Academic Profile

Statistics

Similar Authors

Papers on arXiv

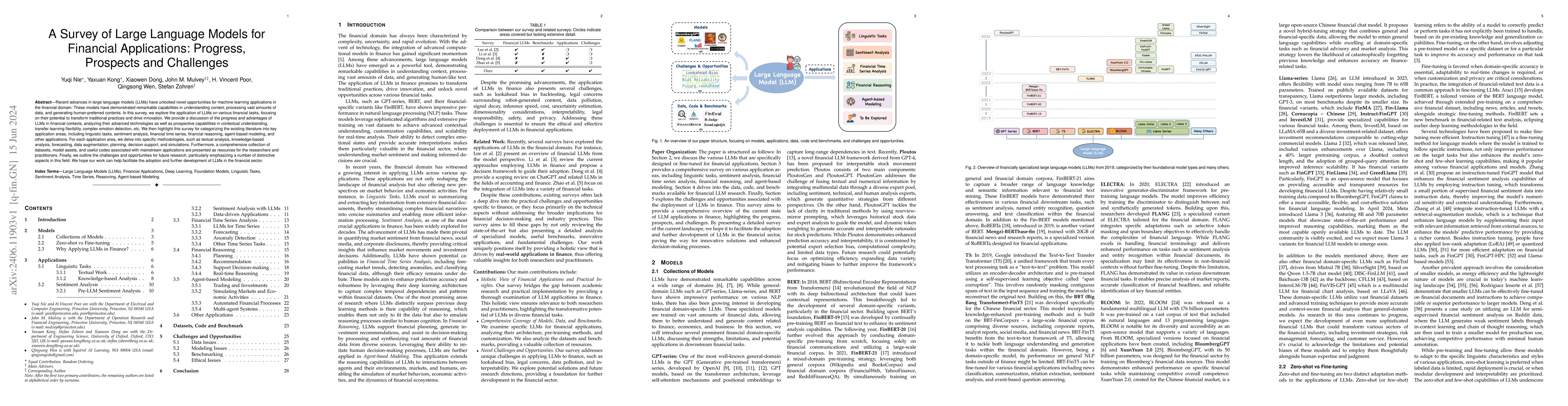

Recent advances in large language models (LLMs) have unlocked novel opportunities for machine learning applications in the financial domain. These models have demonstrated remarkable capabilities in...

