Academic Profile

Statistics

Similar Authors

Papers on arXiv

Minimizing execution costs for large orders is a fundamental challenge in finance. Firms often depend on brokers to manage their trades due to limited internal resources for optimizing trading strat...

Portfolio managers' orders trade off return and trading cost predictions. Return predictions rely on alpha models, whereas price impact models quantify trading costs. This paper studies what happens...

We study a multi-player stochastic differential game, where agents interact through their joint price impact on an asset that they trade to exploit a common trading signal. In this context, we prove...

We study one-shot Nash competition between an arbitrary number of identical dealers that compete for the order flow of a client. The client trades either because of proprietary information, exposure...

We study a risk-sharing economy where an arbitrary number of heterogenous agents trades an arbitrary number of risky assets subject to quadratic transaction costs. For linear state dynamics, the for...

This paper studies the equilibrium price of an asset that is traded in continuous time between N agents who have heterogeneous beliefs about the state process underlying the asset's payoff. We propo...

We study risk-sharing equilibria with general convex costs on the agents' trading rates. For an infinite-horizon model with linear state dynamics and exogenous volatilities, we prove that the equili...

We study risk-sharing economies where heterogenous agents trade subject to quadratic transaction costs. The corresponding equilibrium asset prices and trading strategies are characterised by a syste...

We study a continuous-time version of the intermediation model of Grossman and Miller (1988). To wit, we solve for the competitive equilibrium prices at which liquidity takers' demands are absorbed ...

Using elementary arguments, we show how to derive $\mathbf{L}_p$-error bounds for the approximation of frictionless wealth process in markets with proportional transaction costs. For utilities with ...

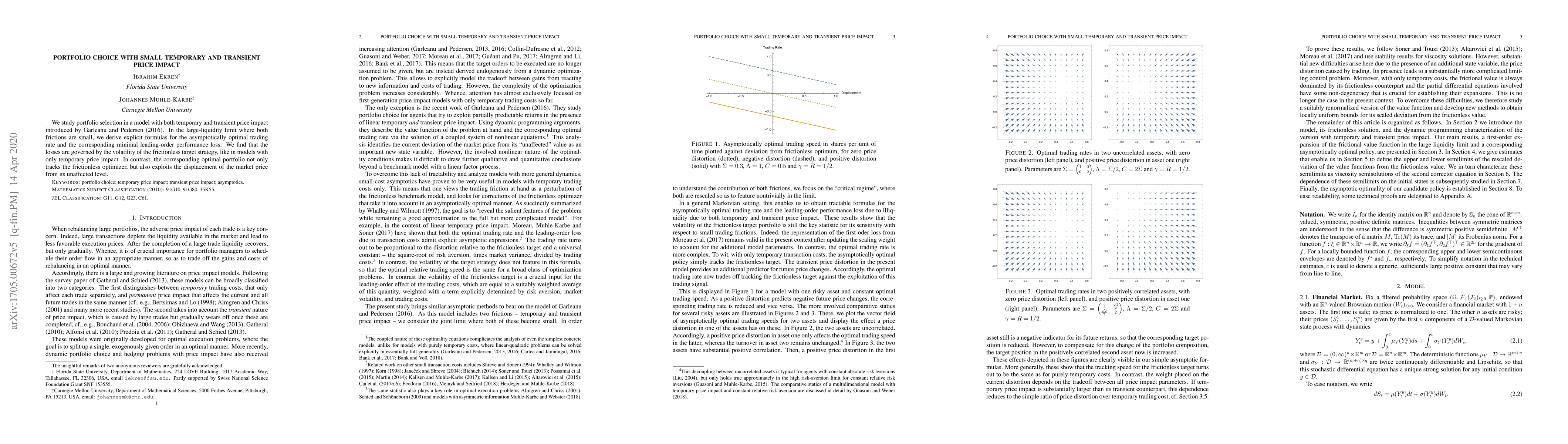

We study portfolio selection in a model with both temporary and transient price impact introduced by Garleanu and Pedersen (2016). In the large-liquidity limit where both frictions are small, we der...

Maglaras, Moallemi, and Zheng (2021) have introduced a flexible queueing model for fragmented limit-order markets, whose fluid limit remains remarkably tractable. In the present study we prove that, i...

