of barren plateaus, which present fundamental challenges to the scalability of applications, such as variationa...

Simulating limit order books (LOBs) has important applications across forecasting and backtesting for financial market data. However, deep generative models struggle in this context due to the high no...

Robust asset allocation is a key challenge in quantitative finance, where deep-learning forecasters often fail due to objective mismatch and error amplification. We introduce the Signature-Informed Tr...

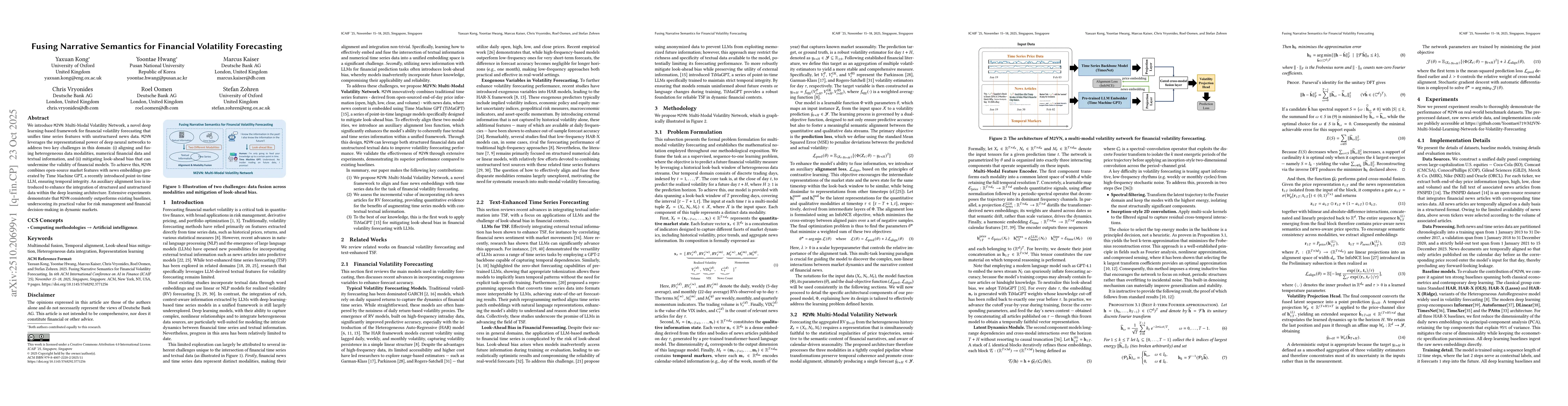

We introduce M2VN: Multi-Modal Volatility Network, a novel deep learning-based framework for financial volatility forecasting that unifies time series features with unstructured news data. M2VN levera...

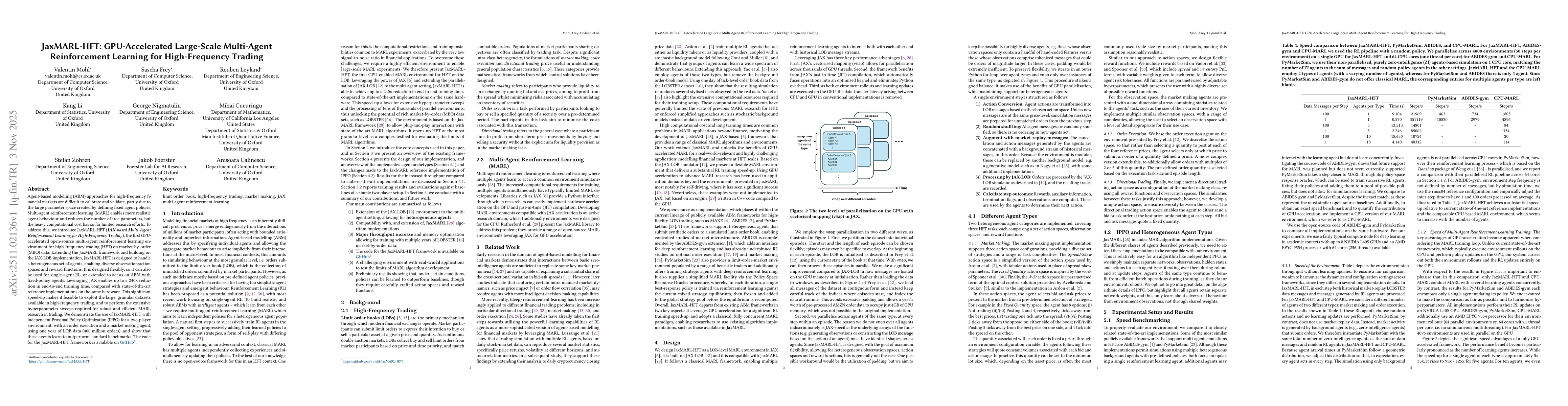

Agent-based modelling (ABM) approaches for high-frequency financial markets are difficult to calibrate and validate, partly due to the large parameter space created by defining fixed agent policies. M...

