Academic Profile

Statistics

Similar Authors

Papers on arXiv

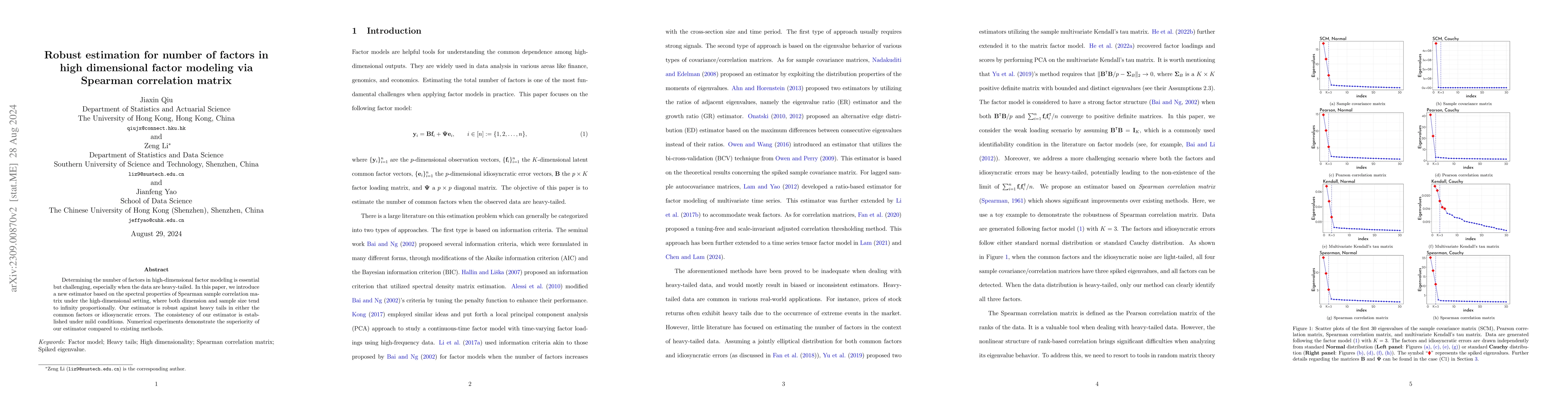

Determining the number of factors in high-dimensional factor modeling is essential but challenging, especially when the data are heavy-tailed. In this paper, we introduce a new estimator based on th...

This paper develops a new specification test for the instrument weakness when the number of instruments $K_n$ is large with a magnitude comparable to the sample size $n$. The test relies on the fact...

This paper revisits the Lagrange multiplier type test for the null hypothesis of no cross-sectional dependence in large panel data models. We propose a unified test procedure and its power enhanceme...

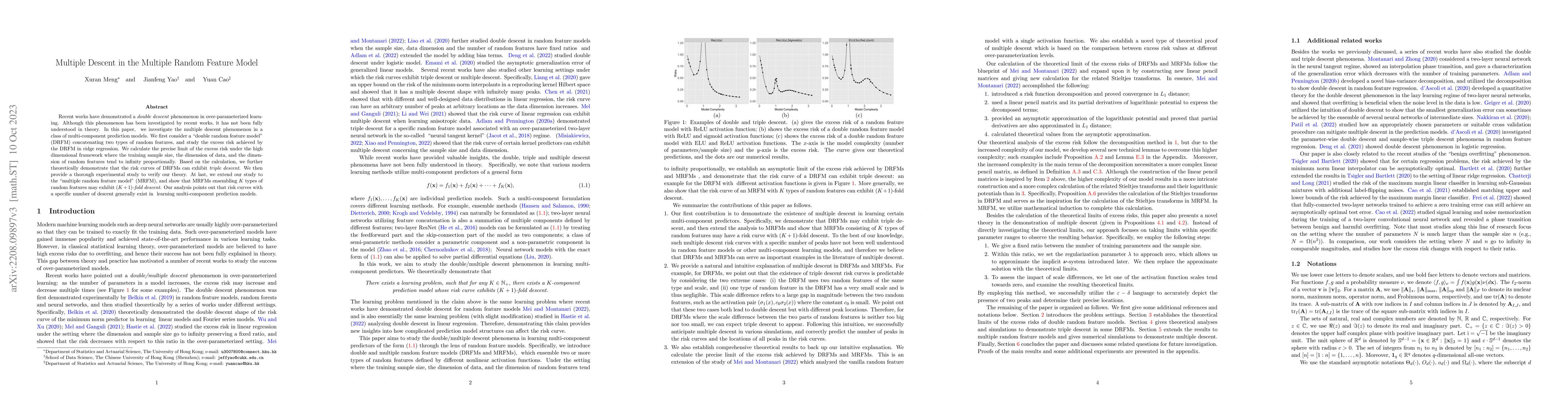

Recent works have demonstrated a double descent phenomenon in over-parameterized learning. Although this phenomenon has been investigated by recent works, it has not been fully understood in theory....

