Academic Profile

Statistics

Similar Authors

Papers on arXiv

In recent years, generative pre-trained paradigms such as Large Language Models (LLMs) and Large Vision Models (LVMs) have achieved revolutionary advancements and widespread real-world applications....

Deep learning (e.g., Transformer) has been widely and successfully used in multivariate time series forecasting (MTSF). Unlike existing methods that focus on training models from a single modal of t...

In this study, we introduce three distinct testing methods for testing alpha in high dimensional linear factor pricing model that deals with dependent data. The first method is a sum-type test proce...

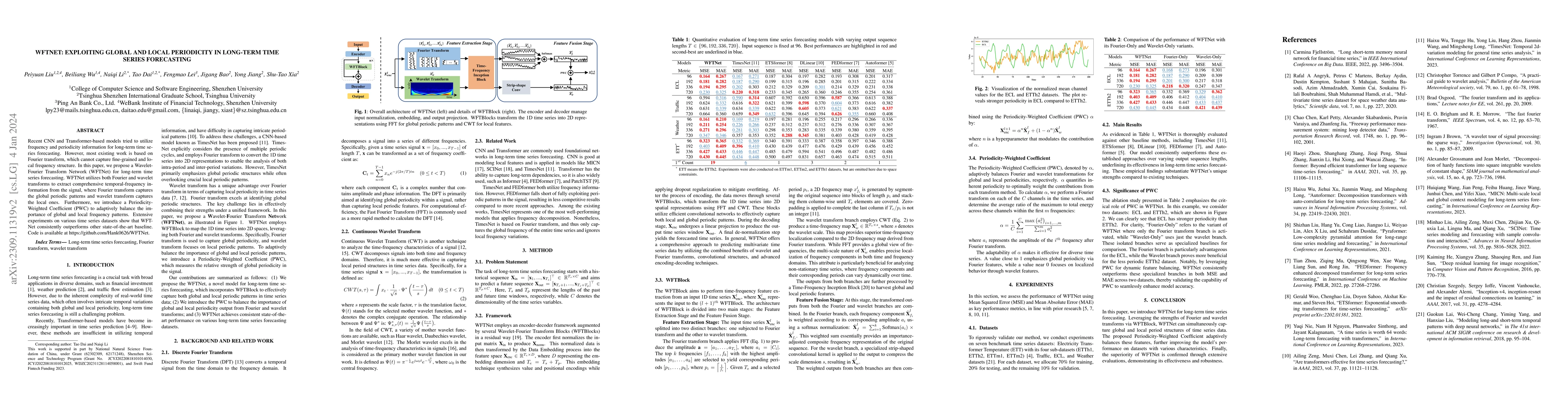

Recent CNN and Transformer-based models tried to utilize frequency and periodicity information for long-term time series forecasting. However, most existing work is based on Fourier transform, which...

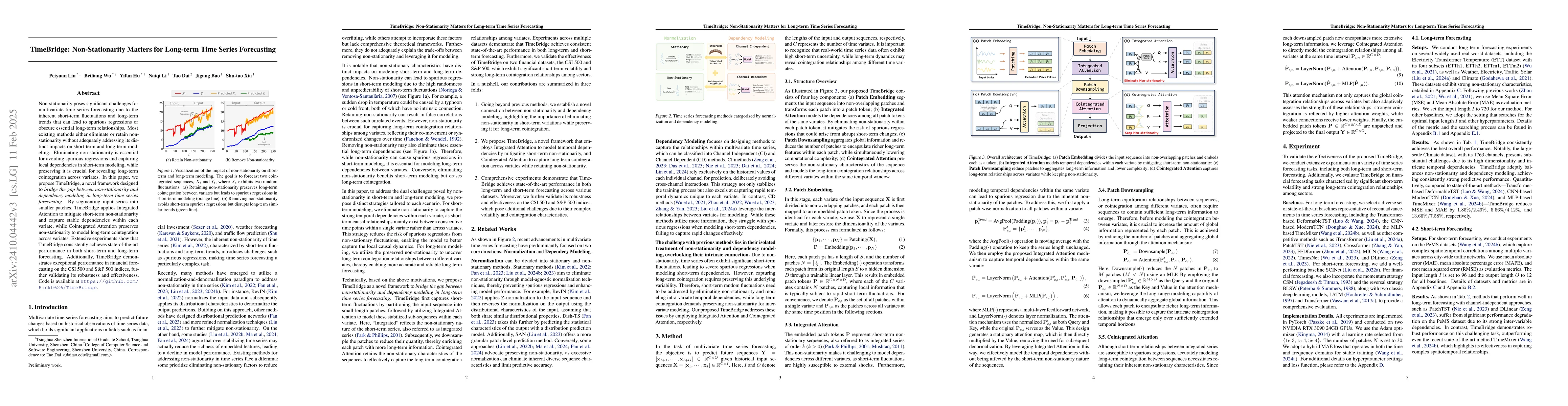

Non-stationarity poses significant challenges for multivariate time series forecasting due to the inherent short-term fluctuations and long-term trends that can lead to spurious regressions or obscure...

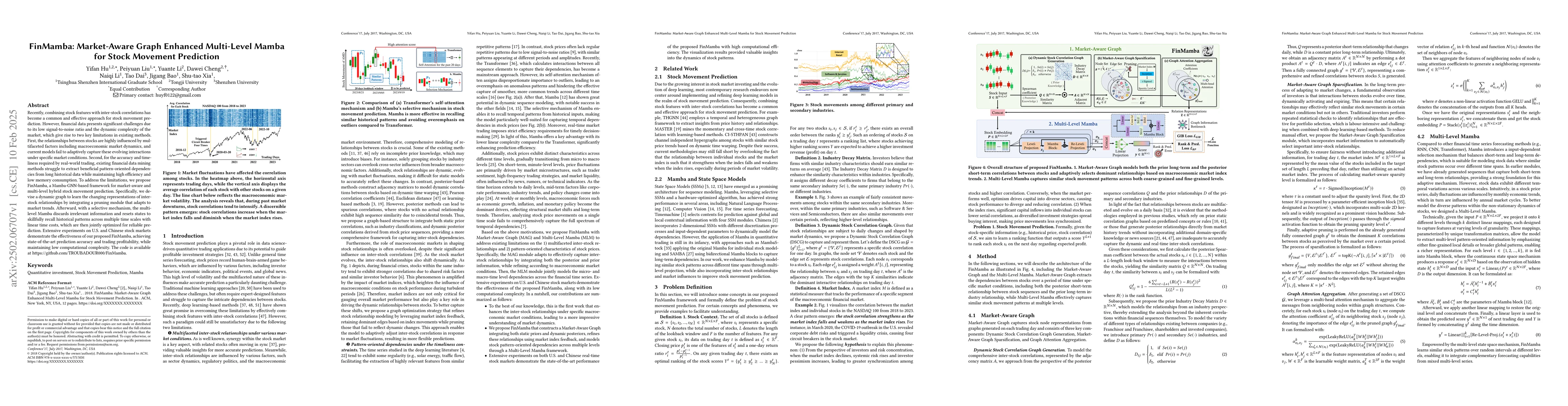

Recently, combining stock features with inter-stock correlations has become a common and effective approach for stock movement prediction. However, financial data presents significant challenges due t...