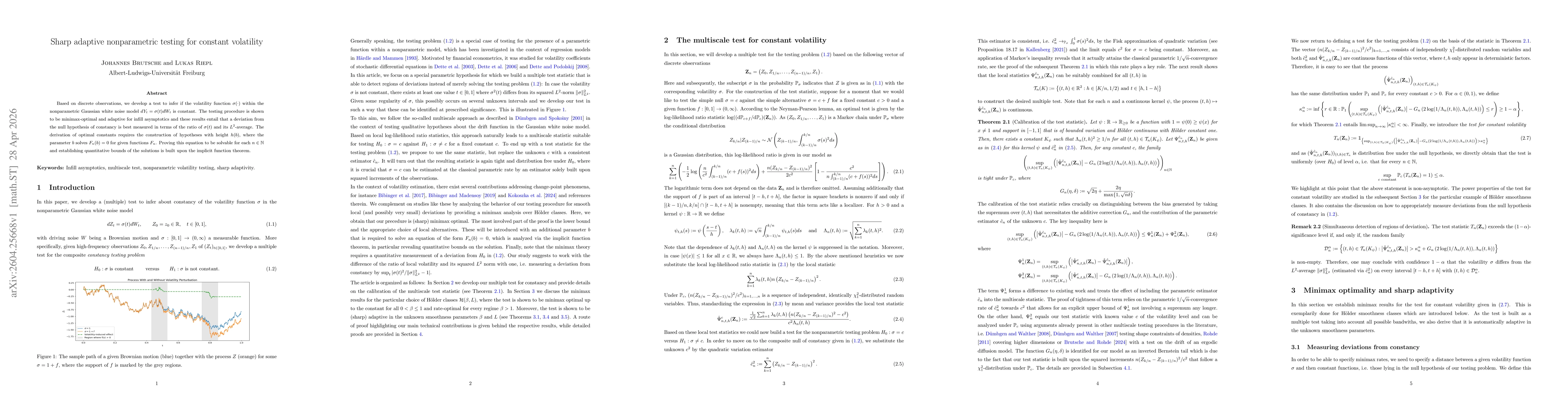

Sharp adaptive nonparametric testing for constant volatility

Publication

Metrics

AI Quick Summary

The paper develops a minimax-optimal, adaptive test to decide whether the volatility σ(t) in a continuous-time Gaussian white-noise model is constant, based on discrete observations. It shows that deviations from constancy are best measured by the ratio of σ(t) to its L2 average, and its proofs rely on constructing altitude-based hypotheses using the implicit function theorem to solve for key constants.

Paper Preview

Abstract

Based on discrete observations, we develop a test to infer if the volatility function $σ(\cdot)$ within the nonparametric Gaussian white noise model $dY_t = σ(t)dW_t$ is constant. The testing procedure is shown to be minimax-optimal and adaptive for infill asymptotics and these results entail that a deviation from the null hypothesis of constancy is best measured in terms of the ratio of $σ(t)$ and its $L^2$-average. The derivation of optimal constants requires the construction of hypotheses with height $h(b)$, where the parameter $b$ solves $F_n(b)=0$ for given functions $F_n$. Proving this equation to be solvable for each $n\in\mathbb{N}$ and establishing quantitative bounds of the solutions is built upon the implicit function theorem.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Discussion 0