Academic Profile

Statistics

Similar Authors

Papers on arXiv

Conformal prediction is a non-parametric technique for constructing prediction intervals or sets from arbitrary predictive models under the assumption that the data is exchangeable. It is popular as i...

Given an undirected measurement graph $\mathcal{H} = ([n], \mathcal{E})$, the classical angular synchronization problem consists of recovering unknown angles $\theta_1^*,\dots,\theta_n^*$ from a col...

This paper studies the directed graph clustering problem through the lens of statistics, where we formulate clustering as estimating underlying communities in the directed stochastic block model (DS...

For analysing real-world networks, graph representation learning is a popular tool. These methods, such as a graph autoencoder (GAE), typically rely on low-dimensional representations, also called e...

The angular synchronization problem aims to accurately estimate (up to a constant additive phase) a set of unknown angles $\theta_1, \dots, \theta_n\in[0, 2\pi)$ from $m$ noisy measurements of their...

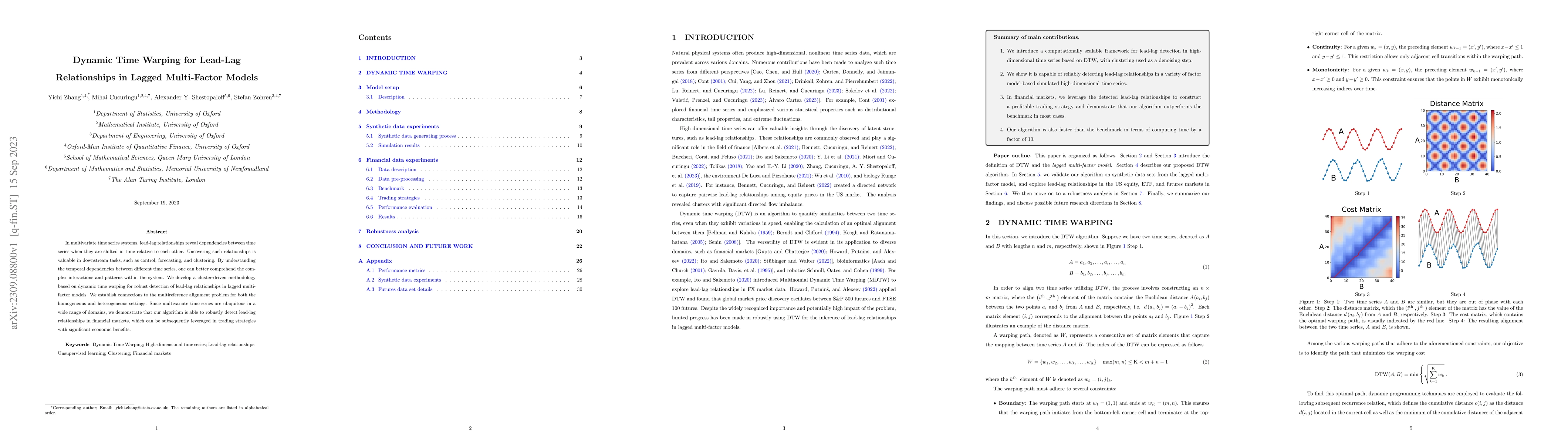

In multivariate time series systems, lead-lag relationships reveal dependencies between time series when they are shifted in time relative to each other. Uncovering such relationships is valuable in...

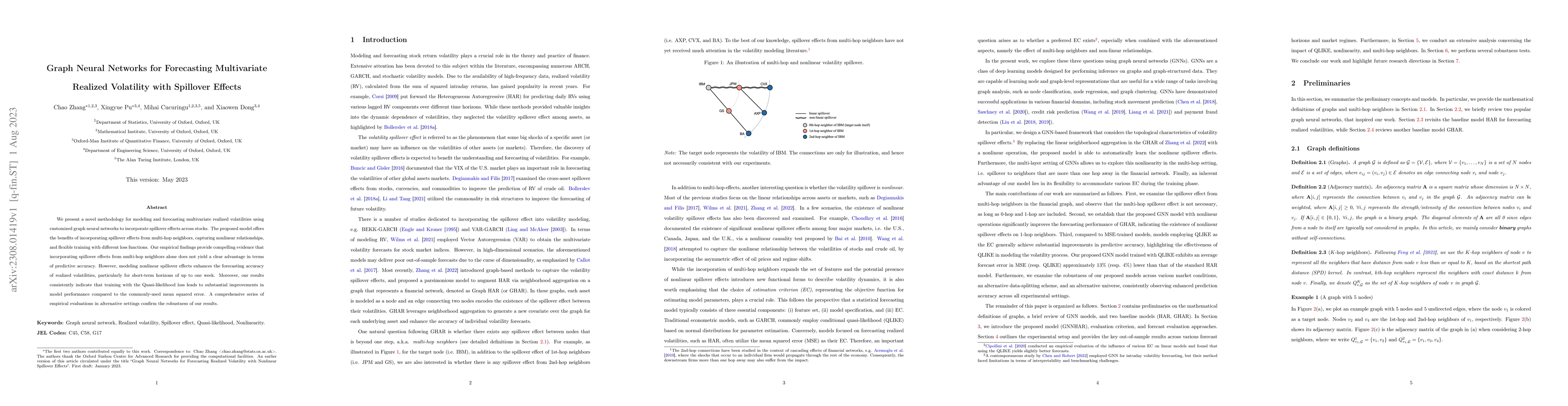

We present a novel methodology for modeling and forecasting multivariate realized volatilities using customized graph neural networks to incorporate spillover effects across stocks. The proposed mod...

Over recent years, denoising diffusion generative models have come to be considered as state-of-the-art methods for synthetic data generation, especially in the case of generating images. These appr...

