Academic Profile

Statistics

Papers on arXiv

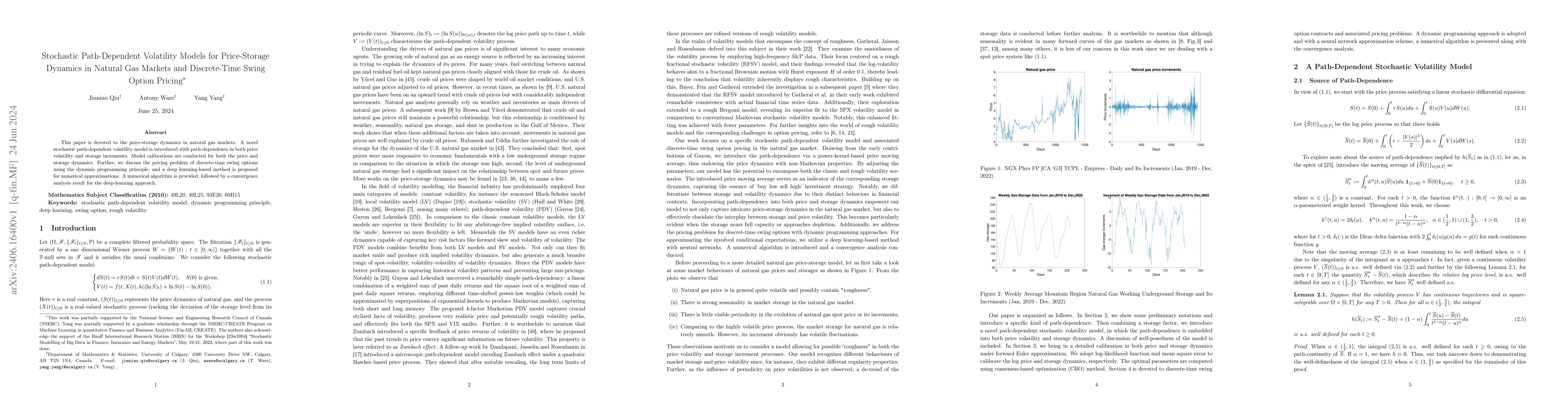

This paper is devoted to the price-storage dynamics in natural gas markets. A novel stochastic path-dependent volatility model is introduced with path-dependence in both price volatility and storage...

This paper is devoted to solving a class of second order Hamilton-Jacobi-Bellman (HJB) equations in the Wasserstein space, associated with mean field control problems involving common noise. We prov...

In this paper, we present a novel consensus-based zeroth-order algorithm tailored for non-convex multiplayer games. The proposed method leverages a metaheuristic approach using concepts from swarm i...

This paper is devoted to a viscosity solution theory of the stochastic Hamilton-Jacobi-Bellman equation in the Wasserstein spaces for the mean-field type control problem which allows for random coef...

This paper is devoted to the stochastic optimal control problem of infinite-dimensional differential systems allowing for both path-dependence and measurable randomness. As opposed to the determinis...

We investigate a general class of models for swarming/self-collective behaviour in domains with boundaries. The model is expressed as a stochastic system of interacting particles subject to both ref...

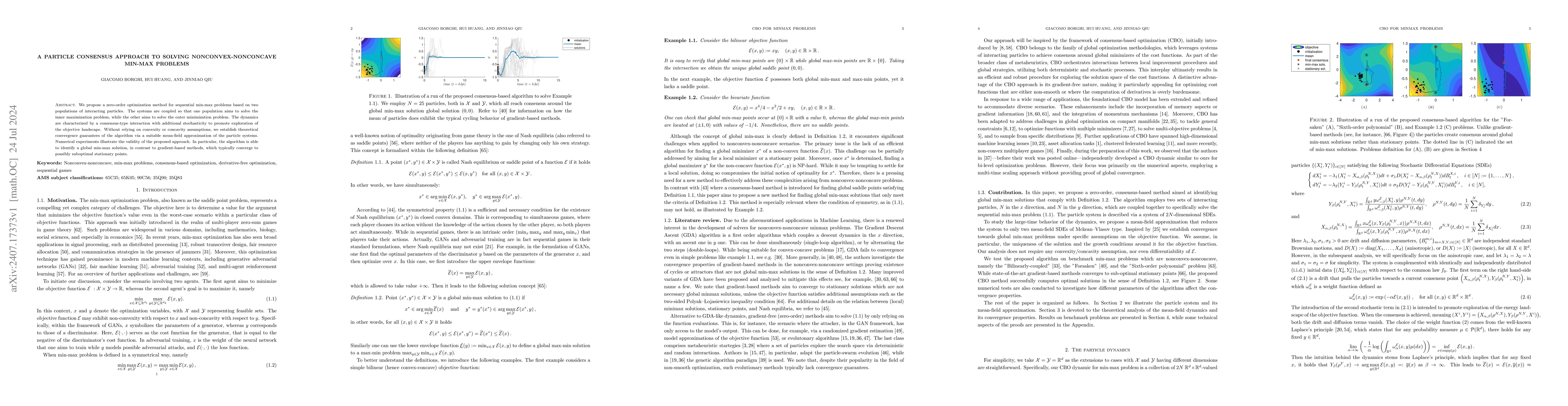

In this paper, we propose consensus-based optimization for saddle point problems (CBO-SP), a novel multi-particle metaheuristic derivative-free optimization method capable of provably finding global...

