Academic Profile

Statistics

Similar Authors

Papers on arXiv

The paper investigates the long-time behavior of zero-sum linear-quadratic stochastic differential games, aiming to demonstrate that, under appropriate conditions, both the saddle strategy and the o...

Motivated by linear-quadratic optimal control problems (LQ problems, for short) for mean-field stochastic differential equations (SDEs, for short) with the coefficients containing regime switching g...

We investigate a linear quadratic stochastic zero-sum game where two players lobby a political representative to invest in a wind turbine farm. Players are time-inconsistent because they discount pe...

In this paper, a systematic investigation is carried out for the general solvability of multi-dimensional backward stochastic Volterra integral equations (BSVIEs) with the generators being super-lin...

This paper is concerned with an optimal control problem for a mean-field linear stochastic differential equation with a quadratic functional in the infinite time horizon. Under suitable conditions, ...

This paper is concerned with an optimal control problem for a forward-backward stochastic differential equation (FBSDE, for short) with a recursive cost functional determined by a backward stochasti...

In this work, we introduce a stochastic maximum principle (SMP) approach for solving the reinforcement learning problem with the assumption that the unknowns in the environment can be parameterized ...

For a backward stochastic differential equation (BSDE, for short), when the generator is not progressively measurable, it might not admit adapted solutions, shown by an example. However, for backwar...

Spike variation technique plays a crucial role in deriving Pontryagin's type maximum principle of optimal controls for differential equations of several types, including ordinary differential equati...

A linear-quadratic optimal control problem for a forward stochastic Volterra integral equation (FSVIE, for short) is considered. Under the usual convexity conditions, open-loop optimal control exist...

This paper analyzes the limiting behavior of stochastic linear-quadratic optimal control problems in finite time horizon $[0,T]$ as $T\rightarrow\infty$. The so-called turnpike properties are establ...

This paper is concerned with a linear quadratic optimal control for a class of singular Volterra integral equations. Under proper convexity conditions, optimal control uniquely exists, and it could ...

For Hamilton-Jacobi-Bellman (HJB) equations, with the standard definitions of viscosity super-solution and sub-solution, it is known that there is a comparison between any (viscosity) super-solution...

A linear control system with quadratic cost functional over infinite time horizon is considered without assuming controllability/stabilizability condition and the global integrability condition for ...

The goal of this paper is to solve a class of stochastic optimal control problems numerically, in which the state process is governed by an It\^o type stochastic differential equation with control p...

An optimal ergodic control problem (EC problem, for short) is investigated for a linear stochastic differential equation with quadratic cost functional. Constant nonhomogeneous terms, not all zero, ...

This paper examines mean field linear-quadratic-Gaussian (LQG) social optimum control with volatility-uncertain common noise. The diffusion terms in the dynamics of agents contain an unknown volatil...

An optimal control problem is considered for a stochastic differential equation with the cost functional determined by a backward stochastic Volterra integral equation (BSVIE, for short). This kind ...

Maximization and minimization problems of the principle eigenvalue for divergence form second order elliptic operators with the Dirichlet boundary condition are considered. The principal eigen map o...

Motivated by the optimality system associated with controlled (forward) Volterra integral equations (FVIEs, for short), the well-posedness of coupled forward-backward Voterra integral equations (FBVIE...

This paper investigates the asymptotic behavior of the solution to a linear-quadratic stochastic optimal control problems. The so-called probability cell problem is introduced the first time. It serve...

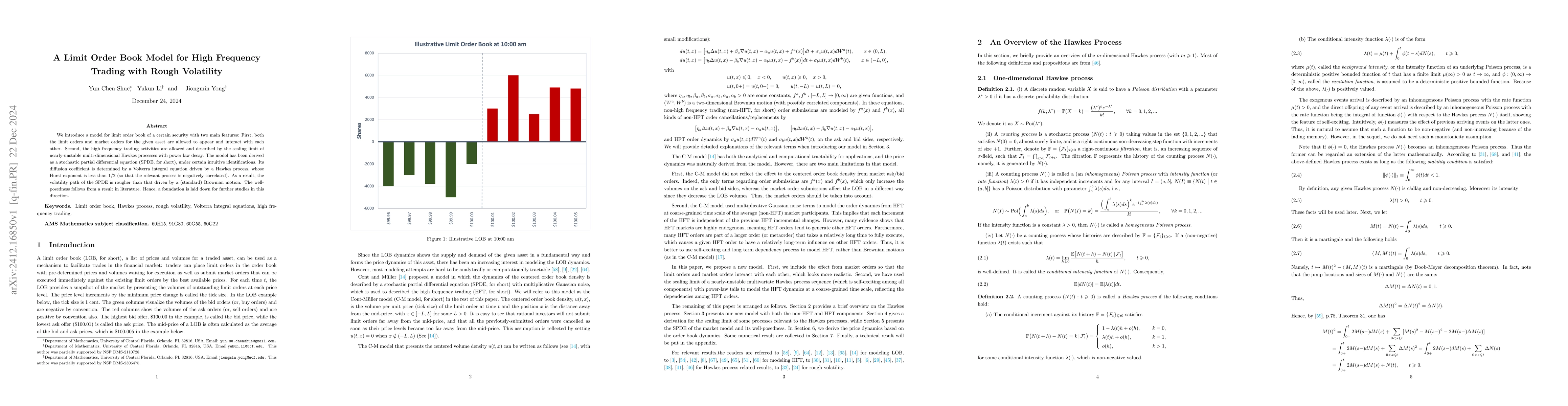

We introduce a model for limit order book of a certain security with two main features: First, both the limit orders and market orders for the given asset are allowed to appear and interact with each ...

This paper is concerned with stochastic linear quadratic (LQ, for short) optimal control problems in an infinite horizon with conditional mean-field term in a switching regime environment. The orthogo...

This paper is concerned with an infinite horizon stochastic linear quadratic (LQ, for short) optimal control problems with conditional mean-field terms in a switching environment. Different from [17],...

This paper is concerned with optimal control problems for a linear homogeneous stochastic differential equation having regime switching with purely quadratic functional in the large time horizons. We ...

This paper investigates a mean-field linear-quadratic optimal control problem where the state dynamics and cost functional incorporate both expectation and conditional expectation terms. We explicitly...

This paper is concerned with an optimal control problem for a nonhomogeneous linear stochastic differential equation having regime switching with a quadratic functional in the large time horizon. This...

This paper is concerned with a time-inconsistent stochastic optimal control problem in an infinite time horizon with a non-degenerate diffusion in the state equation. A major assumption is that people...

This paper is concerned with stochastic impulse control problems in which the running cost changes depending on the impulse control. Because of such a dependence, it brings several difficulties when t...

This paper is concerned with a stochastic linear quadratic (LQ, for short) control problem with a recursive cost functional. It involves BSDEs in $L^1$ whose well-posedness is a subtle issue. A suitab...

This paper is concerned with a stochastic linear quadratic (LQ, for short) control problem with a recursive cost functional in an infinite horizon. A main difficult is well-posedness of the BSDE in $L...