Academic Profile

Statistics

Similar Authors

Papers on arXiv

Within the nonparametric diffusion model, we develop a multiple test to infer about similarity of an unknown drift $b$ to some reference drift $b_0$: At prescribed significance, we simultaneously id...

For some discretely observed path of oscillating Brownian motion with level of self-organized criticality $\rho_0$, we prove in the infill asymptotics that the MLE is $n$-consistent, where $n$ denotes...

Based on discrete observations $X_0,X_Δ,\dots, X_{nΔ}$ for $Δ=n^{-γ}$ with $γ\in [0,1)$ of the null-recurrent dynamic $dX_t = σ(X_t)dW_t$ with a Brownian motion $W$ and $σ(x)=α\mathbb{1}\{x<ρ\} + β\ma...

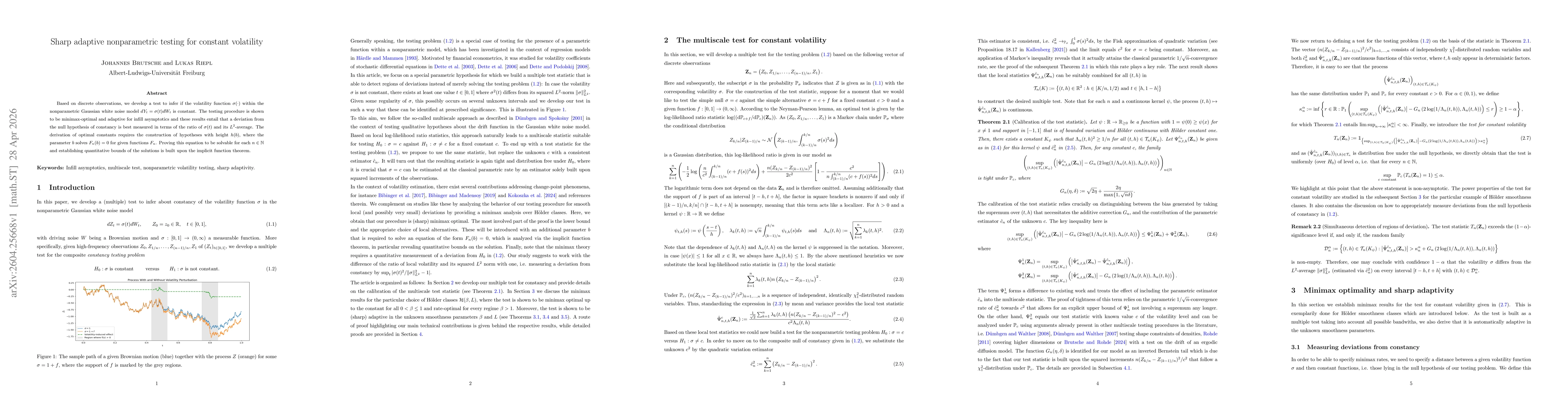

Based on discrete observations, we develop a test to infer if the volatility function $σ(\cdot)$ within the nonparametric Gaussian white noise model $dY_t = σ(t)dW_t$ is constant. The testing procedur...