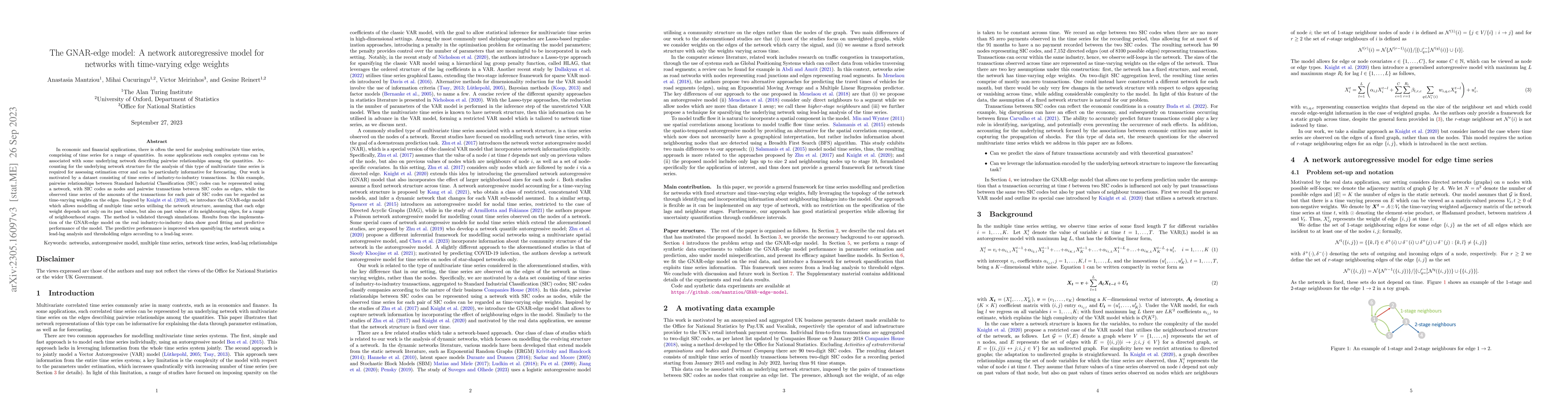

In economic and financial applications, there is often the need for analysing multivariate time series, comprising of time series for a range of quantities. In some applications such complex systems...

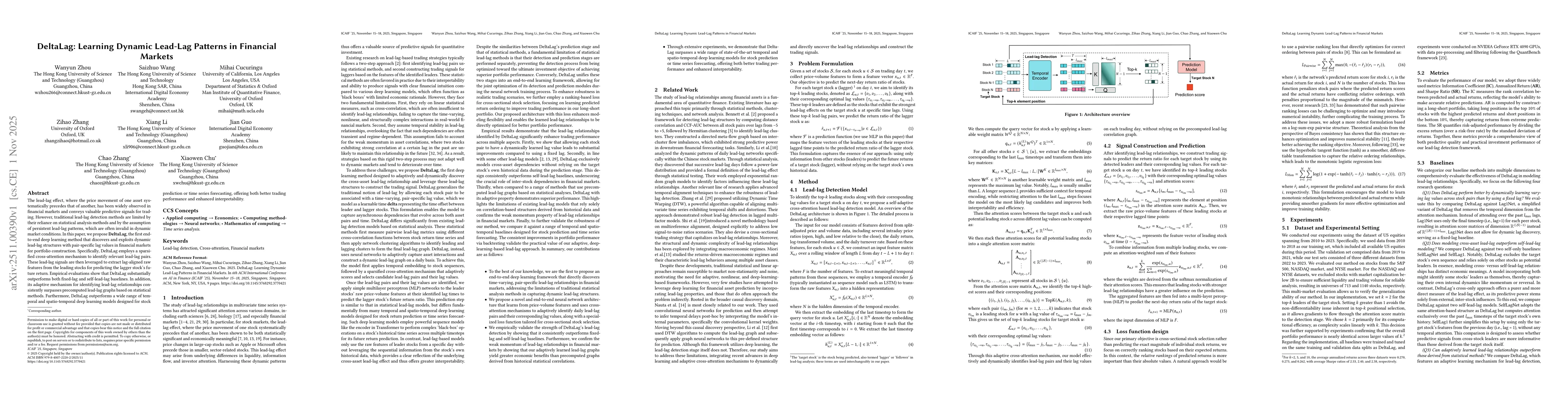

In multivariate time series systems, key insights can be obtained by discovering lead-lag relationships inherent in the data, which refer to the dependence between two time series shifted in time re...

We introduce OFTER, a time series forecasting pipeline tailored for mid-sized multivariate time series. OFTER utilizes the non-parametric models of k-nearest neighbors and Generalized Regression Neu...

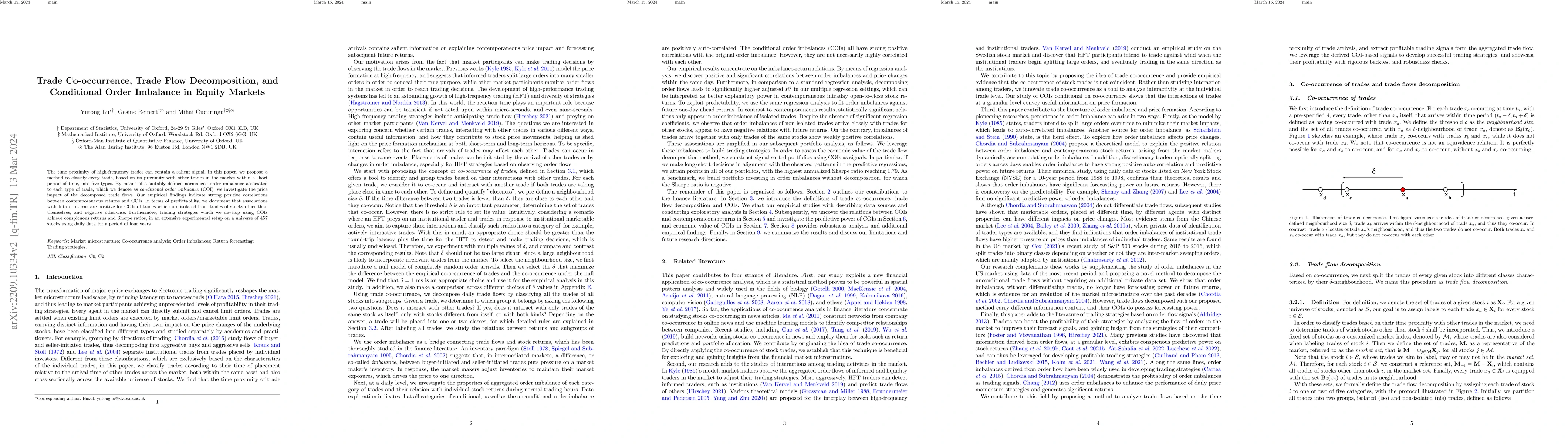

The time proximity of trades across stocks reveals interesting topological structures of the equity market in the United States. In this article, we investigate how such concurrent cross-stock tradi...

Uniswap is a Constant Product Market Maker built around liquidity pools, where pairs of tokens are exchanged subject to a fee that is proportional to the size of transactions. At the time of writing...