We study the eigenvalue distributions for sums of independent rank-one $k$-fold tensor products of large $n$-dimensional vectors. Previous results in the literature assume that $k=o(n)$ and show tha...

Much research effort has been devoted to explaining the success of deep learning. Random Matrix Theory (RMT) provides an emerging way to this end: spectral analysis of large random matrices involved...

Motivated by the stochastic block model, we investigate a class of Wigner-type matrices with certain block structures, and establish a CLT for the corresponding linear spectral statistics via the la...

Since the introduction of Dyson's Brownian motion in early 1960's, there have been a lot of developments in the investigation of stochastic processes on the space of Hermitian matrices. Their proper...

The asymptotic normality for a large family of eigenvalue statistics of a general sample covariance matrix is derived under the ultra-high dimensional setting, that is, when the dimension to sample ...

In this paper, we analyse singular values of a large $p\times n$ data matrix $\mathbf{X}_n= (\mathbf{x}_{n1},\ldots,\mathbf{x}_{nn})$ where the column $\mathbf{x}_{nj}$'s are independent $p$-dimensi...

We reexamine the classical linear regression model when the model is subject to two types of uncertainty: (i) some of covariates are either missing or completely inaccessible, and (ii) the variance ...

We introduce a new random matrix model called distance covariance matrix in this paper, whose normalized trace is equivalent to the distance covariance. We first derive a deterministic limit for the...

Inference of population structure from genetic data plays an important role in population and medical genetics studies. With the advancement and decreasing cost of sequencing technology, the increas...

This paper reexamines the seminal Lagrange multiplier test for cross-section independence in a large panel model where both the number of cross-sectional units n and the number of time series observ...

In this article, we establish a limiting distribution for eigenvalues of a class of auto-covariance matrices. The same distribution has been found in the literature for a regularized version of thes...

We consider a data matrix $X:=C_N^{1/2}ZR_M^{1/2}$ from a multivariate stationary process with a separable covariance function, where $C_N$ is a $N\times N$ positive semi-definite matrix, $Z$ a $N\t...

Consider a $p$-dimensional population ${\mathbf x} \in\mathbb{R}^p$ with iid coordinates in the domain of attraction of a stable distribution with index $\alpha\in (0,2)$. Since the variance of ${\m...

We consider eigenvalues of generalized Wishart processes as well as particle systems, of which the empirical measures converge to deterministic measures as the dimension goes to infinity. In this pa...

This paper studies the joint limiting behavior of extreme eigenvalues and trace of large sample covariance matrix in a generalized spiked population model, where the asymptotic regime is such that t...

This paper investigates limiting properties of eigenvalues of multivariate sample spatial-sign covariance matrices when both the number of variables and the sample size grow to infinity. The underly...

