Academic Profile

Statistics

Similar Authors

Papers on arXiv

Diffusion models (DMs) are a type of generative model that has a huge impact on image synthesis and beyond. They achieve state-of-the-art generation results in various generative tasks. A great dive...

In this work, we present a novel machine learning approach for pricing high-dimensional American options based on the modified Gaussian process regression (GPR). We incorporate deep kernel learning ...

Constructing the Implied Volatility Surface (IVS) is a challenging task in quantitative finance due to the complexity of real markets and the sparsity of market data. Structural models like Stochastic...

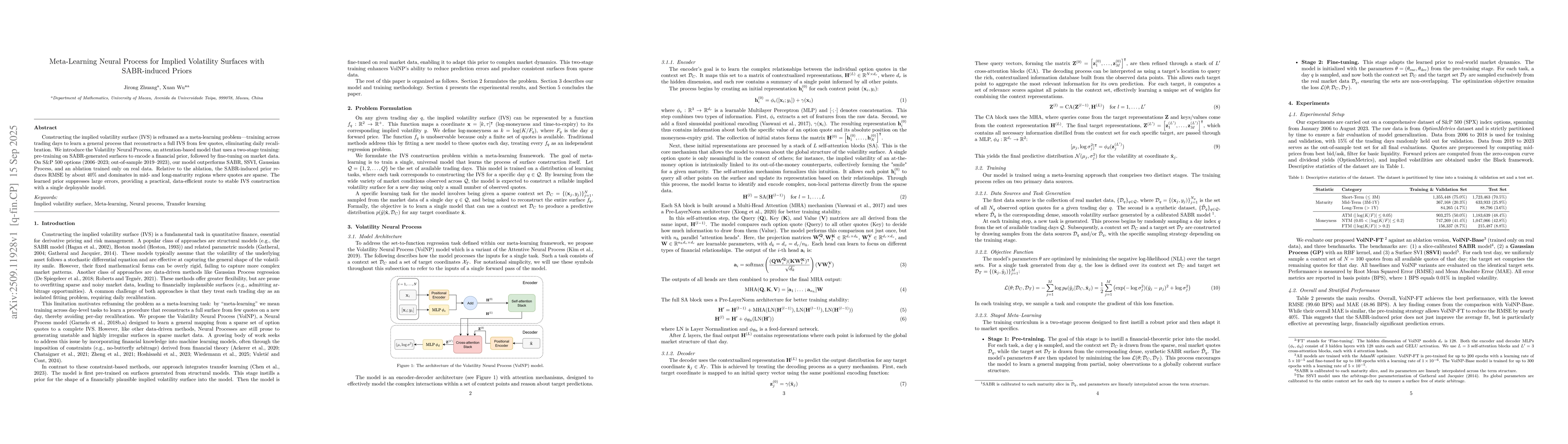

Constructing the implied volatility surface (IVS) is reframed as a meta-learning problem training across trading days to learn a general process that reconstructs a full IVS from few quotes, eliminati...