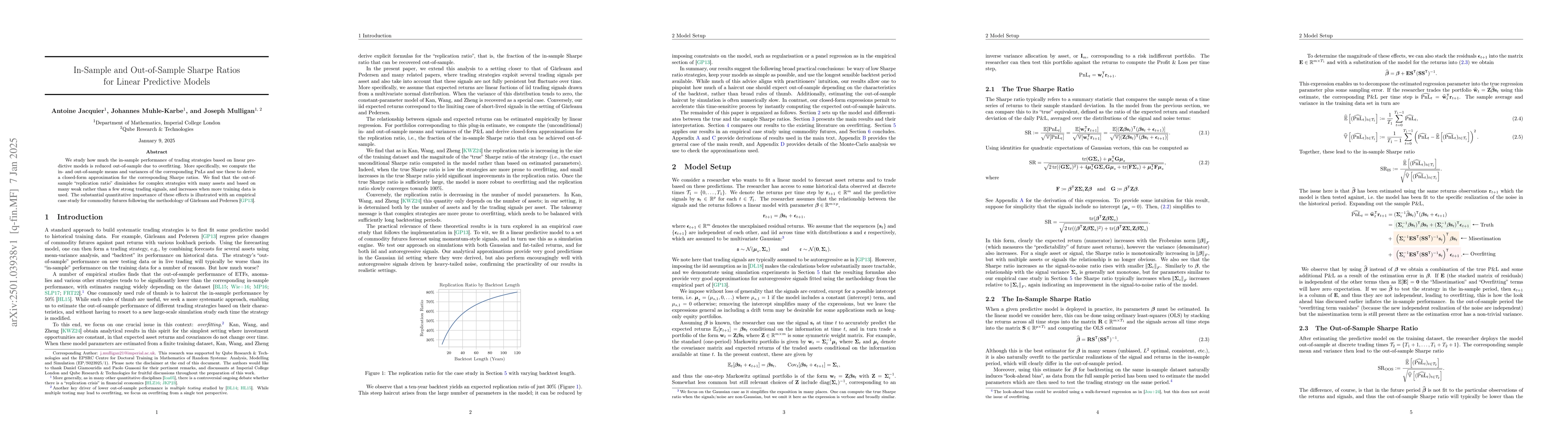

We study how much the in-sample performance of trading strategies based on linear predictive models is reduced out-of-sample due to overfitting. More specifically, we compute the in- and out-of-sample...

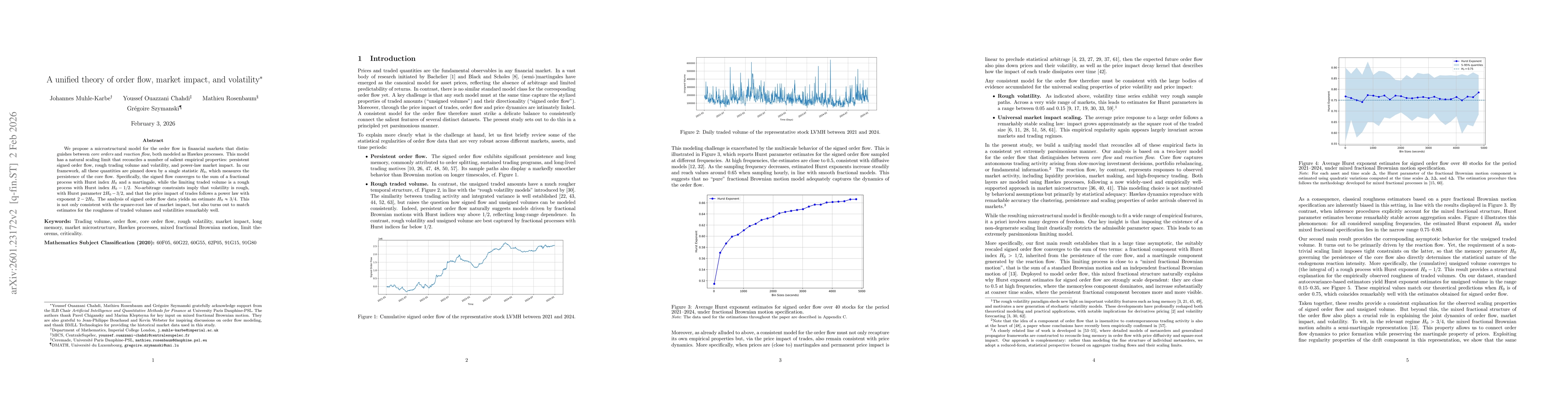

We propose a microstructural model for the order flow in financial markets that distinguishes between {\it core orders} and {\it reaction flow}, both modeled as Hawkes processes. This model has a natu...