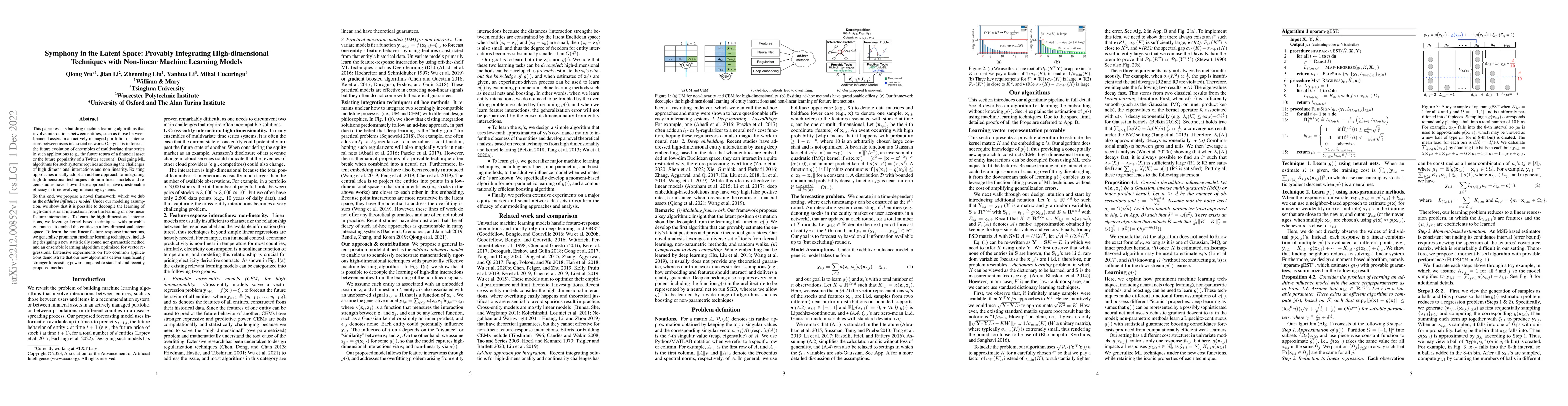

This paper revisits building machine learning algorithms that involve interactions between entities, such as those between financial assets in an actively managed portfolio, or interactions between ...

The time proximity of high-frequency trades can contain a salient signal. In this paper, we propose a method to classify every trade, based on its proximity with other trades in the market within a ...

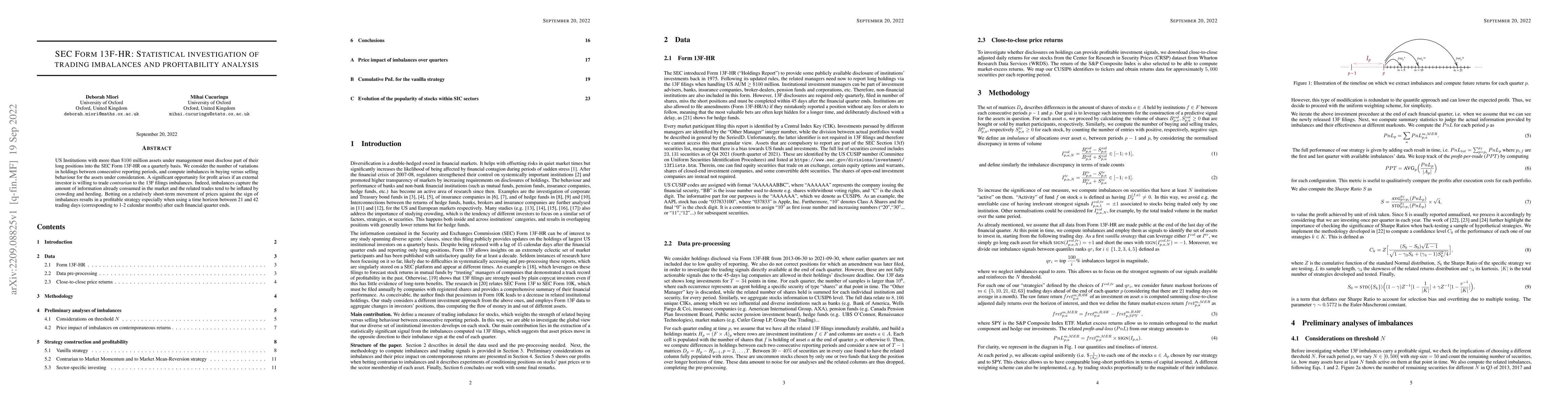

US Institutions with more than $100 million assets under management must disclose part of their long positions into the SEC Form 13F-HR on a quarterly basis. We consider the number of variations in ...

Signed and directed networks are ubiquitous in real-world applications. However, there has been relatively little work proposing spectral graph neural networks (GNNs) for such networks. Here we intr...

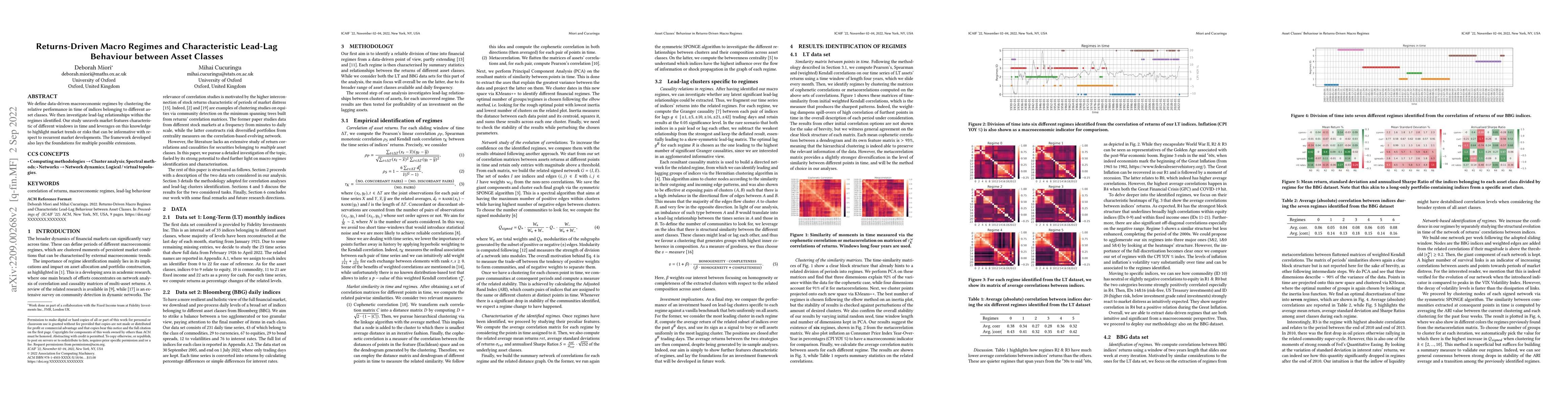

We define data-driven macroeconomic regimes by clustering the relative performance in time of indices belonging to different asset classes. We then investigate lead-lag relationships within the regi...

