Publication

Metrics

AI Quick Summary

This paper proposes an adaptive moving average estimator using a Random Forest model to dynamically adjust the look-back window based on current macroeconomic conditions, thereby offering a more timely and accurate signal extraction compared to traditional static methods. The results highlight its effectiveness in interpreting post-pandemic inflation trends differently from standard approaches.

Paper Preview

Abstract

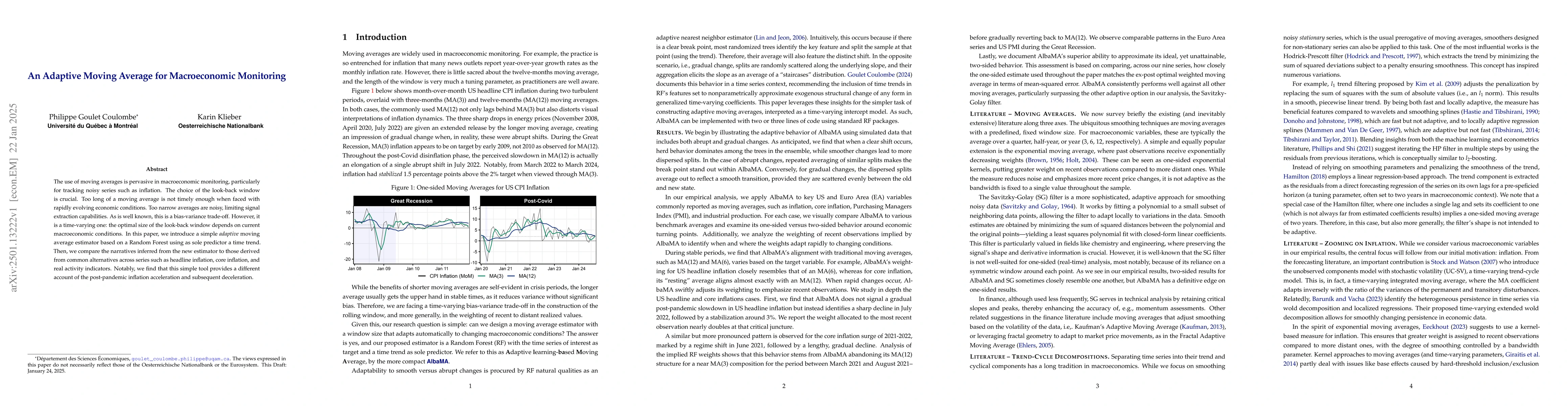

The use of moving averages is pervasive in macroeconomic monitoring, particularly for tracking noisy series such as inflation. The choice of the look-back window is crucial. Too long of a moving average is not timely enough when faced with rapidly evolving economic conditions. Too narrow averages are noisy, limiting signal extraction capabilities. As is well known, this is a bias-variance trade-off. However, it is a time-varying one: the optimal size of the look-back window depends on current macroeconomic conditions. In this paper, we introduce a simple adaptive moving average estimator based on a Random Forest using as sole predictor a time trend. Then, we compare the narratives inferred from the new estimator to those derived from common alternatives across series such as headline inflation, core inflation, and real activity indicators. Notably, we find that this simple tool provides a different account of the post-pandemic inflation acceleration and subsequent deceleration.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Authors

PDF Preview

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0