Academic Profile

Statistics

Similar Authors

Papers on arXiv

The IFRS 9 accounting standard requires the prediction of credit deterioration in financial instruments, i.e., significant increases in credit risk (SICR). However, the definition of such a SICR-eve...

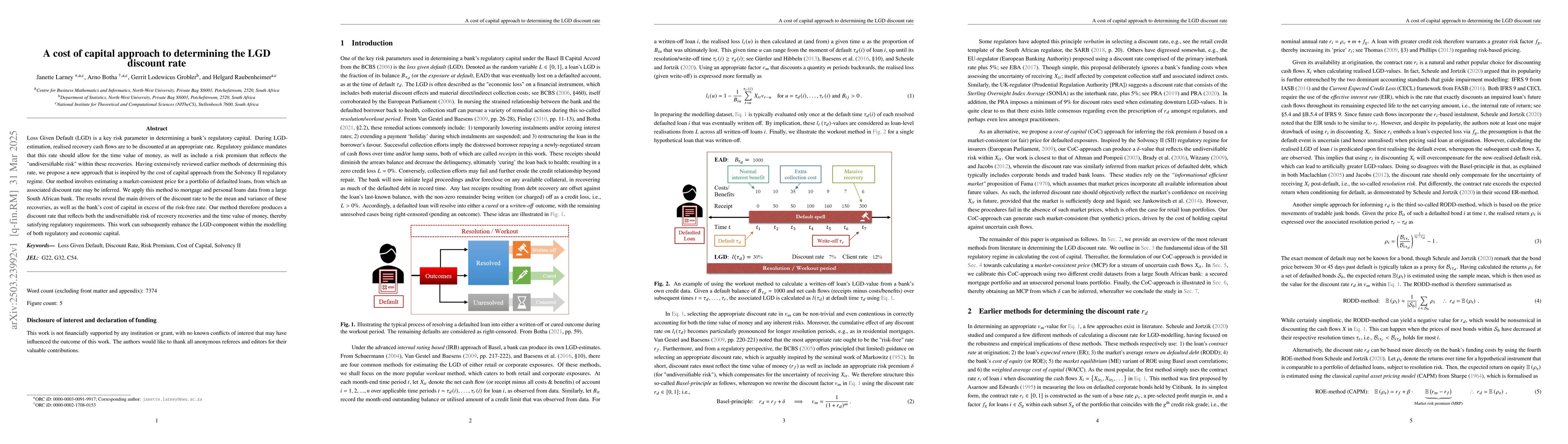

Loss Given Default (LGD) is a key risk parameter in determining a bank's regulatory capital. During LGD-estimation, realised recovery cash flows are to be discounted at an appropriate rate. Regulatory...

The estimation of marginal loan write-off probabilities is a non-trivial task when modelling the loss given default (LGD) risk parameter in credit risk. We explore two types of survival models in esti...