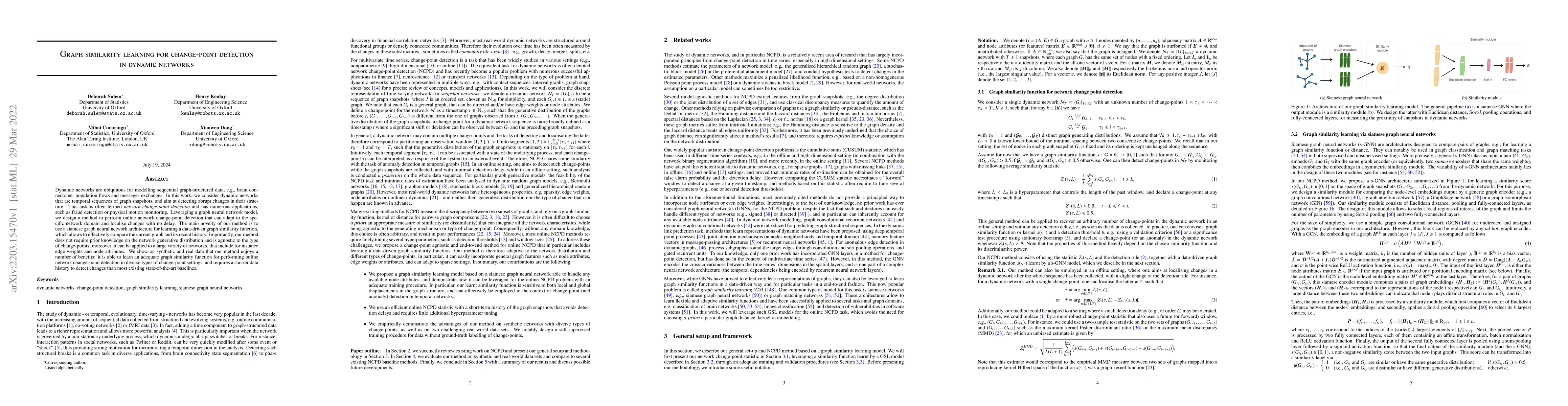

Dynamic networks are ubiquitous for modelling sequential graph-structured data, e.g., brain connectome, population flows and messages exchanges. In this work, we consider dynamic networks that are t...

Generative models for network time series (also known as dynamic graphs) have tremendous potential in fields such as epidemiology, biology and economics, where complex graph-based dynamics are core ...

The estimation of loss distributions for dynamic portfolios requires the simulation of scenarios representing realistic joint dynamics of their components, with particular importance devoted to the ...

Networks are ubiquitous in many real-world applications (e.g., social networks encoding trust/distrust relationships, correlation networks arising from time series data). While many networks are sig...

We apply machine learning models to forecast intraday realized volatility (RV), by exploiting commonality in intraday volatility via pooling stock data together, and by incorporating a proxy for the...

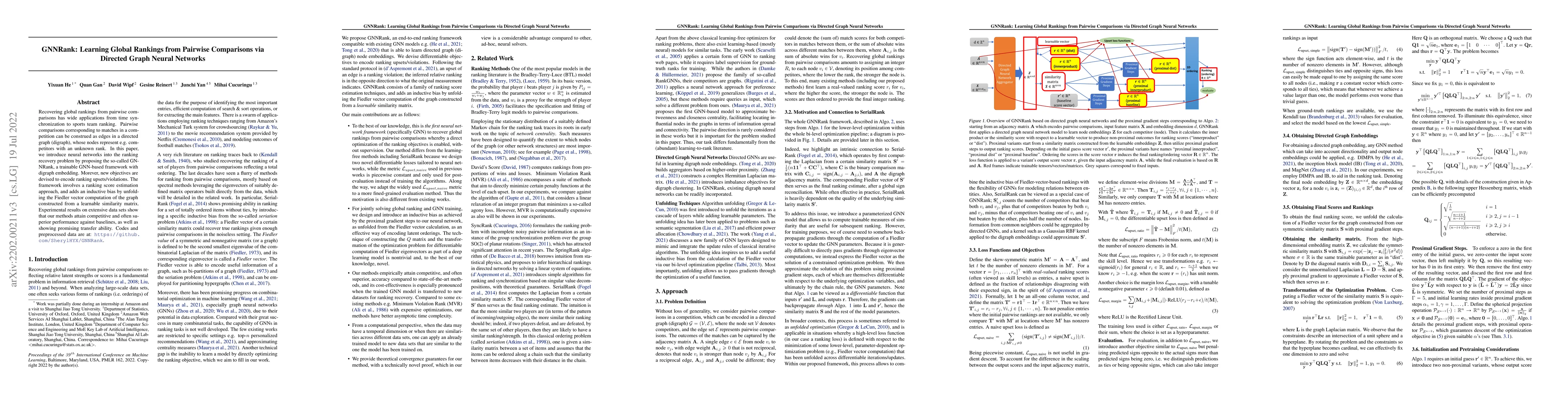

Recovering global rankings from pairwise comparisons has wide applications from time synchronization to sports team ranking. Pairwise comparisons corresponding to matches in a competition can be con...

We investigate the use of the normalized imbalance between option volumes corresponding to positive and negative market views, as a predictor for directional price movements in the spot market. Via ...

In multivariate time series systems, it has been observed that certain groups of variables partially lead the evolution of the system, while other variables follow this evolution with a time delay; ...

We propose a decentralised "local2global"' approach to graph representation learning, that one can a-priori use to scale any embedding technique. Our local2global approach proceeds by first dividing...

We investigate the impact of order flow imbalance (OFI) on price movements in equity markets in a multi-asset setting. First, we propose a systematic approach for combining OFIs at the top levels of...

We propose a universal end-to-end framework for portfolio optimization where asset distributions are directly obtained. The designed framework circumvents the traditional forecasting step and avoids...

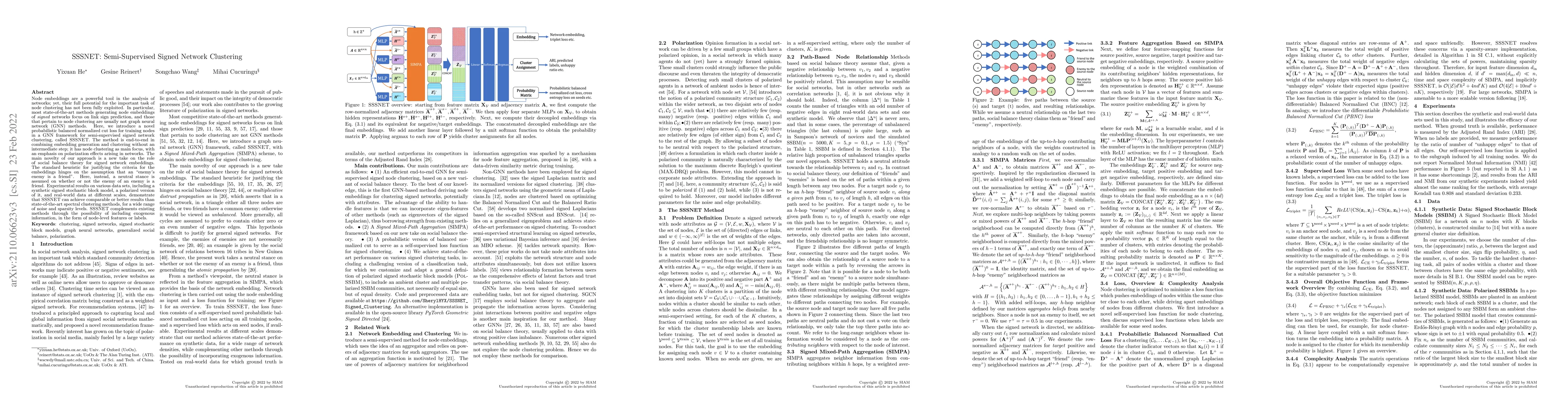

Node embeddings are a powerful tool in the analysis of networks; yet, their full potential for the important task of node clustering has not been fully exploited. In particular, most state-of-the-ar...

