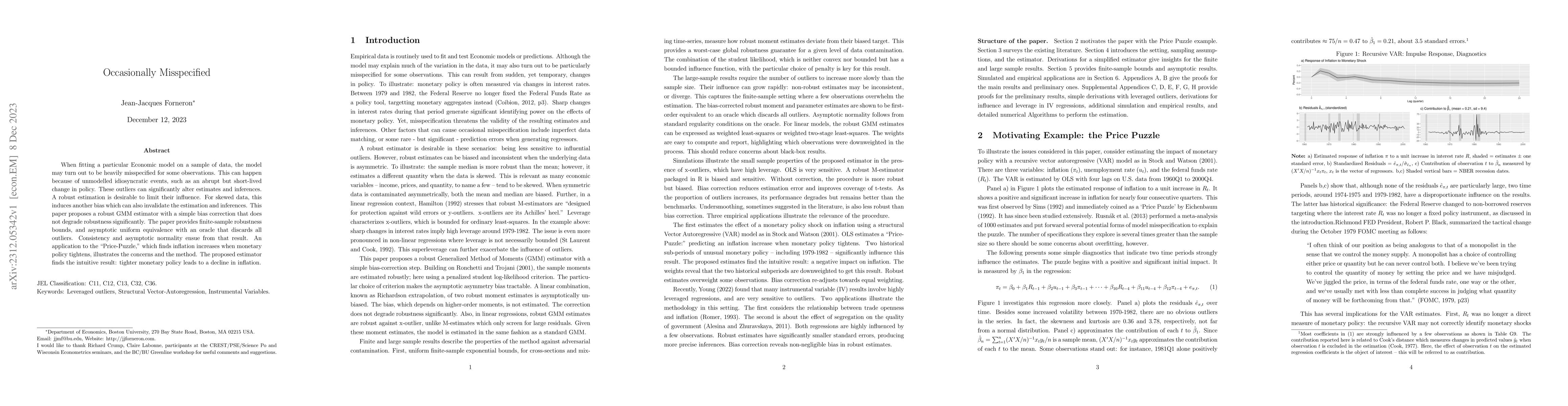

When fitting a particular Economic model on a sample of data, the model may

turn out to be heavily misspecified for some observations. This can happen

because of unmodelled idiosyncratic events, such as an abrupt but short-lived

change in policy. These outliers can significantly alter estimates and

inferences. A robust estimation is desirable to limit their influence. For

skewed data, this induces another bias which can also invalidate the estimation

and inferences. This paper proposes a robust GMM estimator with a simple bias

correction that does not degrade robustness significantly. The paper provides

finite-sample robustness bounds, and asymptotic uniform equivalence with an

oracle that discards all outliers. Consistency and asymptotic normality ensue

from that result. An application to the "Price-Puzzle," which finds inflation

increases when monetary policy tightens, illustrates the concerns and the

method. The proposed estimator finds the intuitive result: tighter monetary

policy leads to a decline in inflation.

Discussion 0