Academic Profile

Statistics

Similar Authors

Papers on arXiv

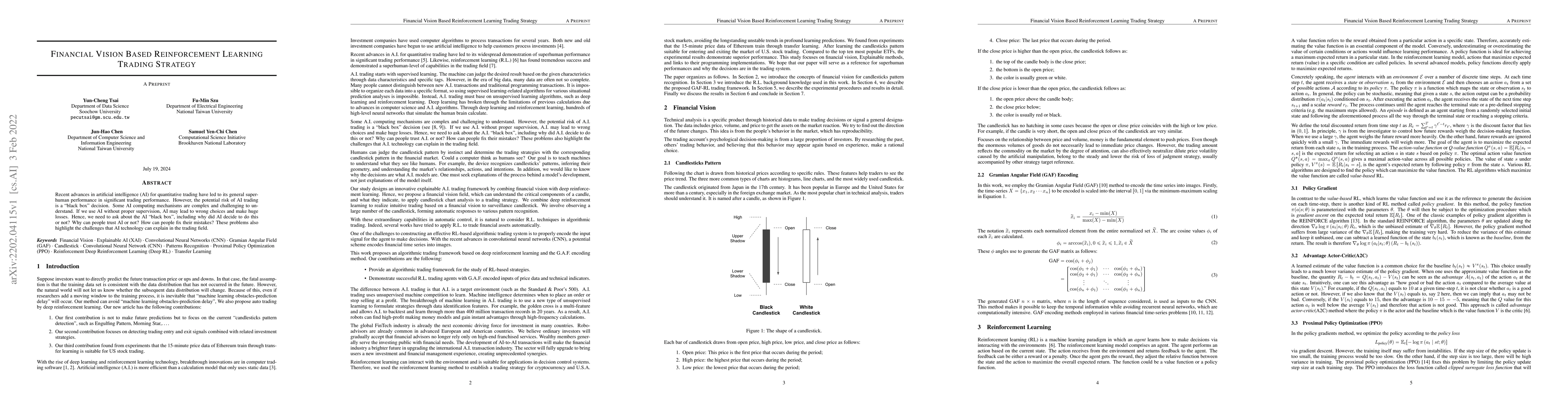

Recent advances in artificial intelligence (AI) for quantitative trading have led to its general superhuman performance in significant trading performance. However, the potential risk of AI trading ...

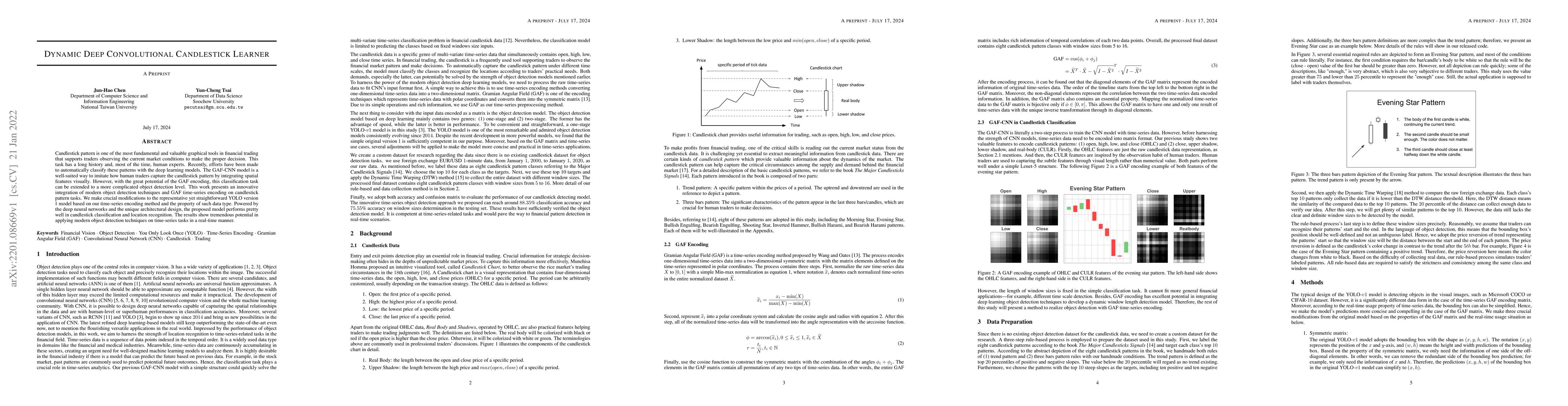

Candlestick pattern is one of the most fundamental and valuable graphical tools in financial trading that supports traders observing the current market conditions to make the proper decision. This t...