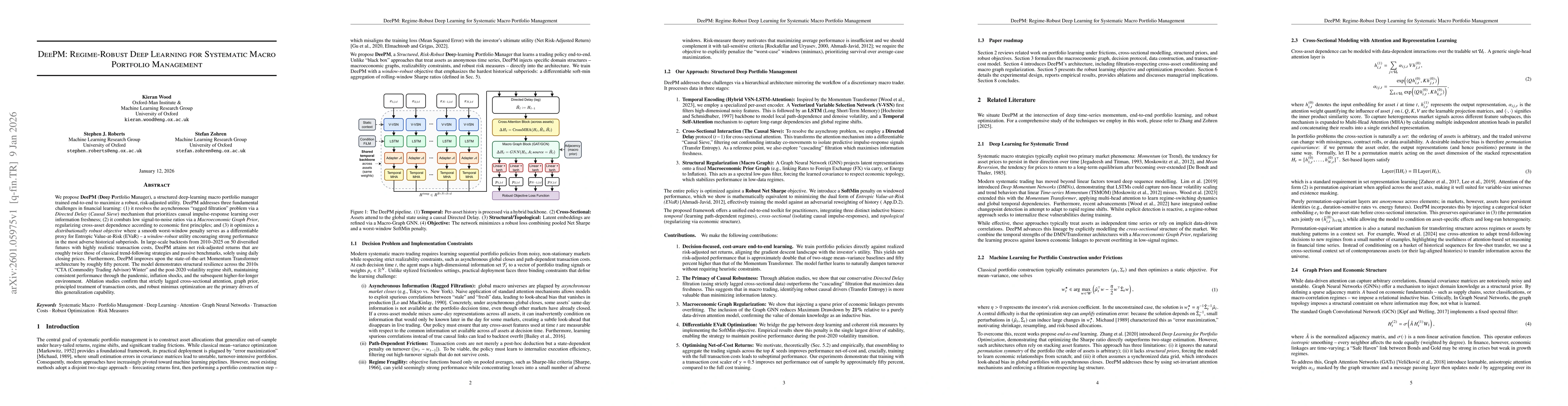

We propose DeePM (Deep Portfolio Manager), a structured deep-learning macro portfolio manager trained end-to-end to maximize a robust, risk-adjusted utility. DeePM addresses three fundamental challeng...

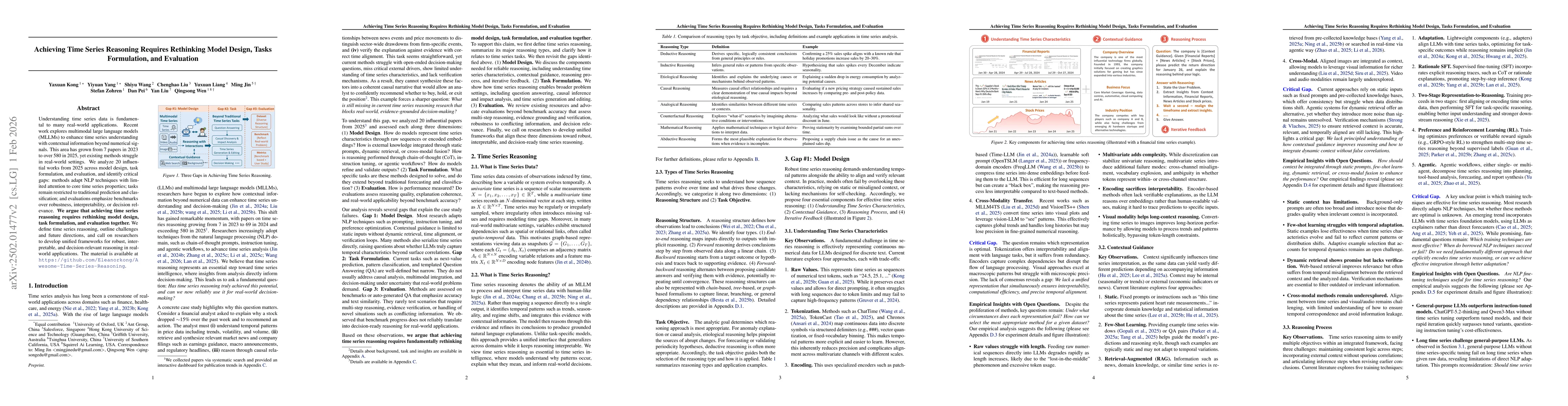

Understanding time series data is fundamental to many real-world applications. Recent work explores multimodal large language models (MLLMs) to enhance time series understanding with contextual inform...