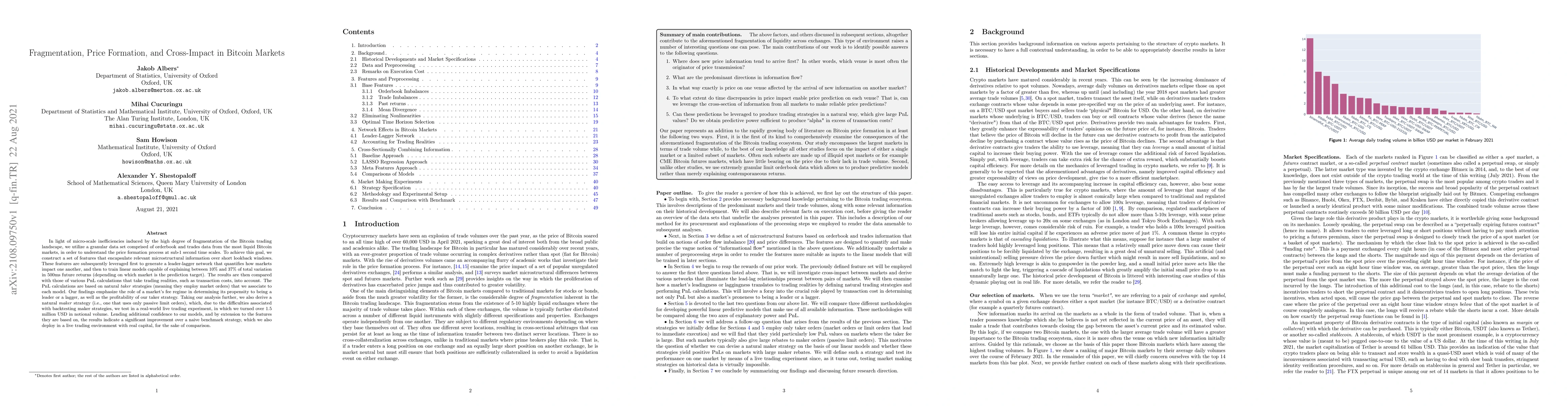

In light of micro-scale inefficiencies induced by the high degree of fragmentation of the Bitcoin trading landscape, we utilize a granular data set comprised of orderbook and trades data from the mo...

We propose a decentralised "local2global" approach to graph representation learning, that one can a-priori use to scale any embedding technique. Our local2global approach proceeds by first dividing ...

Lexical semantic change (detecting shifts in the meaning and usage of words) is an important task for social and cultural studies as well as for Natural Language Processing applications. Diachronic ...

Node clustering is a powerful tool in the analysis of networks. We introduce a graph neural network framework, named DIGRAC, to obtain node embeddings for directed networks in a self-supervised mann...

We study the problem of $k$-way clustering in signed graphs. Considerable attention in recent years has been devoted to analyzing and modeling signed graphs, where the affinity measure between nodes...

The transportation $\mathrm{L}^p$ distance, denoted $\mathrm{TL}^p$, has been proposed as a generalisation of Wasserstein $\mathrm{W}^p$ distances motivated by the property that it can be applied di...

We consider spectral approaches to the problem of ranking n players given their incomplete and noisy pairwise comparisons, but revisit this classical problem in light of player covariate information...

Many statistical learning problems have recently been shown to be amenable to Semi-Definite Programming (SDP), with community detection and clustering in Gaussian mixture models as the most striking...

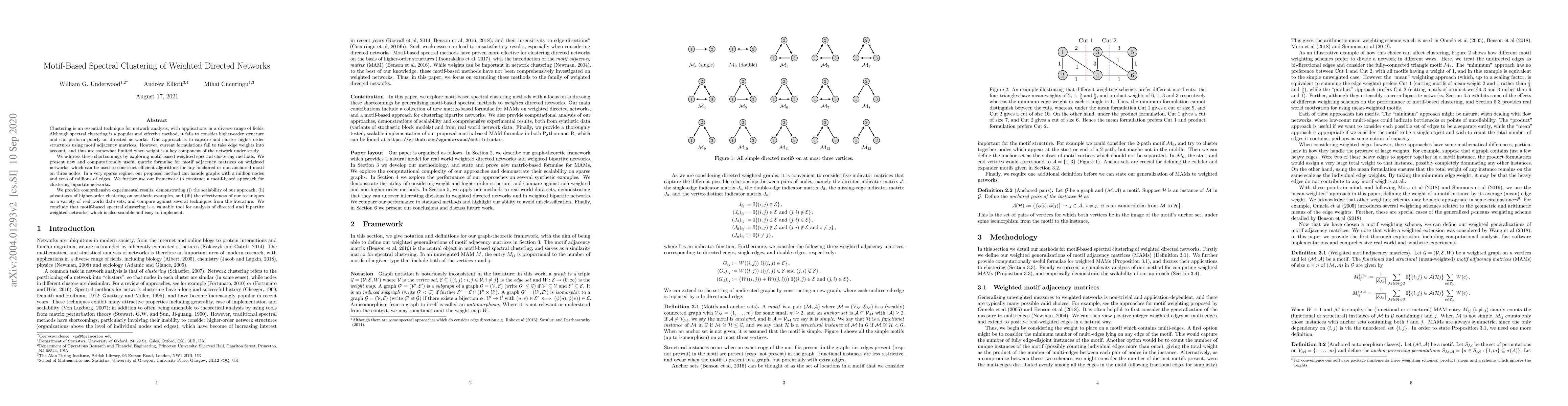

Clustering is an essential technique for network analysis, with applications in a diverse range of fields. Although spectral clustering is a popular and effective method, it fails to consider higher...