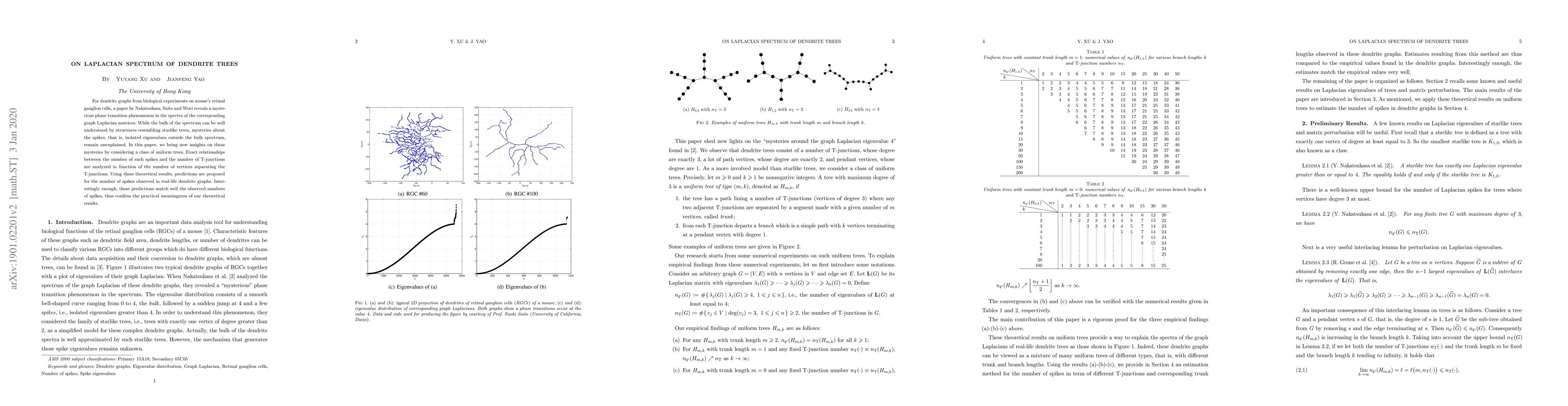

For dendrite graphs from biological experiments on mouse's retinal ganglion cells, a paper by Nakatsukasa, Saito and Woei reveals a mysterious phase transition phenomenon in the spectra of the corre...

Several well-established benchmark predictors exist for Value-at-Risk (VaR), a major instrument for financial risk management. Hybrid methods combining AR-GARCH filtering with skewed-$t$ residuals a...

Multimodal emotion recognition in conversation (MER) aims to accurately identify emotions in conversational utterances by integrating multimodal information. Previous methods usually treat multimodal ...

We consider two hypothesis testing problems for low-rank and high-dimensional tensor signals, namely the tensor signal alignment and tensor signal matching problems. These problems are challenging due...

This paper proposes procedures for testing the equality hypothesis and the proportionality hypothesis involving a large number of $q$ covariance matrices of dimension $p\times p$. Under a limiting sch...

P-hacking poses challenges to traditional hypothesis testing. In this paper, we propose a robust method for the one-sample significance test that can protect against p-hacking from sample manipulation...

Empirical studies reported that the Hessian matrix of neural networks (NNs) exhibits a near-block-diagonal structure, yet its theoretical foundation remains unclear. In this work, we reveal two forces...

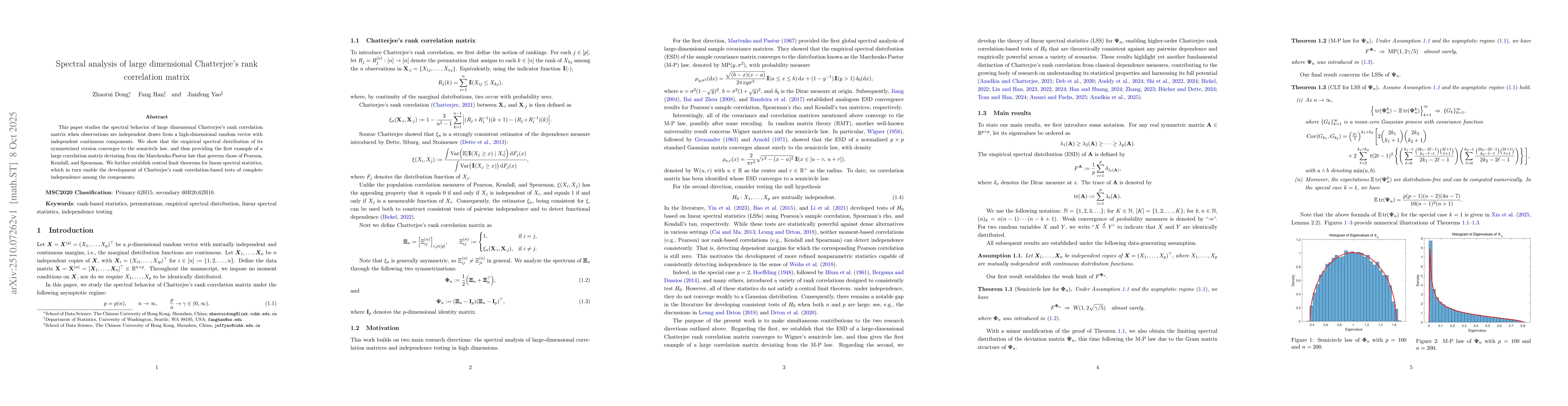

This paper studies the spectral behavior of large dimensional Chatterjee's rank correlation matrix when observations are independent draws from a high-dimensional random vector with independent contin...

In this paper, we consider procedures for testing hypotheses on the dimension of the linear span generated by a growing number of $p\times p$ covariance matrices from independent $q$ populations. Unde...

Let $\mathbf{x}$ be a random vector with $n$ i.i.d.\ real-valued components in the domain attraction of an $α$-stable law with $α\in(0,2)$, and let $\mathbf{y}=\mathbf{x}/\|\mathbf{x}\|_2$ be the asso...

This paper investigates testing for deviation of a high-dimensional mean vector $\boldsymbolμ$. In contrast to the standard one-sample significance test of the form: $H_0^\texttt{e} : \boldsymbolμ = \...

