Academic Profile

Statistics

Similar Authors

Papers on arXiv

Timely monetary policy decision-making requires timely core inflation measures. We create a new core inflation series that is explicitly designed to succeed at that goal. Precisely, we introduce the...

We reinvigorate maximum likelihood estimation (MLE) for macroeconomic density forecasting through a novel neural network architecture with dedicated mean and variance hemispheres. Our architecture f...

This paper examines the degree of integration at euro area financial markets. To that end, we estimate overall and country-specific integration indices based on a panel vector-autoregression with fa...

This paper introduces non-linear dimension reduction in factor-augmented vector autoregressions to analyze the effects of different economic shocks. I argue that controlling for non-linearities betw...

Macroeconomic data is characterized by a limited number of observations (small T), many time series (big K) but also by featuring temporal dependence. Neural networks, by contrast, are designed for ...

In this paper, we assess whether using non-linear dimension reduction techniques pays off for forecasting inflation in real-time. Several recent methods from the machine learning literature are adop...

This paper analyzes nonlinearities in the international transmission of financial shocks originating in the US. To do so, we develop a flexible nonlinear multi-country model. Our framework is capable ...

We propose a method to learn the nonlinear impulse responses to structural shocks using neural networks, and apply it to uncover the effects of US financial shocks. The results reveal substantial asym...

Machine learning predictions are typically interpreted as the sum of contributions of predictors. Yet, each out-of-sample prediction can also be expressed as a linear combination of in-sample values o...

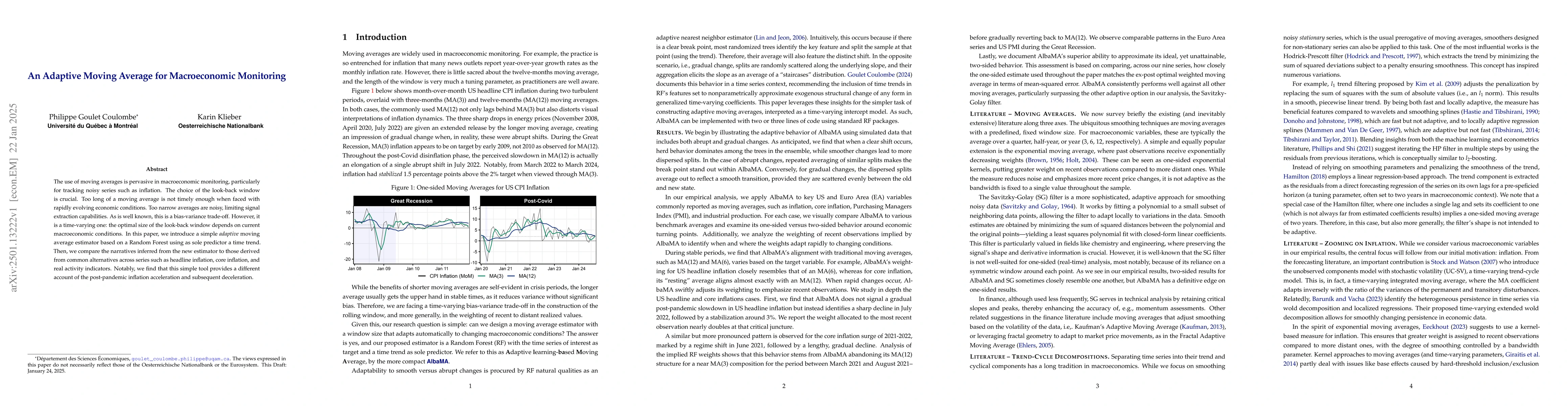

The use of moving averages is pervasive in macroeconomic monitoring, particularly for tracking noisy series such as inflation. The choice of the look-back window is crucial. Too long of a moving avera...

Local projections (LPs) are widely used in empirical macroeconomics to estimate impulse responses to policy interventions. Yet, in many ways, they are black boxes. It is often unclear what mechanism o...