Academic Profile

Statistics

Similar Authors

Papers on arXiv

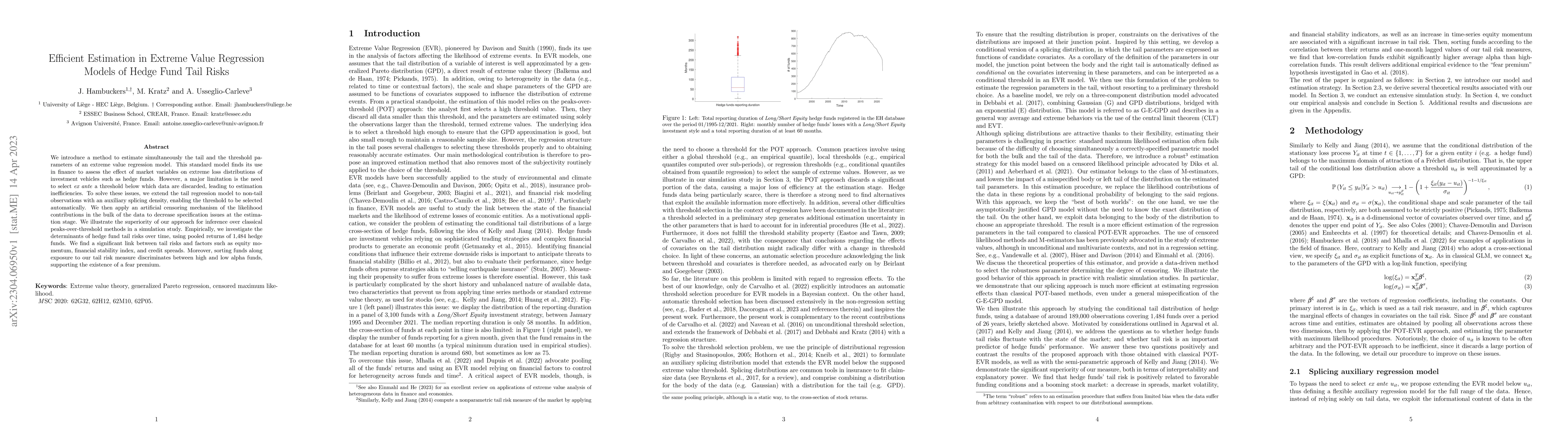

We introduce a method to estimate simultaneously the tail and the threshold parameters of an extreme value regression model. This standard model finds its use in finance to assess the effect of mark...

We study tail risk dynamics in high-frequency financial markets and their connection with trading activity and market uncertainty. We introduce a dynamic extreme value regression model accommodating...

Response functions linking regression predictors to properties of the response distribution are fundamental components in many statistical models. However, the choice of these functions is typically...