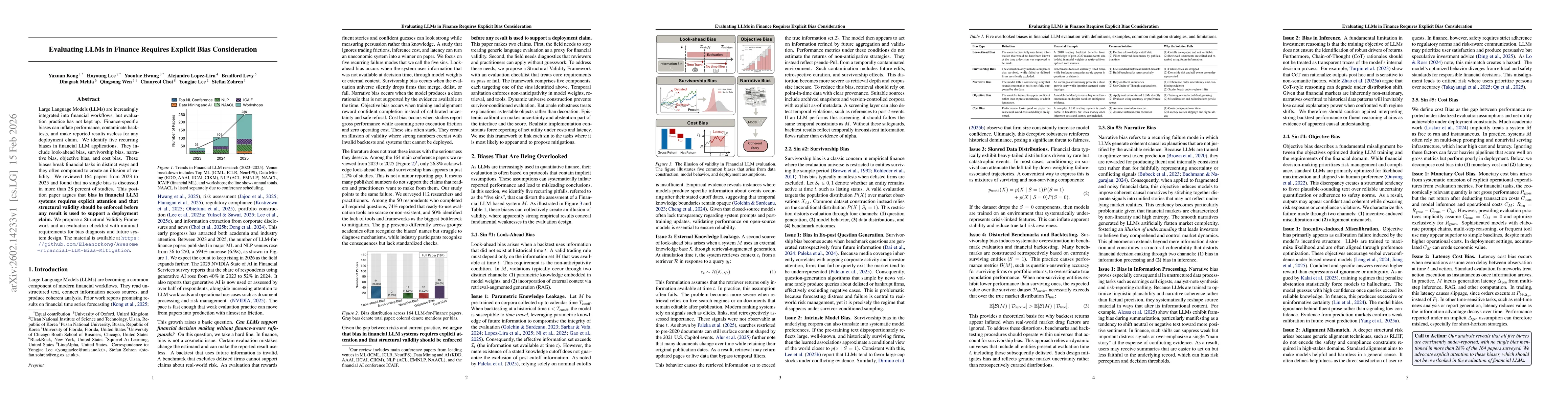

Large Language Models (LLMs) are increasingly integrated into financial workflows, but evaluation practice has not kept up. Finance-specific biases can inflate performance, contaminate backtests, and ...

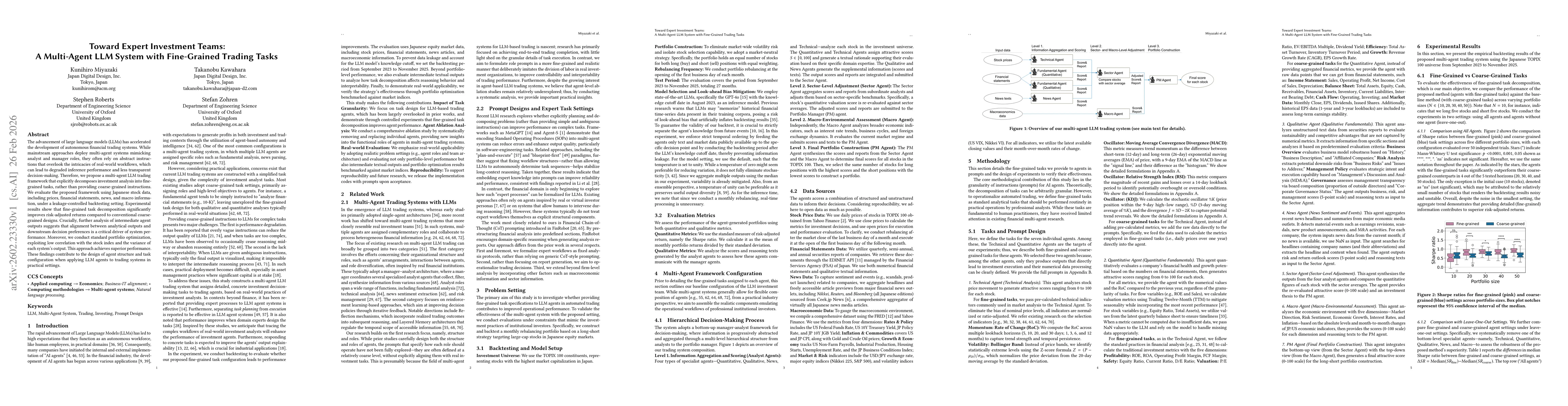

The advancement of large language models (LLMs) has accelerated the development of autonomous financial trading systems. While mainstream approaches deploy multi-agent systems mimicking analyst and ma...

