Academic Profile

Statistics

Similar Authors

Papers on arXiv

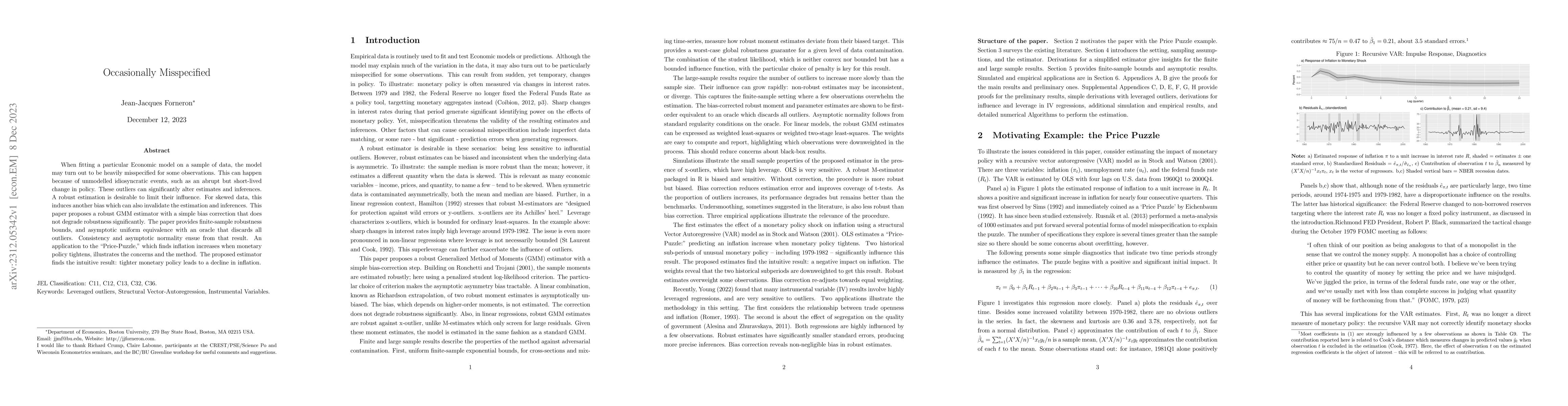

When fitting a particular Economic model on a sample of data, the model may turn out to be heavily misspecified for some observations. This can happen because of unmodelled idiosyncratic events, suc...

Generalized and Simulated Method of Moments are often used to estimate structural Economic models. Yet, it is commonly reported that optimization is challenging because the corresponding objective f...

A practical challenge for structural estimation is the requirement to accurately minimize a sample objective function which is often non-smooth, non-convex, or both. This paper proposes a simple alg...

In non-linear estimations, it is common to assess sampling uncertainty by bootstrap inference. For complex models, this can be computationally intensive. This paper combines optimization with resamp...

