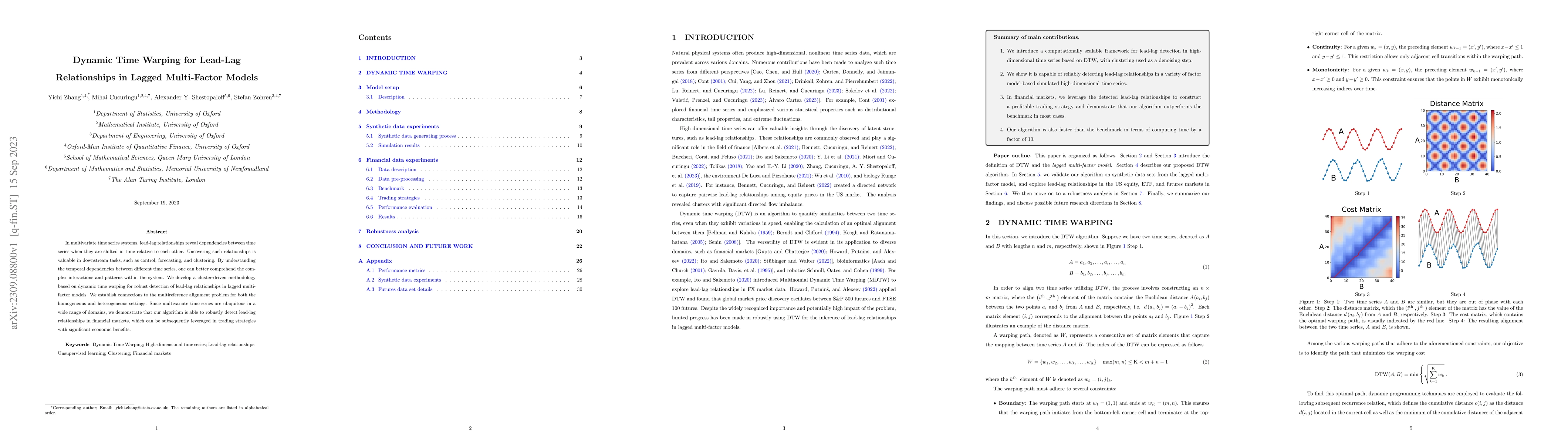

Dynamic Time Warping for Lead-Lag Relationships in Lagged Multi-Factor Models

Publication

Metrics

AI Quick Summary

This paper proposes a dynamic time warping-based methodology for detecting lead-lag relationships in multivariate time series data, crucial for understanding temporal dependencies in systems. The method is demonstrated to robustly identify these relationships in financial markets, potentially enhancing trading strategies.

Paper Preview

Abstract

In multivariate time series systems, lead-lag relationships reveal dependencies between time series when they are shifted in time relative to each other. Uncovering such relationships is valuable in downstream tasks, such as control, forecasting, and clustering. By understanding the temporal dependencies between different time series, one can better comprehend the complex interactions and patterns within the system. We develop a cluster-driven methodology based on dynamic time warping for robust detection of lead-lag relationships in lagged multi-factor models. We establish connections to the multireference alignment problem for both the homogeneous and heterogeneous settings. Since multivariate time series are ubiquitous in a wide range of domains, we demonstrate that our algorithm is able to robustly detect lead-lag relationships in financial markets, which can be subsequently leveraged in trading strategies with significant economic benefits.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0