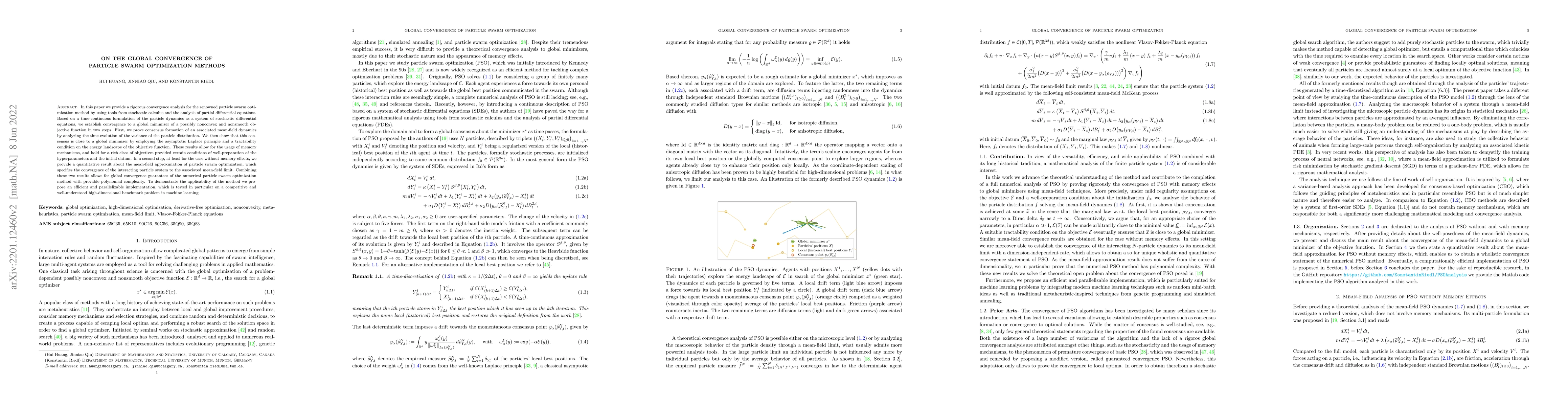

In this paper we provide a rigorous convergence analysis for the renowned particle swarm optimization method by using tools from stochastic calculus and the analysis of partial differential equation...

In this work we survey some recent results on the global minimization of a non-convex and possibly non-smooth high dimensional objective function by means of particle based gradient-free methods. Su...

This paper is concerned with the large particle limit for the consensus-based optimization (CBO), which was postulated in the pioneering works [6,28]. In order to solve this open problem, we adapt a...

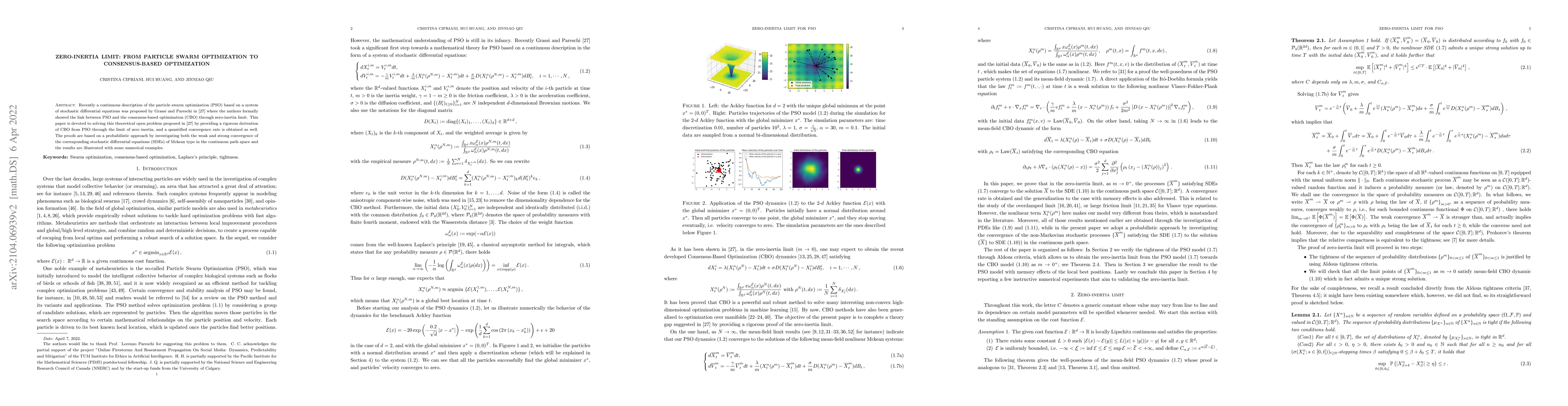

Recently a continuous description of the particle swarm optimization (PSO) based on a system of stochastic differential equations was proposed by Grassi and Pareschi in arXiv:2012.05613 where the au...

We propose and study a scheme combining the finite element method and machine learning techniques for the numerical approximations of coupled nonlinear forward-backward stochastic partial differenti...

In this paper, we study the option pricing problems for rough volatility models. As the framework is non-Markovian, the value function for a European option is not deterministic; rather, it is rando...

In this paper, we propose and study the stochastic path-dependent Hamilton-Jacobi-Bellman (SPHJB) equation that arises naturally from the optimal stochastic control problem of stochastic differentia...

This paper is devoted to a Feynman-Kac formula for general nonlinear time-dependent Schr\"odinger equations with applications in numerical approximations. Our formulation integrates both the Fisk-Stra...

We propose a zero-order optimization method for sequential min-max problems based on two populations of interacting particles. The systems are coupled so that one population aims to solve the inner ma...

In this paper, we show that the value functions of mean field control problems with common noise are the unique viscosity solutions to fully second-order Hamilton-Jacobi-Bellman equations, in a Cranda...

In this work, we extend deep learning-based numerical methods to fully coupled forward-backward stochastic differential equations (FBSDEs) within a non-Markovian framework. Error estimates and converg...

In this work, we investigate a stochastic control framework for global optimization over both finite-dimensional Euclidean spaces and the Wasserstein space of probability measures. In the Euclidean se...