Academic Profile

Statistics

Similar Authors

Papers on arXiv

We consider testing a composite null hypothesis $\mathcal{P}$ against a point alternative $\mathsf{Q}$ using e-variables, which are nonnegative random variables $X$ such that $\mathbb{E}_\mathsf{P}[...

In July 2023, Nasdaq announced a `Special Rebalance' of the Nasdaq-100 index to reduce the index weights of its large constituents. A rebalance as suggested currently by Nasdaq index methodology may...

Fund models are statistical descriptions of markets where all asset returns are spanned by the returns of a lower-dimensional collection of funds, modulo orthogonal noise. Equivalently, they may be ...

We provide a composite version of Ville's theorem that an event has zero measure if and only if there exists a nonnegative martingale which explodes to infinity when that event occurs. This is a cla...

Confidence sequences, anytime p-values (called p-processes in this paper), and e-processes all enable sequential inference for composite and nonparametric classes of distributions at arbitrary stopp...

The paper develops multiplicative compensation for complex-valued semimartingales and studies some of its consequences. It is shown that the stochastic exponential of any complex-valued semimartinga...

We develop a stochastic calculus that makes it easy to capture a variety of predictable transformations of semimartingales such as changes of variables, stochastic integrals, and their compositions....

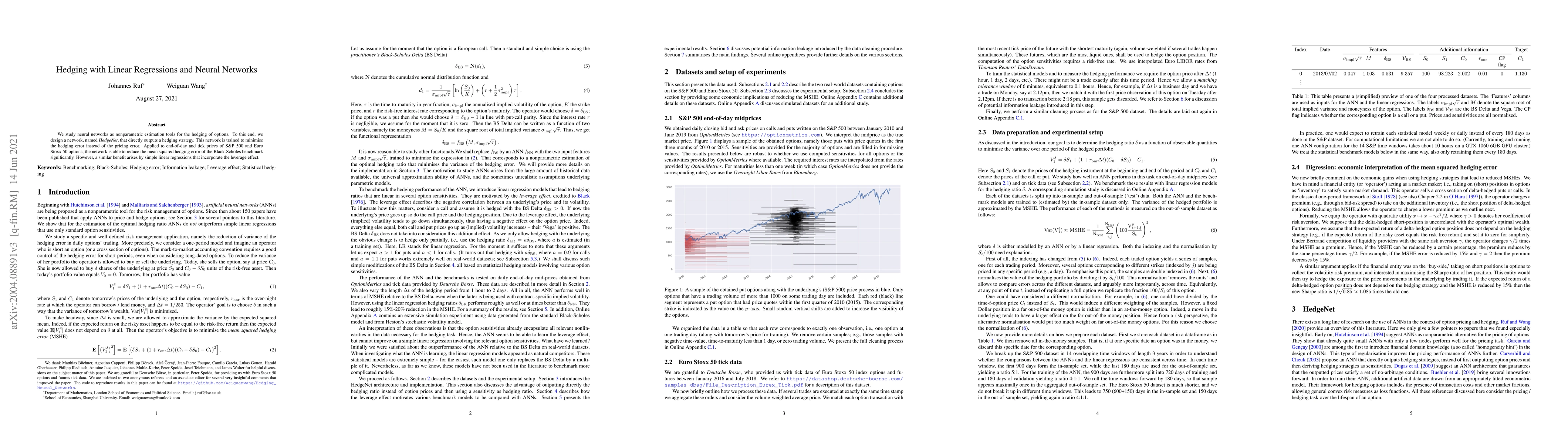

We study neural networks as nonparametric estimation tools for the hedging of options. To this end, we design a network, named HedgeNet, that directly outputs a hedging strategy. This network is tra...

We study the following question: What is the largest deterministic amount of time $T_*$ that a suitably normalized martingale $X$ can be kept inside a convex body $K$ in $\mathbb{R}^d$? We show, in ...

We characterize the minimal time horizon over which any equity market with $d \geq 2$ stocks and sufficient intrinsic volatility admits relative arbitrage with respect to the market portfolio. If $d...

We characterize the event of convergence of a local supermartingale. Conditions are given in terms of its predictable characteristics and quadratic variation. The notion of stationarily local integr...