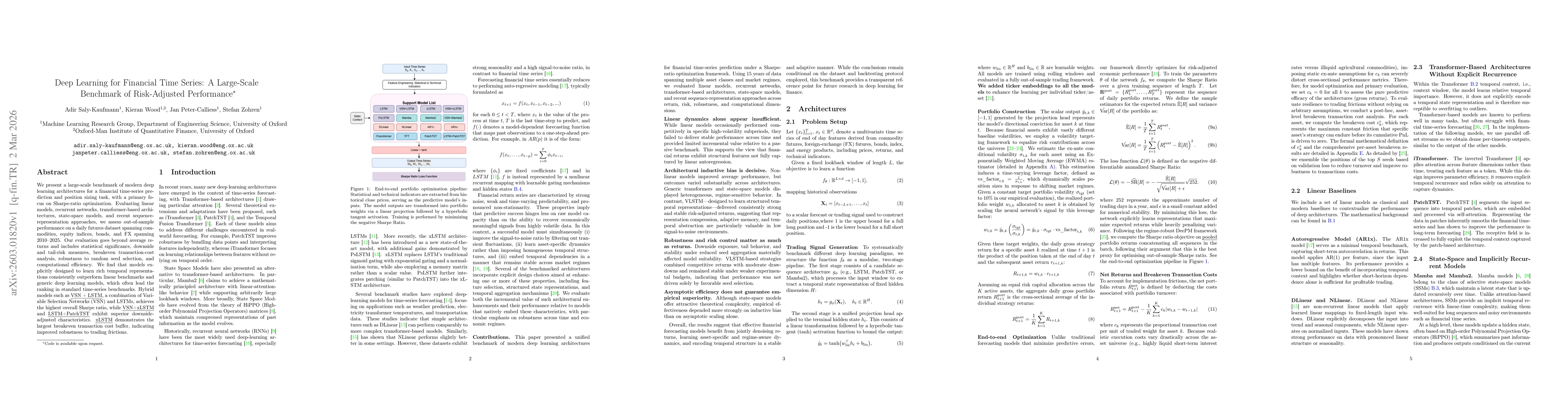

We present a large scale benchmark of modern deep learning architectures for a financial time series prediction and position sizing task, with a primary focus on Sharpe ratio optimization. Evaluating ...

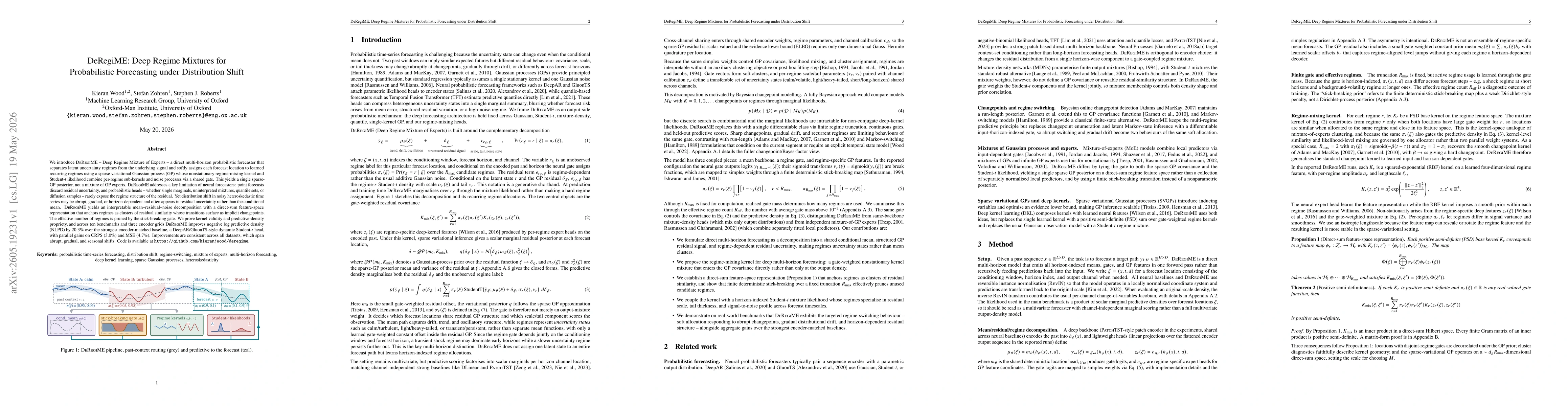

We introduce DeRegiME -- Deep Regime Mixture of Experts -- a direct multi-horizon probabilistic forecaster that separates latent uncertainty regimes from the underlying signal and softly assigns each ...

Deep learning models show promise in financial forecasting, yet their generalization is often undermined by small datasets, noisy signals, and non-stationarity. While meta-learning and related techniq...

Time series data inform critical decisions across many real-world domains. While large language model (LLM) agents can analyze data through natural language and tools, it remains unclear whether they ...