Academic Profile

Statistics

Similar Authors

Papers on arXiv

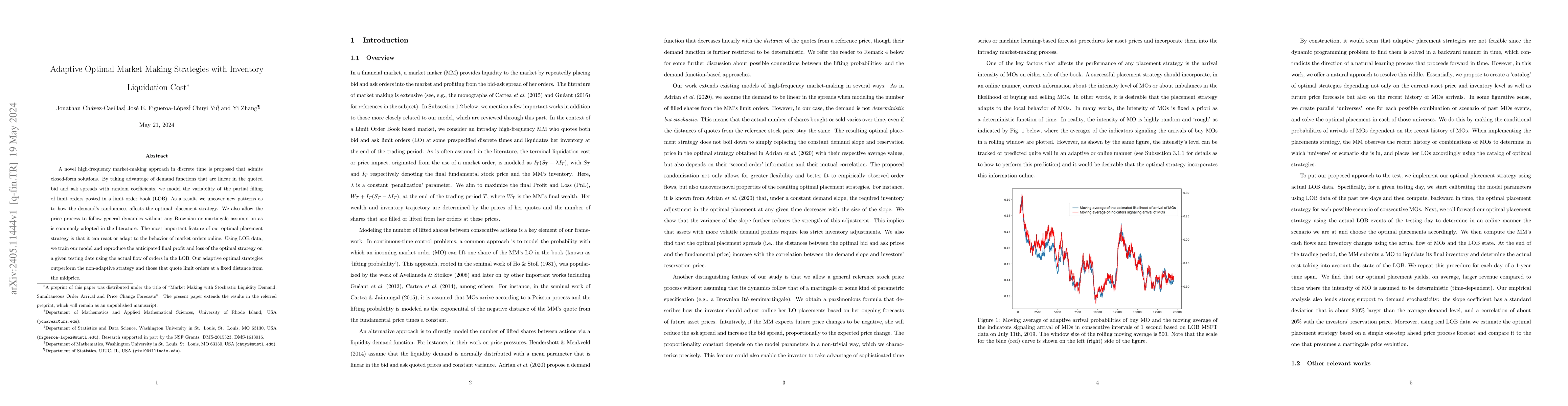

A novel high-frequency market-making approach in discrete time is proposed that admits closed-form solutions. By taking advantage of demand functions that are linear in the quoted bid and ask spread...

Many methods for estimating integrated volatility and related functionals of semimartingales in the presence of jumps require specification of tuning parameters for their use in practice. In much of...

Statistical inference for stochastic processes based on high-frequency observations has been an active research area for more than two decades. One of the most well-known and widely studied problems...

Statistical inference for stochastic processes based on high-frequency observations has been an active research area for more than a decade. One of the most well-known and widely studied problems is...

We provide an explicit characterization of the optimal market making strategy in a discrete-time Limit Order Book (LOB). In our model, the number of filled orders during each period depends linearly...

We first revisit the problem of estimating the spot volatility of an It\^o semimartingale using a kernel estimator. We prove a Central Limit Theorem with optimal convergence rate for a general two-s...

Volatility estimation based on high-frequency data is key to accurately measure and control the risk of financial assets. A L\'{e}vy process with infinite jump activity and microstructure noise is c...

For a multidimensional It\^o semimartingale, we consider the problem of estimating integrated volatility functionals. Jacod and Rosenbaum (2013) studied a plug-in type of estimator based on a Riemann ...

Volatility estimation is a central problem in financial econometrics, but becomes particularly challenging when jump activity is high, a phenomenon observed empirically in highly traded financial secu...

In the present paper, we study the near-maturity ($t\rightarrow T^{-}$) convergence rate of the optimal early-exercise price $b(t)$ of an American put under an exponential Lévy model with a {\it nonze...