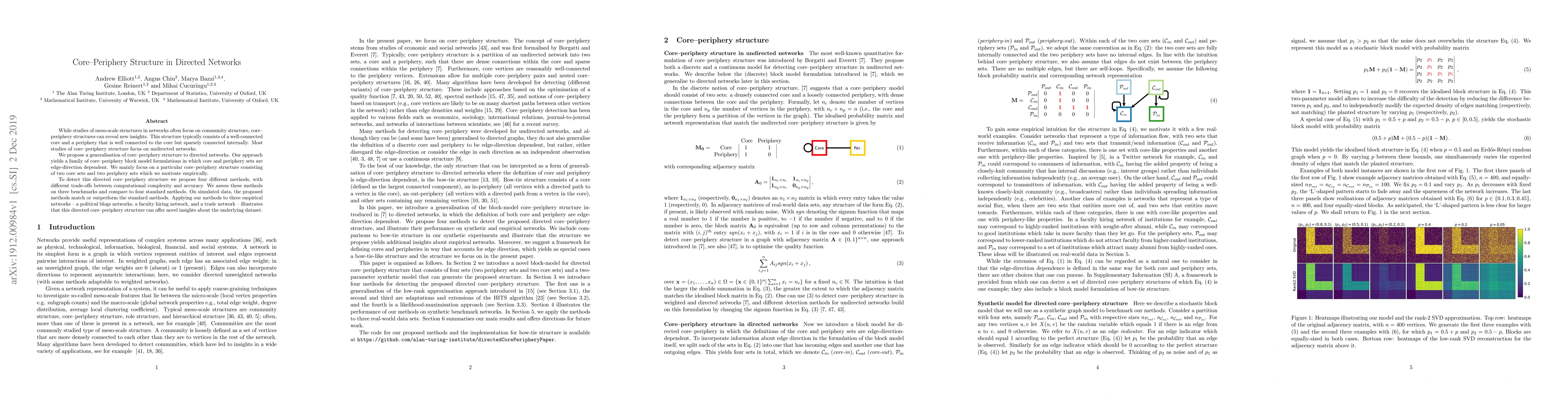

While studies of meso-scale structures in networks often focus on community structure, core--periphery structures can reveal new insights. This structure typically consists of a well-connected core ...

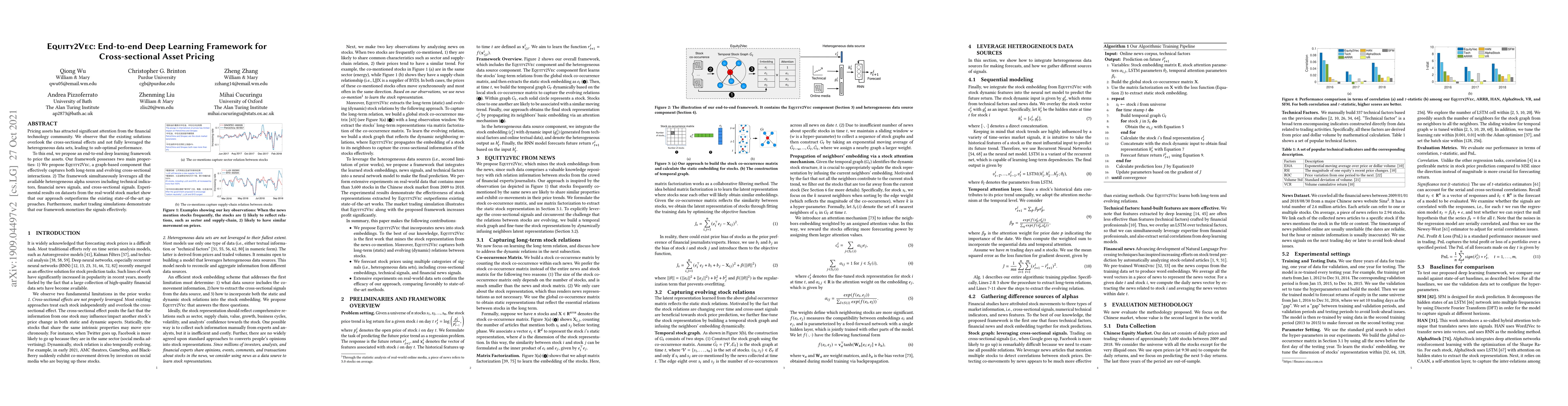

Pricing assets has attracted significant attention from the financial technology community. We observe that the existing solutions overlook the cross-sectional effects and not fully leveraged the he...

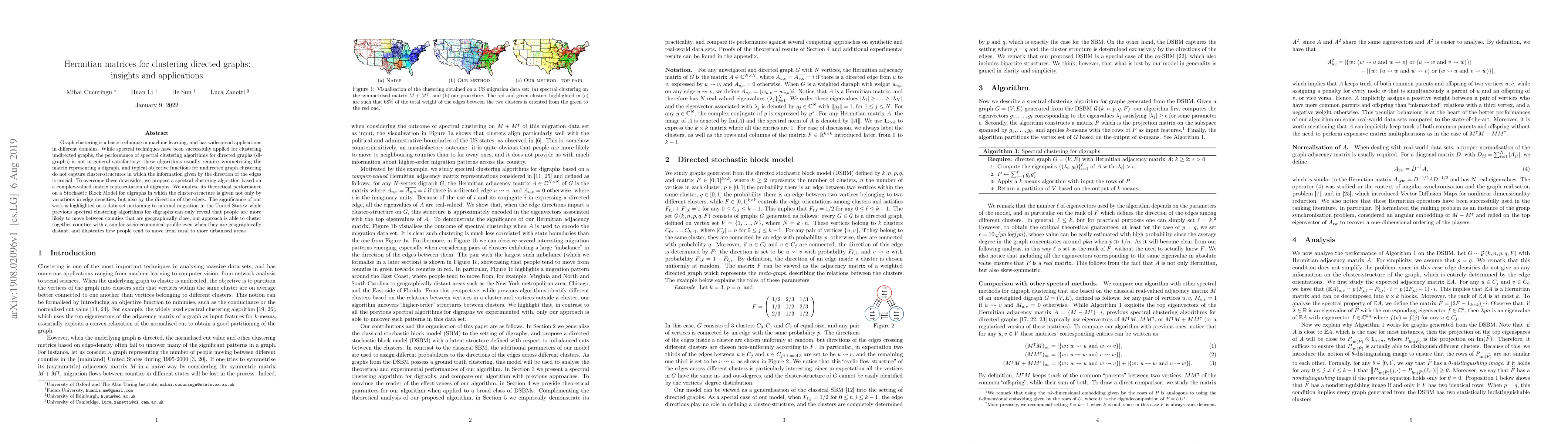

Graph clustering is a basic technique in machine learning, and has widespread applications in different domains. While spectral techniques have been successfully applied for clustering undirected gr...

Given a measurement graph $G= (V,E)$ and an unknown signal $r \in \mathbb{R}^n$, we investigate algorithms for recovering $r$ from pairwise measurements of the form $r_i - r_j$; $\{i,j\} \in E$. Thi...

We introduce a novel framework to financial time series forecasting that leverages causality-inspired models to balance the trade-off between invariance to distributional changes and minimization of p...

