Academic Profile

Statistics

Similar Authors

Papers on arXiv

Timely monetary policy decision-making requires timely core inflation measures. We create a new core inflation series that is explicitly designed to succeed at that goal. Precisely, we introduce the...

We reinvigorate maximum likelihood estimation (MLE) for macroeconomic density forecasting through a novel neural network architecture with dedicated mean and variance hemispheres. Our architecture f...

When it comes to stock returns, any form of predictability can bolster risk-adjusted profitability. We develop a collaborative machine learning algorithm that optimizes portfolio weights so that the...

We use "glide charts" (plots of sequences of root mean squared forecast errors as the target date is approached) to evaluate and compare fixed-target forecasts of Arctic sea ice. We first use them t...

Rapidly diminishing Arctic summer sea ice is a strong signal of the pace of global climate change. We provide point, interval, and density forecasts for four measures of Arctic sea ice: area, extent...

Many problems plague the estimation of Phillips curves. Among them is the hurdle that the two key components, inflation expectations and the output gap, are both unobserved. Traditional remedies inc...

Stips, Macias, Coughlan, Garcia-Gorriz, and Liang (2016, Nature Scientific Reports) use information flows (Liang, 2008, 2014) to establish causality from various forcings to global temperature. We s...

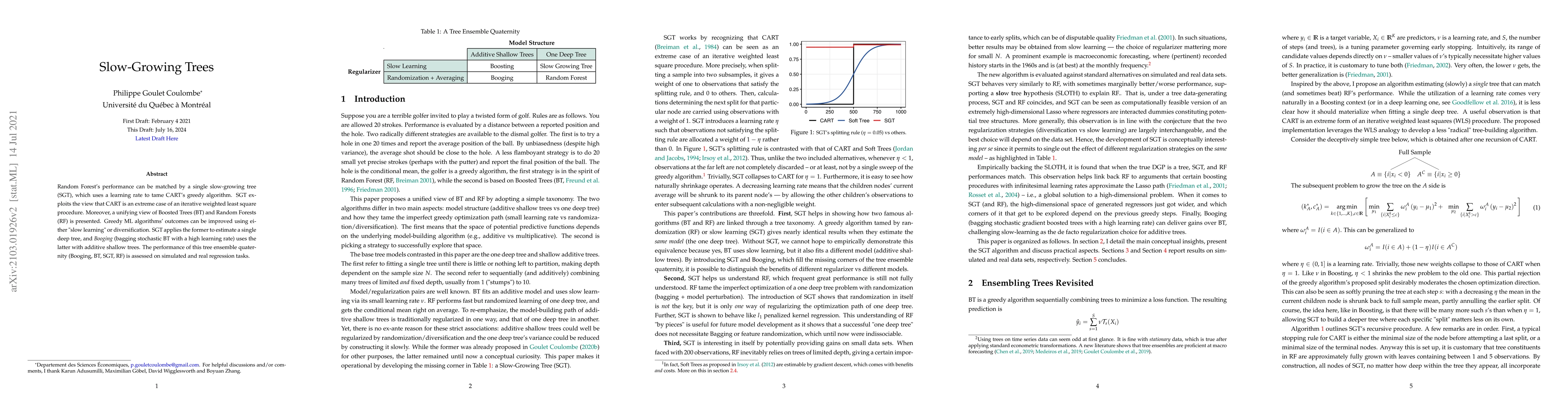

Random Forest's performance can be matched by a single slow-growing tree (SGT), which uses a learning rate to tame CART's greedy algorithm. SGT exploits the view that CART is an extreme case of an i...

Based on evidence gathered from a newly built large macroeconomic data set for the UK, labeled UK-MD and comparable to similar datasets for the US and Canada, it seems the most promising avenue for ...

Time-varying parameters (TVPs) models are frequently used in economics to capture structural change. I highlight a rather underutilized fact -- that these are actually ridge regressions. Instantly, ...

We move beyond "Is Machine Learning Useful for Macroeconomic Forecasting?" by adding the "how". The current forecasting literature has focused on matching specific variables and horizons with a part...