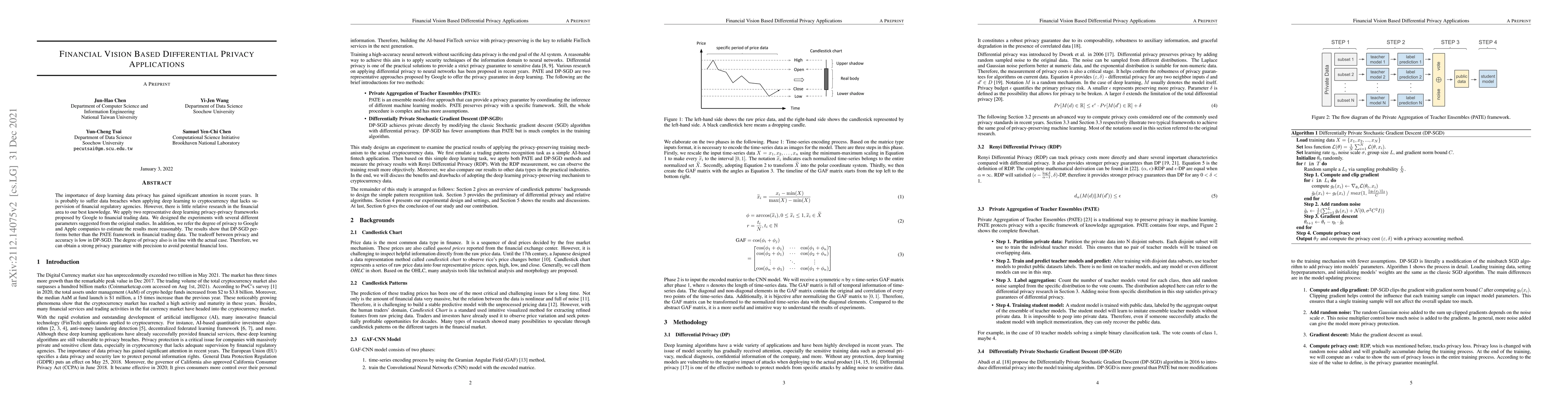

The importance of deep learning data privacy has gained significant attention in recent years. It is probably to suffer data breaches when applying deep learning to cryptocurrency that lacks supervi...

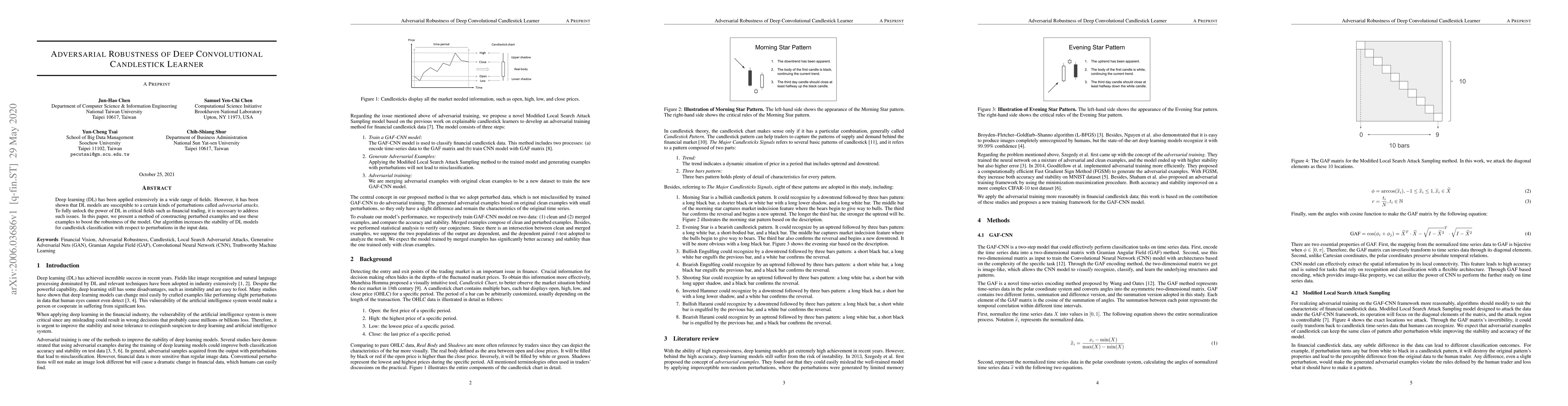

Deep learning (DL) has been applied extensively in a wide range of fields. However, it has been shown that DL models are susceptible to a certain kinds of perturbations called \emph{adversarial atta...