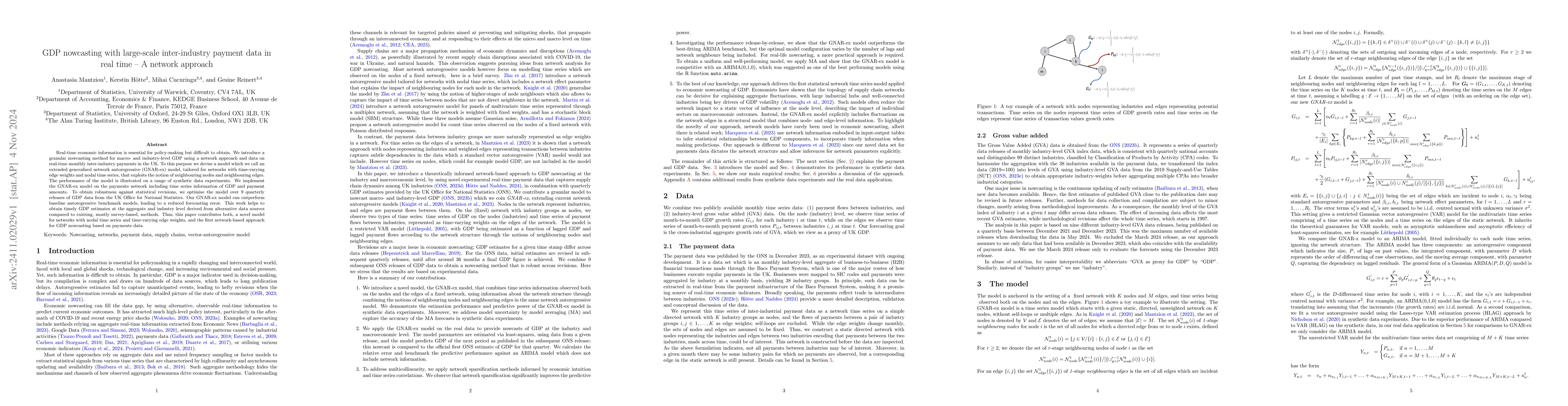

Real-time economic information is essential for policy-making but difficult to obtain. We introduce a granular nowcasting method for macro- and industry-level GDP using a network approach and data on ...

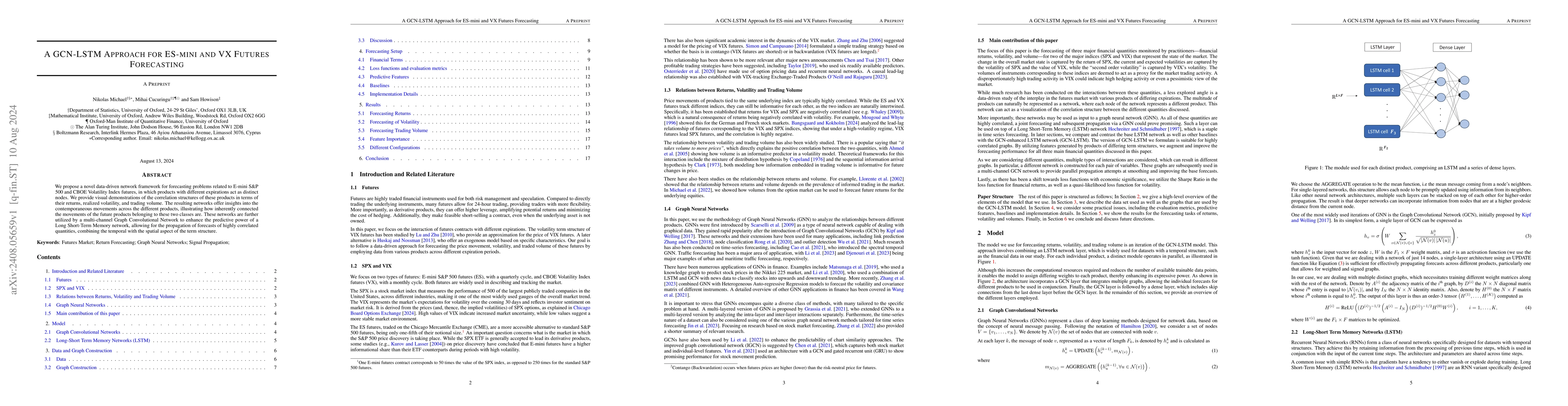

We propose a novel data-driven network framework for forecasting problems related to E-mini S\&P 500 and CBOE Volatility Index futures, in which products with different expirations act as distinct nod...

High-dimensional panels of time series arise in many scientific disciplines such as neuroscience, finance, and macroeconomics. Often, co-movements within groups of the panel components occur. Extracti...

We tackle the challenges of modeling high-dimensional data sets, particularly those with latent low-dimensional structures hidden within complex, non-linear, and noisy relationships. Our approach enab...

Working at a very granular level, using data from a live trading experiment on the Binance linear Bitcoin perpetual-the most liquid crypto market worldwide-we examine the effects of (i) basic order bo...

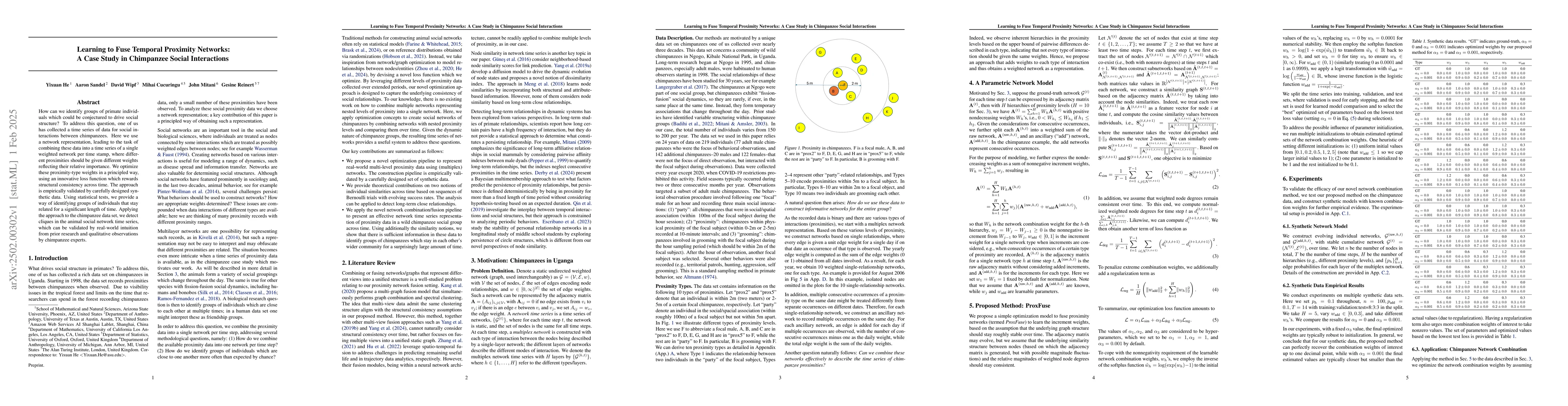

How can we identify groups of primate individuals which could be conjectured to drive social structure? To address this question, one of us has collected a time series of data for social interactions ...