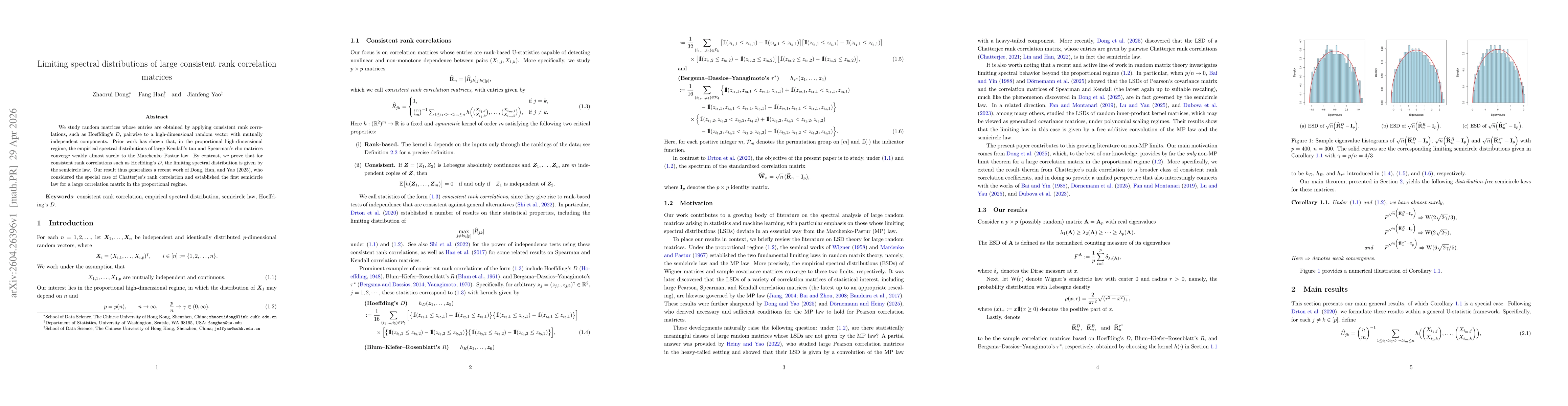

We study random matrices whose entries are obtained by applying consistent rank correlations, such as Hoeffding's $D$, pairwise to a high-dimensional random vector with mutually independent components...

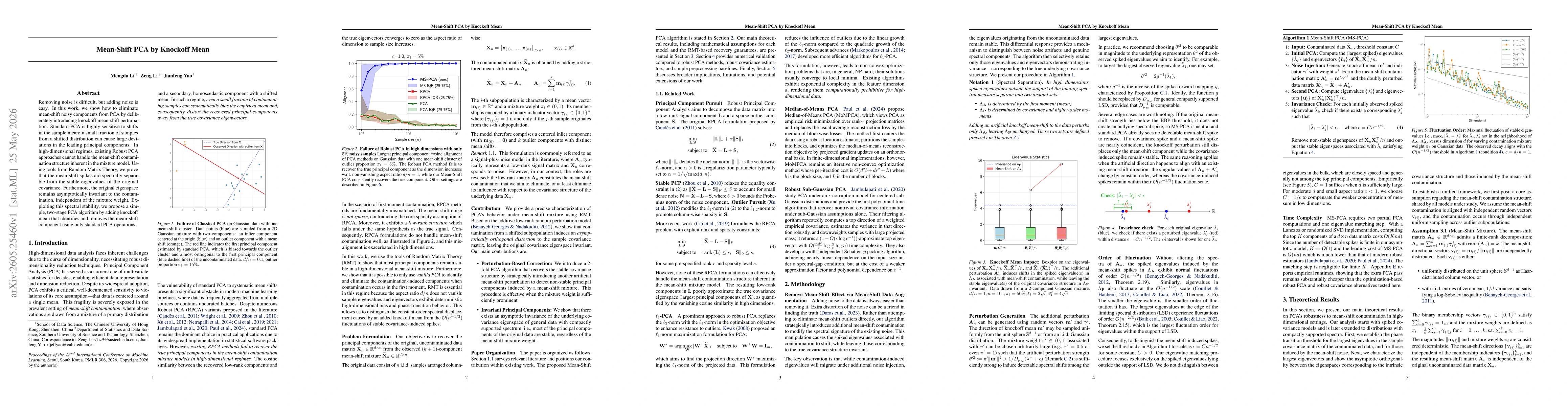

Removing noise is difficult, but adding noise is easy. In this work, we show how to eliminate mean-shift noisy components from PCA by deliberately introducing knockoff mean-shift perturbation. Standar...