Academic Profile

Statistics

Similar Authors

Papers on arXiv

We investigate a value-maximizing problem incorporating a human behavior pattern: present-biased-ness, for a firm which navigates strategic decisions encompassing earning retention/payout and capita...

This paper studies a type of periodic utility maximization for portfolio management in an incomplete market model, where the underlying price diffusion process depends on some external stochastic fa...

This paper studies some unconventional utility maximization problems when the ratio type relative portfolio performance is periodically evaluated over an infinite horizon. Meanwhile, the agent is pr...

We study a De Finetti's optimal dividend and capital injection problem under a Markov additive model. The surplus process before dividend and capital injection is assumed to follow a spectrally posi...

In this paper we consider the De Finetti's optimal dividend and capital injection problem under a Markov additive model. We assume that the surplus process before dividends and capital injections fo...

This paper studies De Finetti's optimal dividend problem with capital injection under spectrally positive Markov additive models. Based on dynamic programming principle, we first study an auxiliary ...

This paper studies a type of periodic utility maximization problems for portfolio management in incomplete stochastic factor models with convex trading constraints. The portfolio performance is period...

This paper studies an optimal consumption problem with both relaxed benchmark tracking and consumption drawdown constraint, leading to a stochastic control problem with dynamic state-control constrain...

In this paper, we examine a modified version of de Finetti's optimal dividend problem, incorporating fixed transaction costs and altering the surplus process by introducing two-valued drift and two-va...

This paper studies a type of consumption preference where some adjustment costs are incured whenever the past spending maximum and the past spending minimum records are updated. This preference can ca...

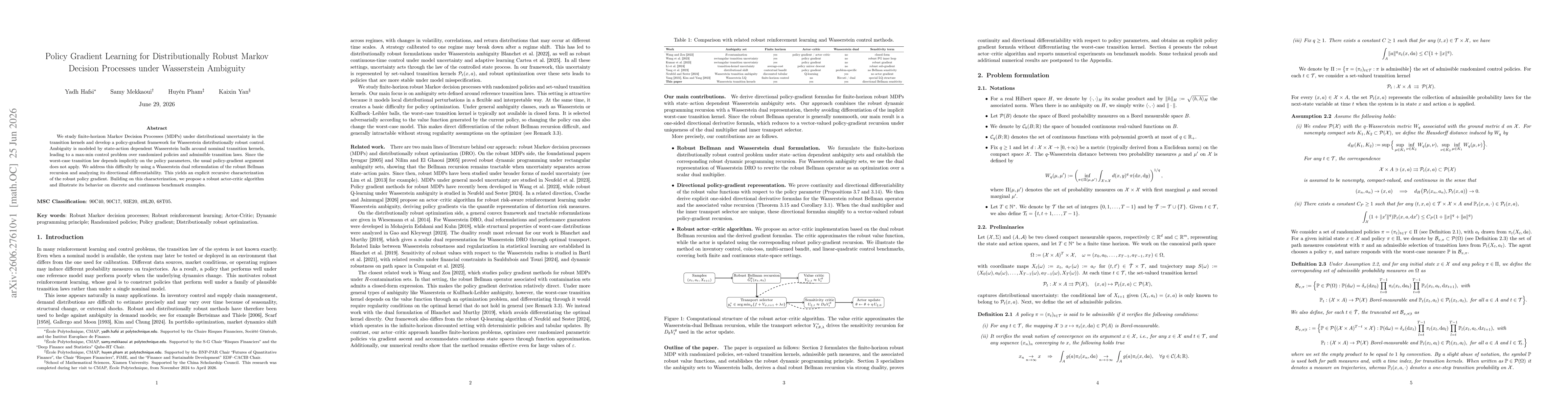

We study finite-horizon Markov Decision Processes (MDPs) under distributional uncertainty in the transition kernels and develop a policy-gradient framework for Wasserstein distributionally robust cont...

We study optimal portfolio and consumption in a regime-switching multi-name credit market with default contagion. Defaults generate portfolio losses and alter the intensities of surviving securities. ...