Academic Profile

Statistics

Similar Authors

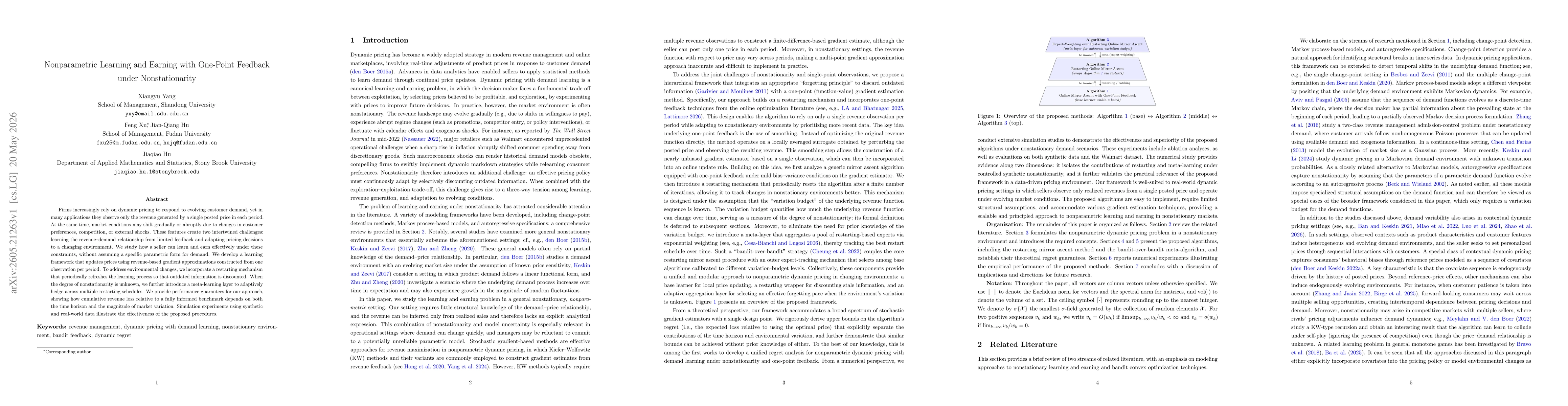

Papers on arXiv

We introduce ajdmom, a Python package designed for automatically deriving moment formulas for the well-established affine jump diffusion (AJD) processes. ajdmom can produce explicit closed-form expres...

We develop moment estimators for the parameters of affine stochastic volatility models. We first address the challenge of calculating moments for the models by introducing a recursive equation for der...

Black-box optimization is often encountered for decision-making in complex systems management, where the knowledge of system is limited. Under these circumstances, it is essential to balance the utili...

We develop a recursive approach for deriving closed-form solutions to both conditional and unconditional moments of affine jump diffusions with state-independent jump intensities. Using these moment s...

We present a kernel-based stochastic approximation (KBSA) framework for solving contextual stochastic optimization problems with differentiable objective functions. The framework only relies on system...

Conditional value-at-risk (CVaR) is a prominent risk measure in financial engineering, energy systems, and supply chain management. In these domains, Markov decision processes (MDPs) with a long-run C...

Firms increasingly rely on dynamic pricing to respond to evolving customer demand, yet in many applications they observe only the revenue generated by a single posted price in each period. At the same...

Data acquisition efficiency is a central challenge in deploying reinforcement learning in business and healthcare operations, where interactions are costly, slow, and often involve humans in the loop....