This paper extends the tactical asset allocation literature by incorporating regime modeling using techniques from machine learning. We propose a novel model that classifies current regimes, forecasts...

In the rapidly evolving world of financial markets, understanding the dynamics of limit order book (LOB) is crucial for unraveling market microstructure and participant behavior. We introduce ClusterL...

This study focuses on forecasting intraday trading volumes, a crucial component for portfolio implementation, especially in high-frequency (HF) trading environments. Given the current scarcity of flex...

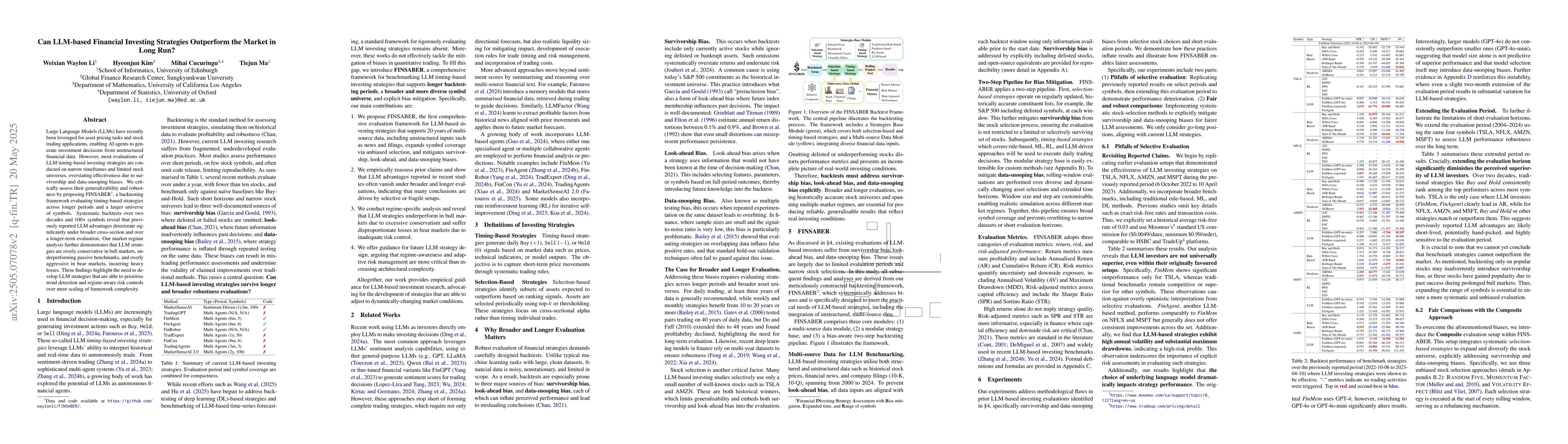

Large Language Models (LLMs) have recently been leveraged for asset pricing tasks and stock trading applications, enabling AI agents to generate investment decisions from unstructured financial data. ...

Graph convolutional neural networks (GCNNs) have emerged as powerful tools for analyzing graph-structured data, achieving remarkable success across diverse applications. However, the theoretical under...

High-dimensional financial time series often exhibit complex dependence relations driven by both common market structures and latent connections among assets. To capture these characteristics, this pa...

The lead-lag effect, where the price movement of one asset systematically precedes that of another, has been widely observed in financial markets and conveys valuable predictive signals for trading. H...

Agent-based modelling (ABM) approaches for high-frequency financial markets are difficult to calibrate and validate, partly due to the large parameter space created by defining fixed agent policies. M...

We introduce Adaptive Spectral Shaping, a data-driven framework for graph filtering that learns a reusable baseline spectral kernel and modulates it with a small set of Gaussian factors. The resulting...

This paper studies cross-market return predictability through a machine learning framework that preserves economic structure. Exploiting the non-overlapping trading hours of the U.S. and Chinese equit...

Deep learning models show promise in financial forecasting, yet their generalization is often undermined by small datasets, noisy signals, and non-stationarity. While meta-learning and related techniq...

Real temporal interaction streams carry predictive structure in short-horizon motif patterns -- repetition, reciprocity, star diversity, triadic flow -- that vanilla temporal graph neural networks (TG...

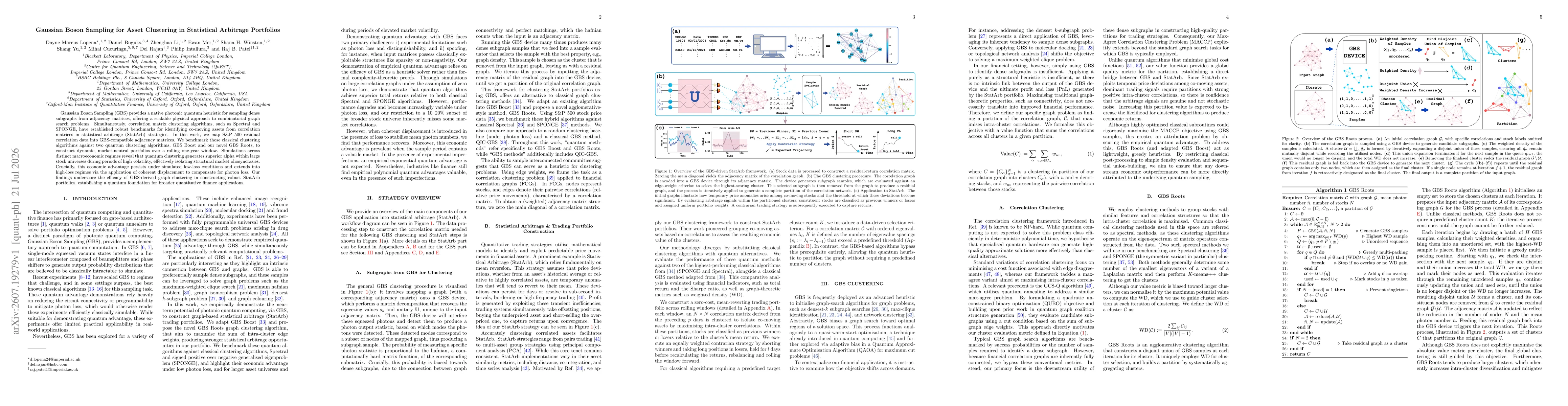

Gaussian Boson Sampling (GBS) provides a native photonic quantum heuristic for sampling dense subgraphs from adjacency matrices, offering a scalable physical approach to combinatorial graph search pro...