Academic Profile

Statistics

Similar Authors

Papers on arXiv

We study the optimal liquidation problem in a market model where the bid price follows a geometric pure jump process whose local characteristics are driven by an unobservable finite-state Markov cha...

We study the problem of a profit maximizing electricity producer who has to pay carbon taxes and who decides on investments into technologies for the abatement of carbon emissions in an environment ...

In this paper, we consider a discrete-time stochastic SIR model, where the transmission rate and the true number of infectious individuals are random and unobservable. An advantage of this model is ...

We study the optimal investment and proportional reinsurance problem of an insurance company, whose investment preferences are described via a forward dynamic utility of exponential type in a stocha...

In this paper, we study two optimisation settings for an insurance company, under the constraint that the terminal surplus at a deterministic and finite time $T$ follows a normal distribution with a...

In this paper we study the optimal investment and reinsurance problem of an insurance company whose investment preferences are described via a forward dynamic exponential utility in a regime-switchi...

We study optimal proportional reinsurance and investment strategies for an insurance company which experiences both ordinary and catastrophic claims and wishes to maximize the expected exponential u...

We study the optimal asset allocation problem for a fund manager whose compensation depends on the performance of her portfolio with respect to a benchmark. The objective of the manager is to maximi...

The objective of this paper is to study the filtering problem for a system of partially observable processes $(X, Y)$, where $X$ is a non-Markovian pure-jump process representing the signal and $Y$ ...

We study a dynamic portfolio optimization problem related to convergence trading, which is an investment strategy that exploits temporary mispricing by simultaneously buying relatively underpriced a...

This paper presents an optimal allocation problem in a financial market with one risk-free and one risky asset, when the market is driven by a stochastic market price of risk. We solve the problem i...

Reinsurance counterparty credit risk (RCCR) is the risk of a loss arising from the fact that a reinsurance company is unable to fulfill her contractual obligations towards the ceding insurer. RCCR i...

We investigate the optimal investment-reinsurance problem for insurance company with partial information on the market price of the risk. Through the use of filtering techniques we convert the origina...

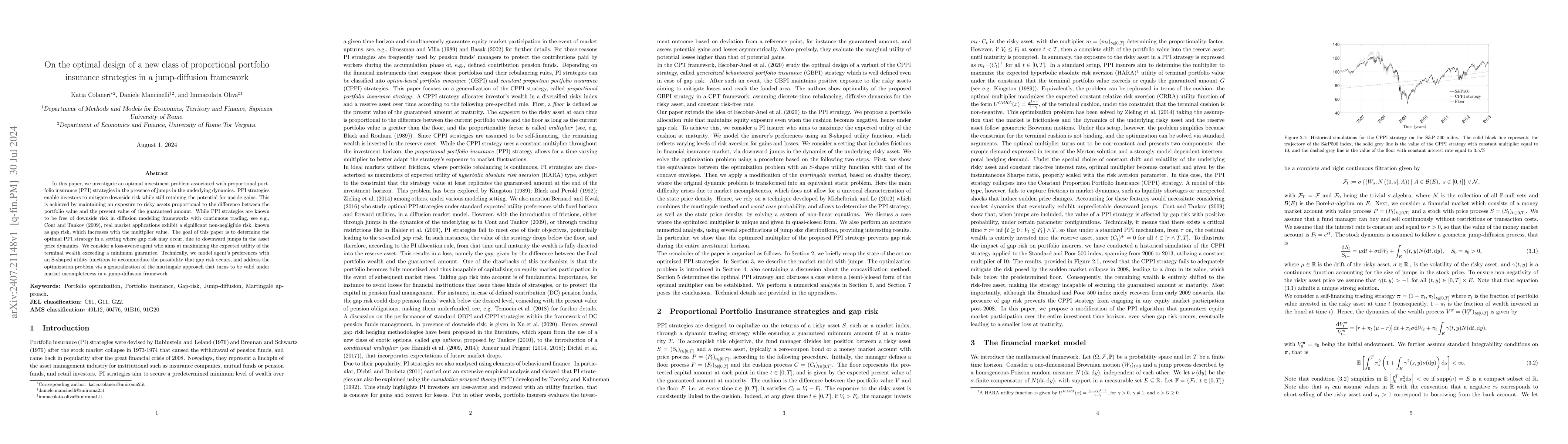

In this paper, we investigate an optimal investment problem associated with proportional portfolio insurance (PPI) strategies in the presence of jumps in the underlying dynamics. PPI strategies enable...

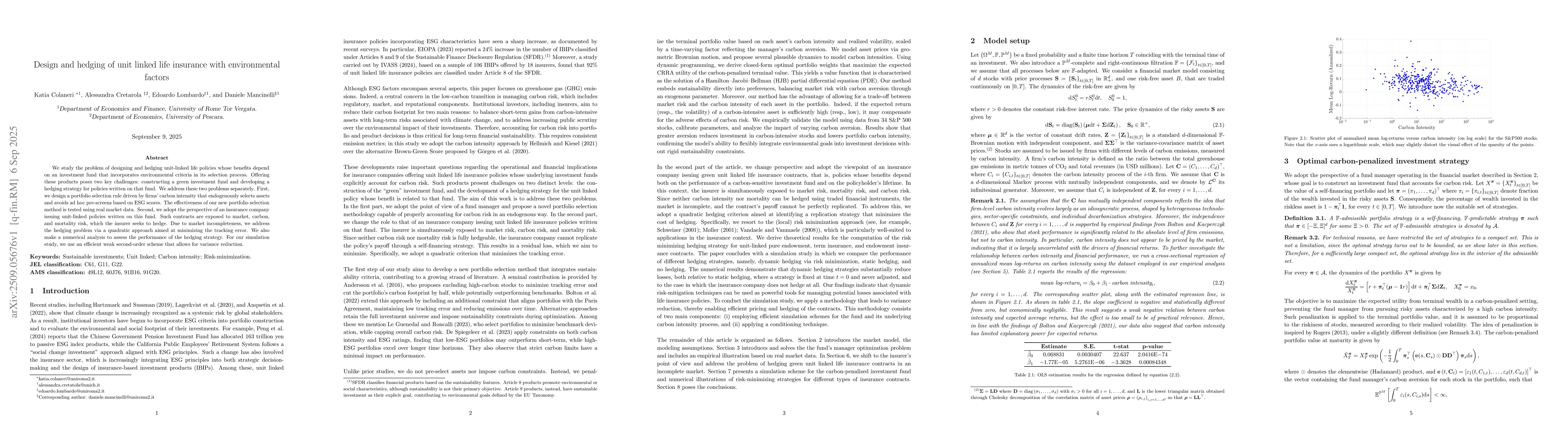

We study the problem of designing and hedging unit-linked life policies whose benefits depend on an investment fund that incorporates environmental criteria in its selection process. Offering these pr...

Given the increasing importance of environmental, social and governance (ESG) factors, particularly carbon emissions, we investigate optimal proportional portfolio insurance (PPI) strategies accountin...