Academic Profile

Statistics

Similar Authors

Papers on arXiv

This paper extends the application of ESG score assessment methodologies from large corporations to individual farmers' production, within the context of climate change. Our proposal involves the in...

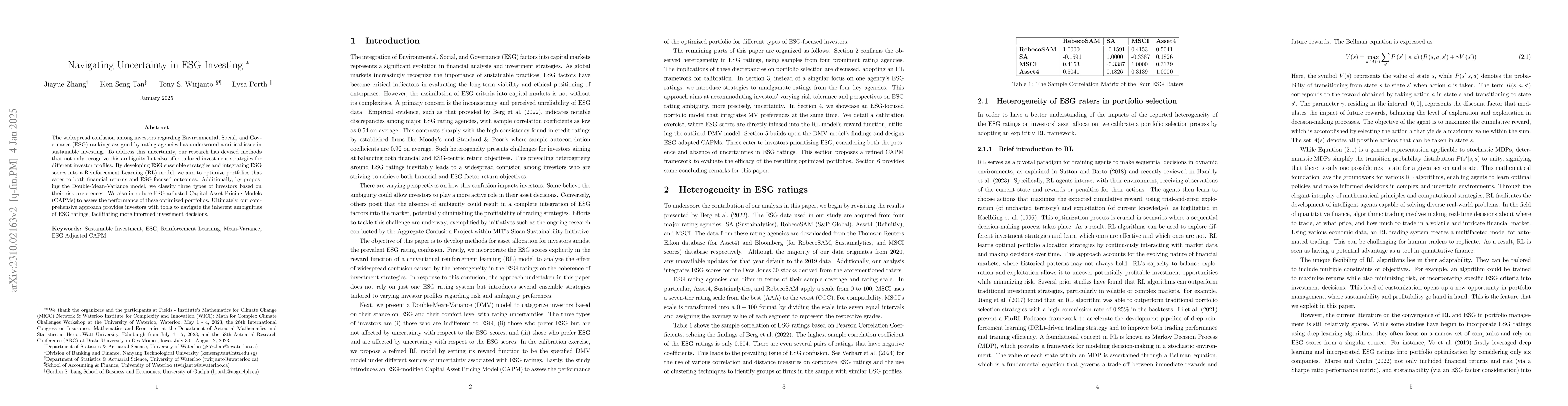

The widespread confusion among investors regarding Environmental, Social, and Governance (ESG) rankings assigned by rating agencies has underscored a critical issue in sustainable investing. To addr...

The replacement closeout convention has drawn more and more attention since the 2008 financial crisis. Compared with the conventional risk-free closeout, the replacement closeout convention incorpor...

In this paper, we study large losses arising from defaults of a credit portfolio. We assume that the portfolio dependence structure is modelled by the Archimedean copula family as opposed to the widel...

This paper investigates strategic investments needed to mitigate transition risks, particularly focusing on sectors significantly impacted by the shift to a low-carbon economy. It emphasizes the impor...