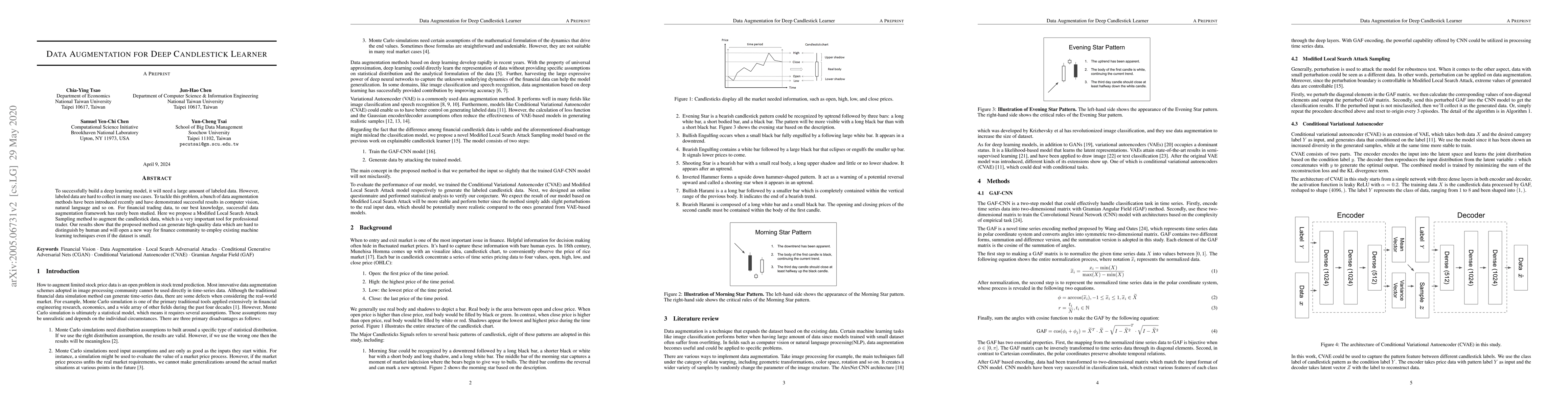

To successfully build a deep learning model, it will need a large amount of labeled data. However, labeled data are hard to collect in many use cases. To tackle this problem, a bunch of data augment...

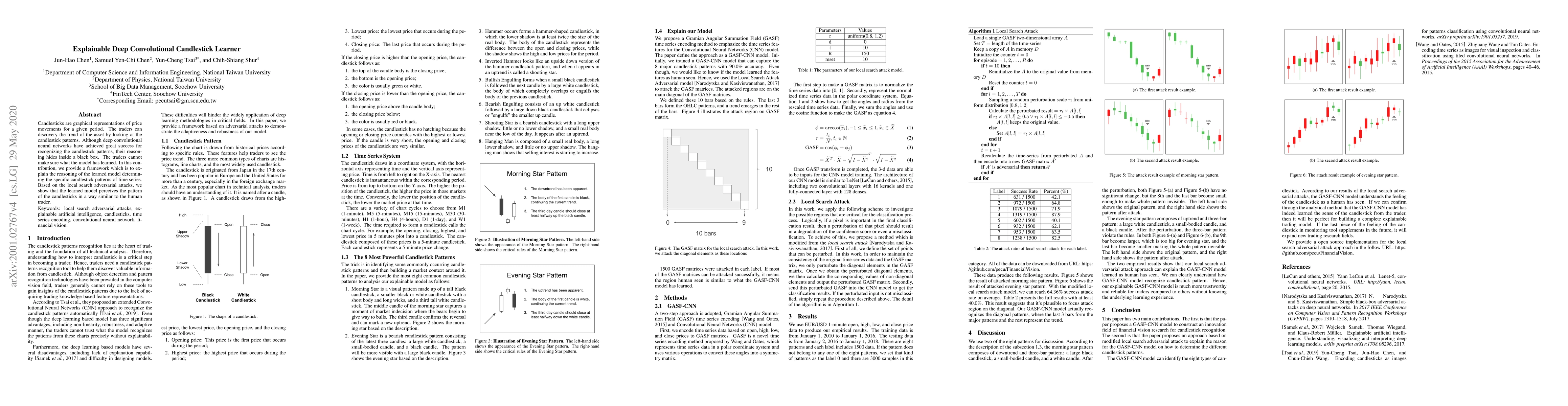

Candlesticks are graphical representations of price movements for a given period. The traders can discovery the trend of the asset by looking at the candlestick patterns. Although deep convolutional...