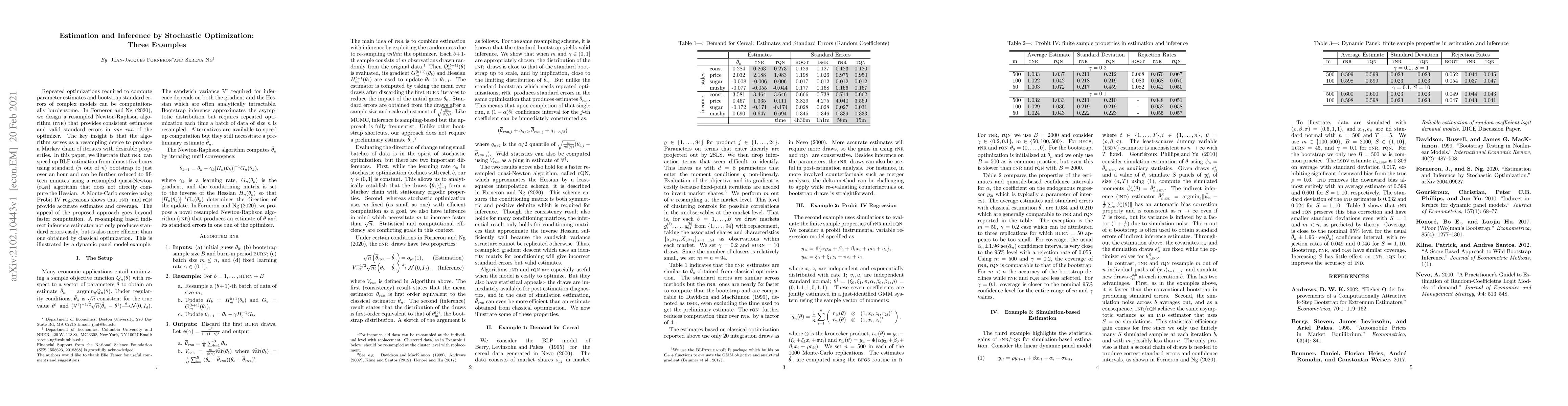

This paper illustrates two algorithms designed in Forneron & Ng (2020): the resampled Newton-Raphson (rNR) and resampled quasi-Newton (rqN) algorithms which speed-up estimation and bootstrap inferen...

Assessing sampling uncertainty in extremum estimation can be challenging when the asymptotic variance is not analytically tractable. Bootstrap inference offers a feasible solution but can be computa...

Quasi-Monte Carlo (qMC) methods are a powerful alternative to classical Monte-Carlo (MC) integration. Under certain conditions, they can approximate the desired integral at a faster rate than the us...

This paper develops an approach to detect identification failure in moment condition models. This is achieved by introducing a quasi-Jacobian matrix computed as the slope of a linear approximation o...

This paper proposes a Sieve Simulated Method of Moments (Sieve-SMM) estimator for the parameters and the distribution of the shocks in nonlinear dynamic models where the likelihood and the moments a...

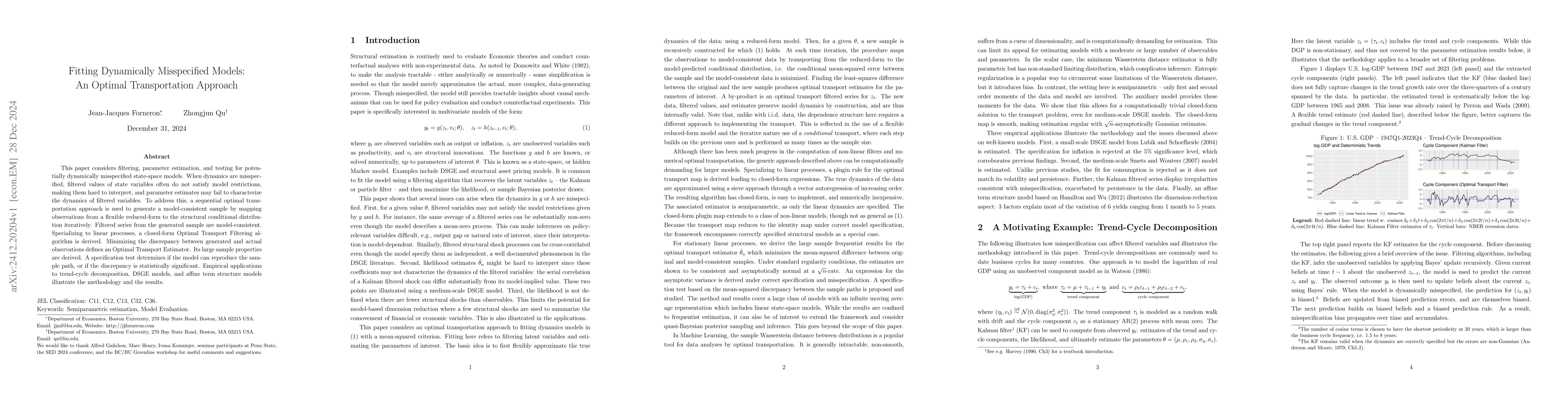

This paper considers filtering, parameter estimation, and testing for potentially dynamically misspecified state-space models. When dynamics are misspecified, filtered values of state variables often ...