Robust estimation for number of factors in high dimensional factor modeling via Spearman correlation matrix

Publication

Metrics

AI Quick Summary

This paper proposes a robust estimator for determining the number of factors in high-dimensional factor models using the spectral properties of the Spearman correlation matrix. The estimator is shown to be robust against heavy-tailed data and is demonstrated to outperform existing methods in numerical experiments.

Paper Preview

Abstract

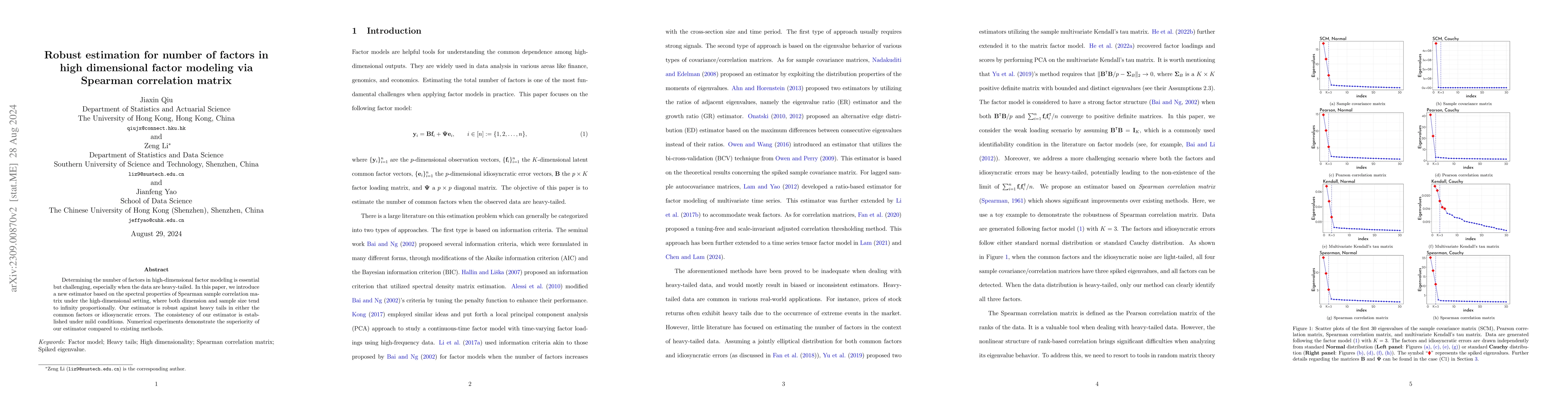

Determining the number of factors in high-dimensional factor modeling is essential but challenging, especially when the data are heavy-tailed. In this paper, we introduce a new estimator based on the spectral properties of Spearman sample correlation matrix under the high-dimensional setting, where both dimension and sample size tend to infinity proportionally. Our estimator is robust against heavy tails in either the common factors or idiosyncratic errors. The consistency of our estimator is established under mild conditions. Numerical experiments demonstrate the superiority of our estimator compared to existing methods.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0