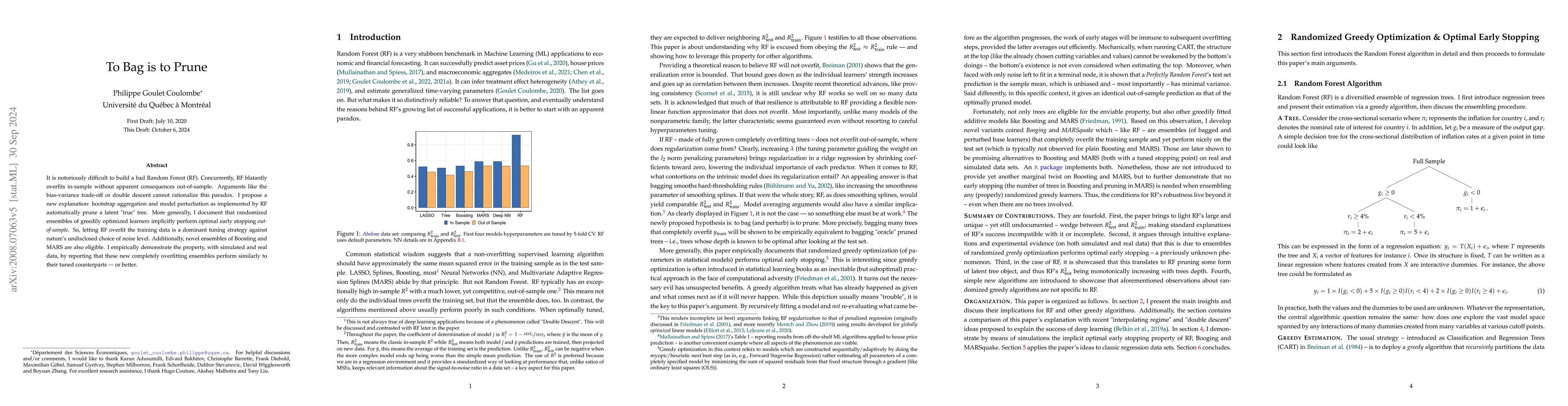

It is notoriously difficult to build a bad Random Forest (RF). Concurrently, RF blatantly overfits in-sample without any apparent consequence out-of-sample. Standard arguments, like the classic bias...

In a low-dimensional linear regression setup, considering linear transformations/combinations of predictors does not alter predictions. However, when the forecasting technology either uses shrinkage...

I develop Macroeconomic Random Forest (MRF), an algorithm adapting the canonical Machine Learning (ML) tool to flexibly model evolving parameters in a linear macro equation. Its main output, General...

Machine learning predictions are typically interpreted as the sum of contributions of predictors. Yet, each out-of-sample prediction can also be expressed as a linear combination of in-sample values o...

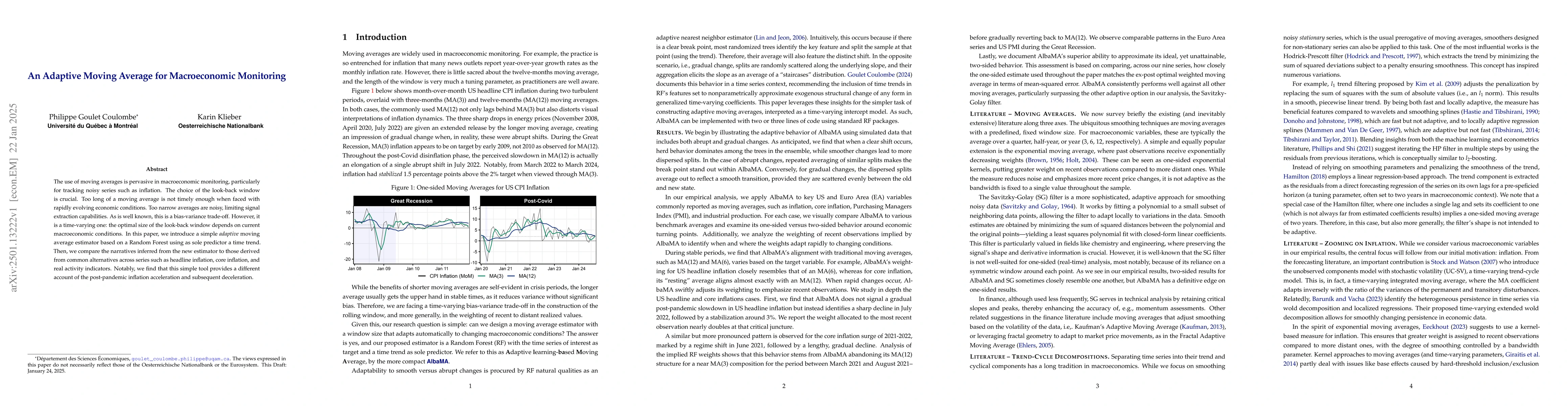

The use of moving averages is pervasive in macroeconomic monitoring, particularly for tracking noisy series such as inflation. The choice of the look-back window is crucial. Too long of a moving avera...

I show that ordinary least squares (OLS) predictions can be rewritten as the output of a restricted attention module, akin to those forming the backbone of large language models. This connection offer...

Local projections (LPs) are widely used in empirical macroeconomics to estimate impulse responses to policy interventions. Yet, in many ways, they are black boxes. It is often unclear what mechanism o...

Average forecast accuracy is not the same as forecast reliability. I treat forecast loss differentials relative to a benchmark as a return series. I then evaluate these returns using risk-adjusted per...

Needless to say, linear dynamics are pervasive in economic time series, particularly autoregressive ones. While gradient boosting with trees excels at capturing nonlinearities, it is inefficient in sm...