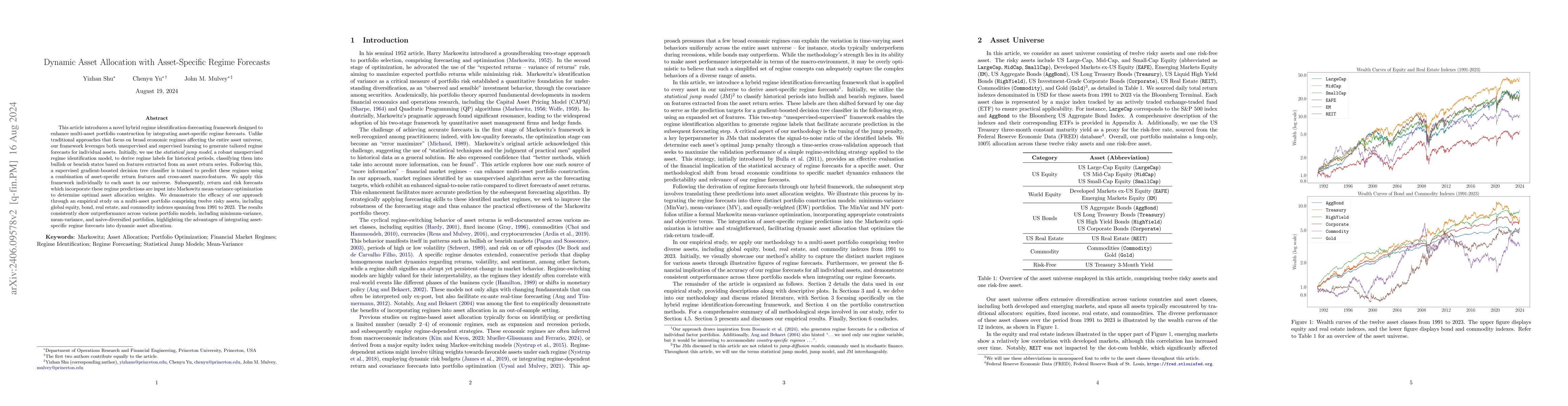

This article introduces a novel hybrid regime identification-forecasting framework designed to enhance multi-asset portfolio construction by integrating asset-specific regime forecasts. Unlike tradi...

Optimal execution of a portfolio have been a challenging problem for institutional investors. Traders face the trade-off between average trading price and uncertainty, and traditional methods suffer...

This paper introduces the MCTS algorithm to the financial world and focuses on solving significant multi-period financial planning models by combining a Monte Carlo Tree Search algorithm with a deep...

Portfolio optimization has been a central problem in finance, often approached with two steps: calibrating the parameters and then solving an optimization problem. Yet, the two-step procedure someti...

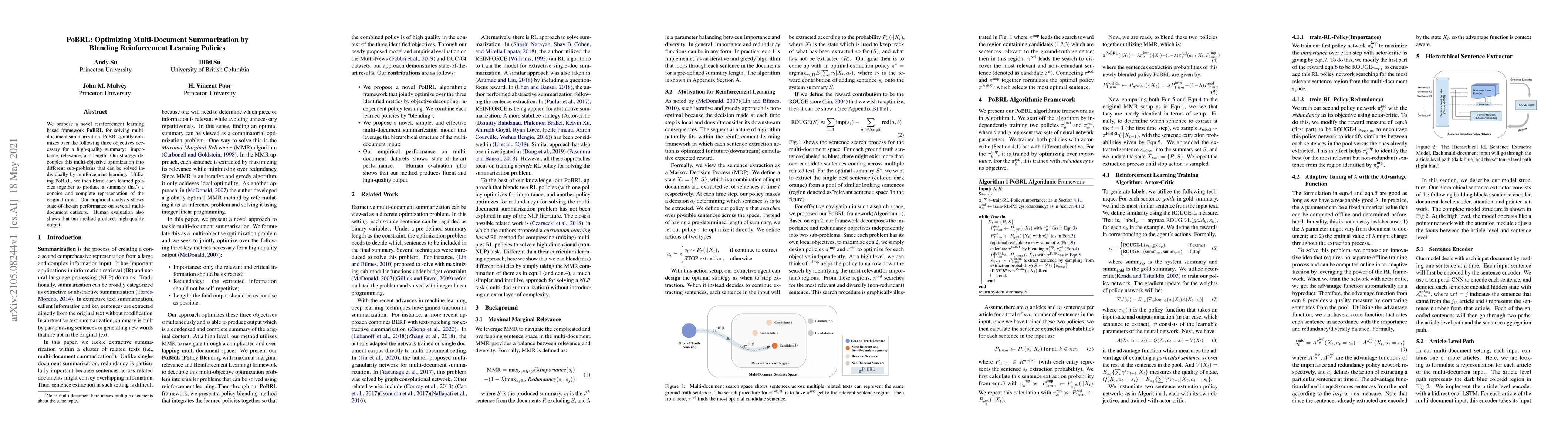

We propose a novel reinforcement learning based framework PoBRL for solving multi-document summarization. PoBRL jointly optimizes over the following three objectives necessary for a high-quality sum...

We employ model predictive control for a multi-period portfolio optimization problem. In addition to the mean-variance objective, we construct a portfolio whose allocation is given by model predicti...

This article explores dynamic factor allocation by analyzing the cyclical performance of factors through regime analysis. The authors focus on a U.S. equity investment universe comprising seven long-o...