Academic Profile

Statistics

Similar Authors

Papers on arXiv

The rapid advancement of large language models presents significant opportunities for financial applications, yet systematic evaluation in specialized financial contexts remains limited. This study pr...

Deep Research (DR) agents, powered by advanced Large Language Models (LLMs), have recently garnered increasing attention for their capability in conducting complex research tasks. However, existing li...

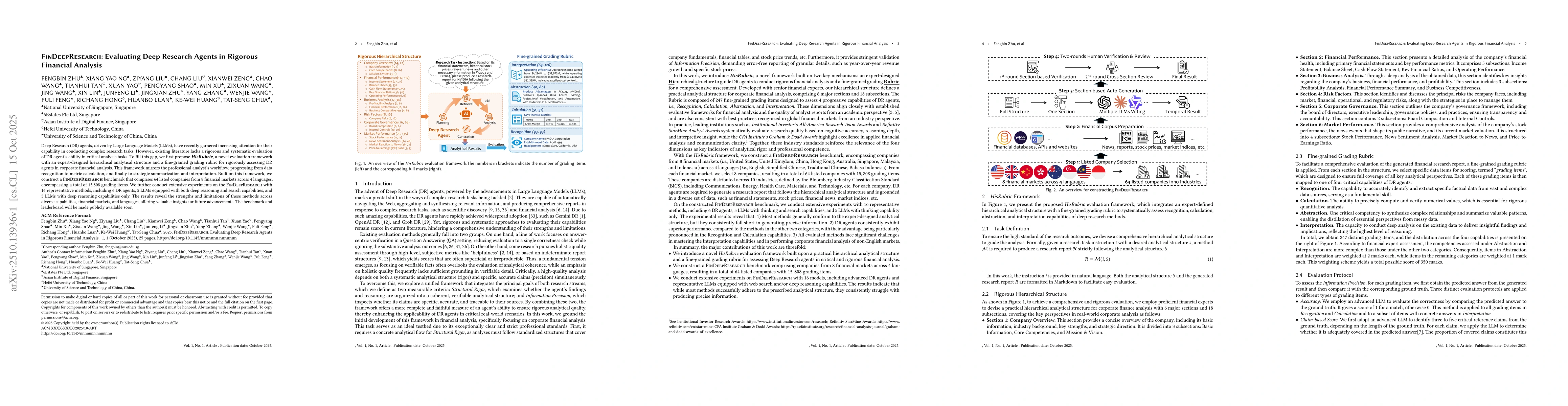

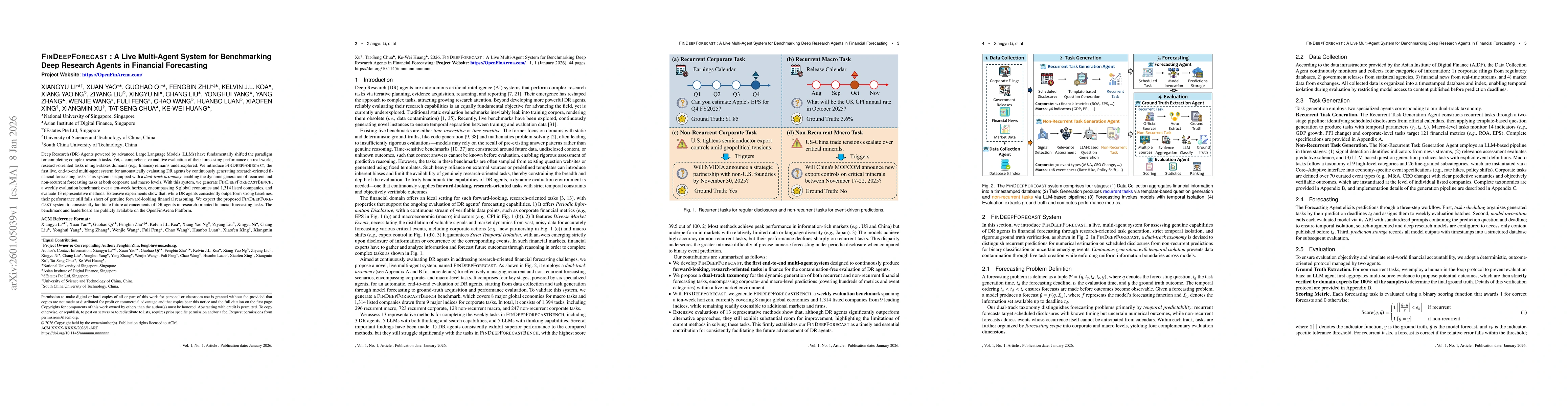

Deep Research (DR) Agents powered by advanced Large Language Models (LLMs) have fundamentally shifted the paradigm for completing complex research tasks. Yet, a comprehensive and live evaluation of th...

Natural Language Processing is rapidly evolving into a primary instrument for Computational Social Science, with researchers increasingly using embeddings to measure latent constructs such as novelty,...

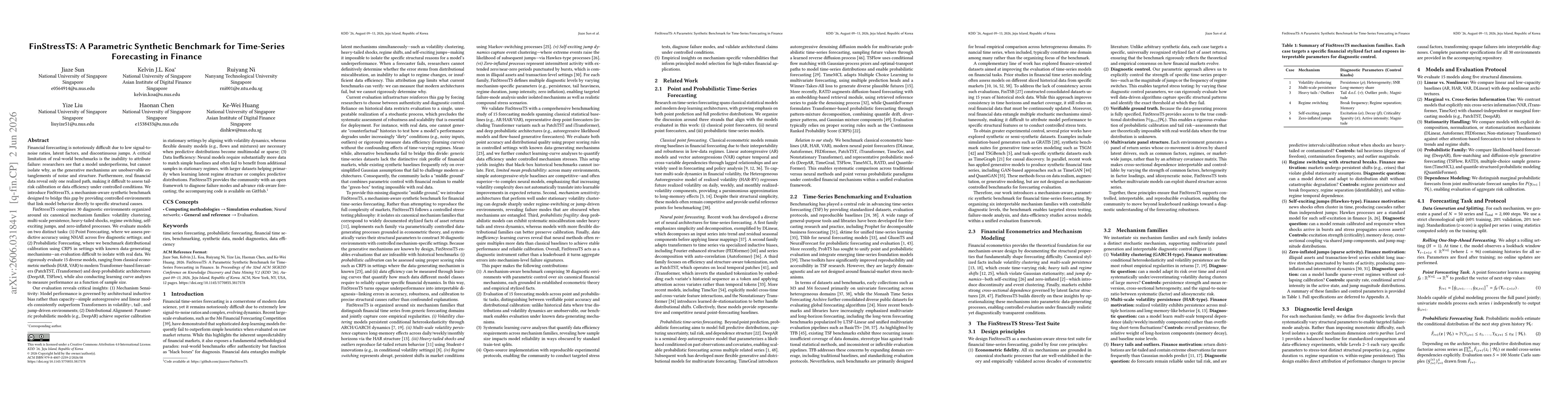

Financial forecasting is difficult due to low signal-to-noise ratios, latent factors, heavy tails, regime shifts, and jumps. Real-world benchmarks offer limited failure attribution: researchers can ob...