Academic Profile

Statistics

Similar Authors

Papers on arXiv

The theory of convex risk functions has now been well established as the basis for identifying the families of risk functions that should be used in risk averse optimization problems. Despite its th...

We introduce a robust variant of the Kelly portfolio optimization model, called the Wasserstein-Kelly portfolio optimization. Our model, taking a Wasserstein distributionally robust optimization (DR...

Wasserstein distributionally robust optimization (DRO) has found success in operations research and machine learning applications as a powerful means to obtain solutions with favourable out-of-sampl...

Data-driven distributionally robust optimization is a recently emerging paradigm aimed at finding a solution that is driven by sample data but is protected against sampling errors. An increasingly p...

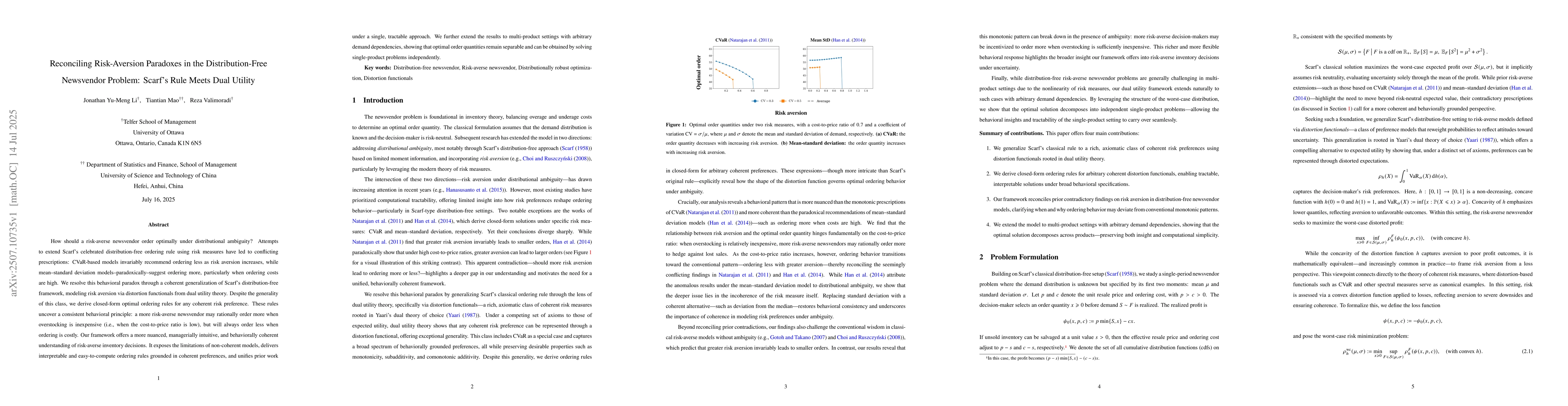

How should a risk-averse newsvendor order optimally under distributional ambiguity? Attempts to extend Scarf's celebrated distribution-free ordering rule using risk measures have led to conflicting pr...

Conditional risk minimization arises in high-stakes decisions where risk must be assessed in light of side information, such as stressed economic conditions, specific customer profiles, or other conte...

We propose Generative Adversarial Regression (GAR), a framework for learning conditional risk scenarios through generators aligned with downstream risk objectives. GAR builds on a regression character...

Sparsity or complexity? In modern high-dimensional asset pricing, these are often viewed as competing principles: richer feature spaces appear to favor complexity, while economic intuition has long fa...

Modern stochastic optimization pipelines increasingly rely on learned generative models to represent uncertainty, while downstream decisions are evaluated almost entirely through Monte Carlo scenarios...