Academic Profile

Statistics

Similar Authors

Papers on arXiv

We design a fully implementable scheme to compute the invariant distribution of ergodic McKean-Vlasov SDE satisfying a uniform confluence property. Under natural conditions, we prove various converg...

We consider the multiple quantile hedging problem, which is a class of partial hedging problems containing as special examples the quantile hedging problem (F{\"o}llmer \& Leukert 1999) and the PnL ...

We study how the climate transition through a low-carbon economy, implemented by carbon pricing, propagates in a credit portfolio and precisely describe how carbon price dynamics affects credit risk...

We propose a new probabilistic scheme which combines deep learning techniques with high order schemes for backward stochastic differential equations belonging to the class of Runge-Kutta methods to ...

We study an implementation of the theoretical splitting scheme introduced in [Chassagneux and Yang, 2022] for singular FBSDEs [Carmona and Delarue 2013] and their associated quasi-linear degenerate ...

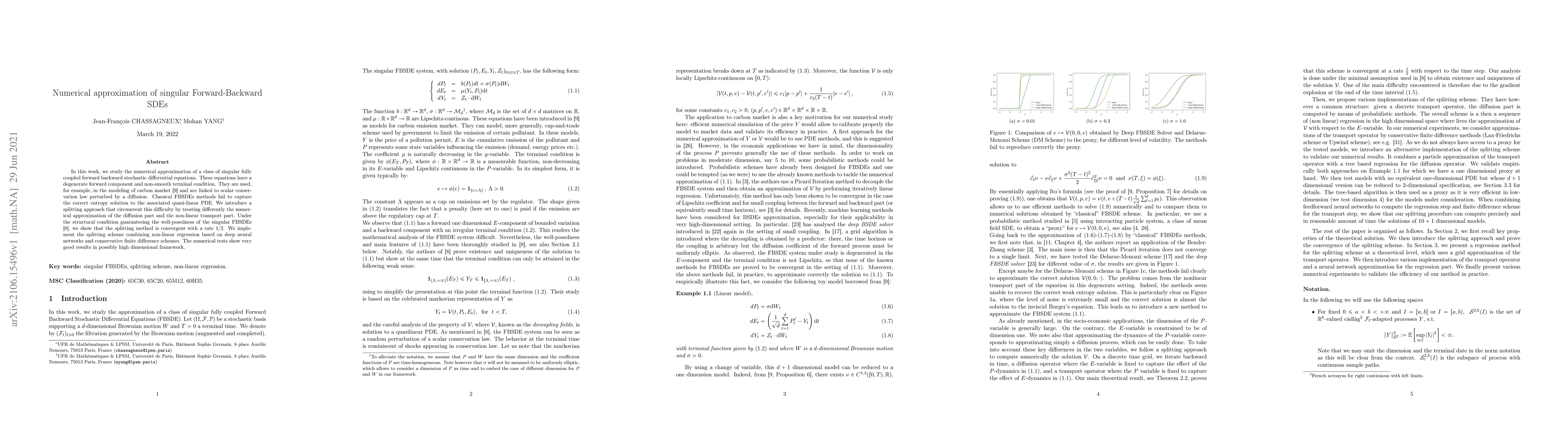

In this work, we study the numerical approximation of a class of singular fully coupled forward backward stochastic differential equations. These equations have a degenerate forward component and no...

Relying on the classical connection between Backward Stochastic Differential Equations (BSDEs) and non-linear parabolic partial differential equations (PDEs), we propose a new probabilistic learning...

This paper establishes the well-posedness of reflected backward stochastic differential equations in the non-convex domains that satisfy a weaker version of the star-shaped property. The main result...

We introduce and study a new class of optimal switching problems, namely switching problem with controlled randomisation, where some extra-randomness impacts the choice of switching modes and associ...

We consider the numerical approximation of the quantile hedging price in a non-linear market. In a Markovian framework, we propose a numerical method based on a Piecewise Constant Policy Timesteppin...

Consider the metric space $(\mathcal{P}_2(\mathbb{R}^d),W_2)$ of square integrable laws on $\mathbb{R}^d$ with the topology induced by the 2-Wasserstein distance $W_2$. Let $\Phi: \mathcal{P}_2( \ma...

In this work, we present a numerical method based on a sparse grid approximation to compute the loss distribution of the balance sheet of a financial or an insurance company. We first describe, in a...

The purpose of this paper is twofold. First, we introduce the notion of a $Γ$-martingale on a Euclidean manifold with a boundary (i.e., the closure of an open connected domain in R d ), we provide its...

The multidimensional Uncertain Volatility Model leads to robust option pricing problems under joint volatility and correlation uncertainty. Their numerical resolution quickly becomes challenging becau...

We study finite-horizon stochastic optimal control problems and approximate the resulting time-discrete formulation by a direct policy-learning problem over neural-network feedback maps. We prove a qu...