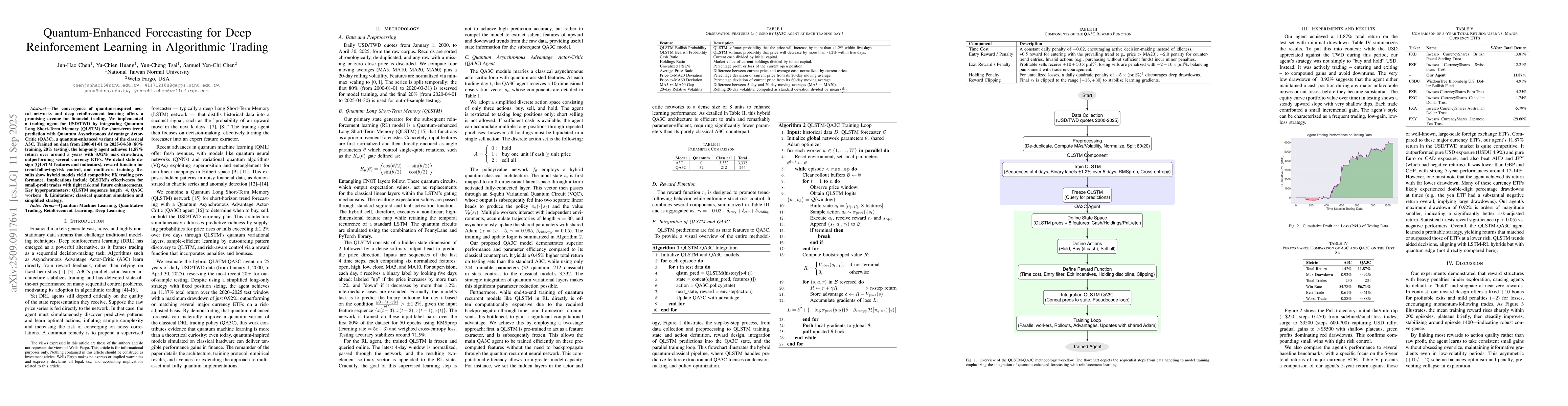

The convergence of quantum-inspired neural networks and deep reinforcement learning offers a promising avenue for financial trading. We implemented a trading agent for USD/TWD by integrating Quantum L...

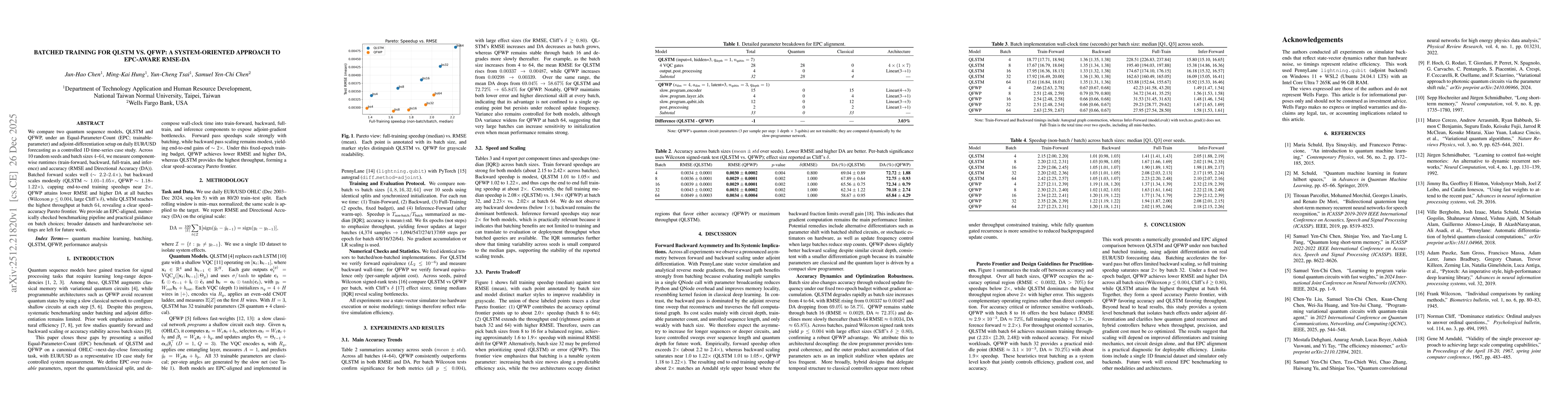

We compare two quantum sequence models, QLSTM and QFWP, under an Equal Parameter Count (EPC) and adjoint differentiation setup on daily EUR USD forecasting as a controlled one dimensional time series ...