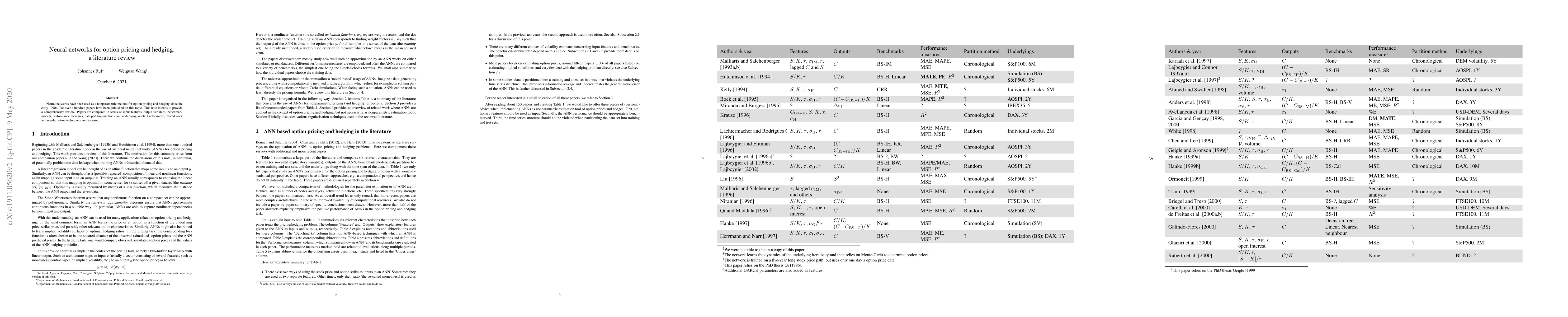

Neural networks have been used as a nonparametric method for option pricing and hedging since the early 1990s. Far over a hundred papers have been published on this topic. This note intends to provi...

A new integral with respect to an integer-valued random measure is introduced. In contrast to the finite variation integral ubiquitous in semimartingale theory (Jacod and Shiryaev, 2003, II.1.5), th...

We propose a method to determine the expectation of the supremum of the price process in stochastic volatility models. It can be applied to the rough Bergomi model, avoiding the need to discuss finite...

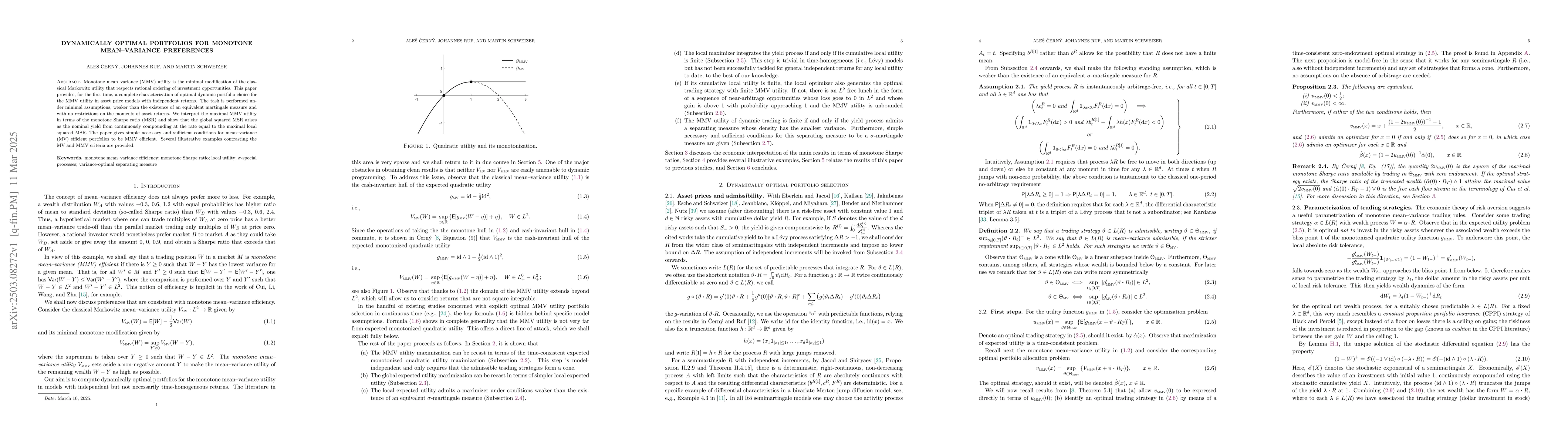

Monotone mean-variance (MMV) utility is the minimal modification of the classical Markowitz utility that respects rational ordering of investment opportunities. This paper provides, for the first time...

An e-variable for a family of distributions $\mathcal{P}$ is a nonnegative random variable whose expected value under every distribution in $\mathcal{P}$ is at most one. E-variables have recently been...

We derive concentration inequalities for sums of independent and identically distributed random variables that yield non-asymptotic generalizations of several strong laws of large numbers including so...

We revisit a fundamental question in hypothesis testing: given two sets of probability measures $\mathcal{P}$ and $\mathcal{Q}$, when does a nontrivial (i.e.\ strictly unbiased) test for $\mathcal{P}$...

This paper presents general strong duality results when testing hypotheses by betting against them. A bet is an e-variable for a composite null hypothesis $\mathcal{P}$: a nonnegative random variable ...

Uniformly weighted divergence preferences (UWDP) introduced in Maccheroni et al. (2006) are an important class of risk-averse preferences that contain as a special case the monotone mean--variance uti...