2

arXiv Papers

7

Total Publications

Profile

Academic Profile

Metrics

Statistics

2

arXiv Papers

7

Total Publications

Network

Similar Authors

Publications

Papers on arXiv

arXiv

Learning Financial Networks with High-frequency Trade Data

Financial networks are typically estimated by applying standard time series analyses to price-based economic variables collected at low-frequency (e.g., daily or monthly stock returns or realized vo...

arXiv

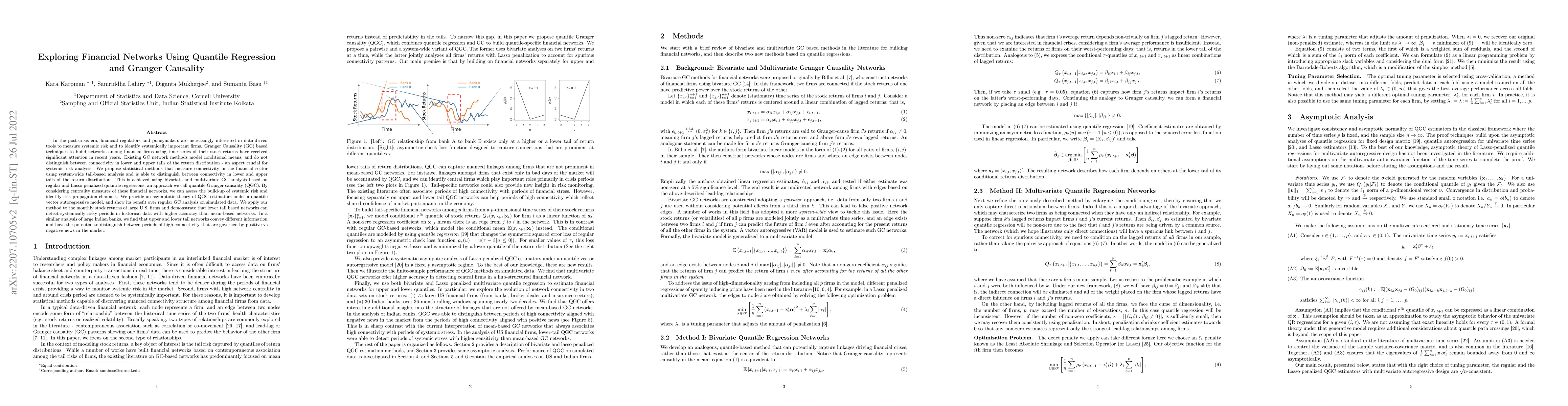

Exploring Financial Networks Using Quantile Regression and Granger

Causality

In the post-crisis era, financial regulators and policymakers are increasingly interested in data-driven tools to measure systemic risk and to identify systemically important firms. Granger Causalit...