Academic Profile

Statistics

Similar Authors

Papers on arXiv

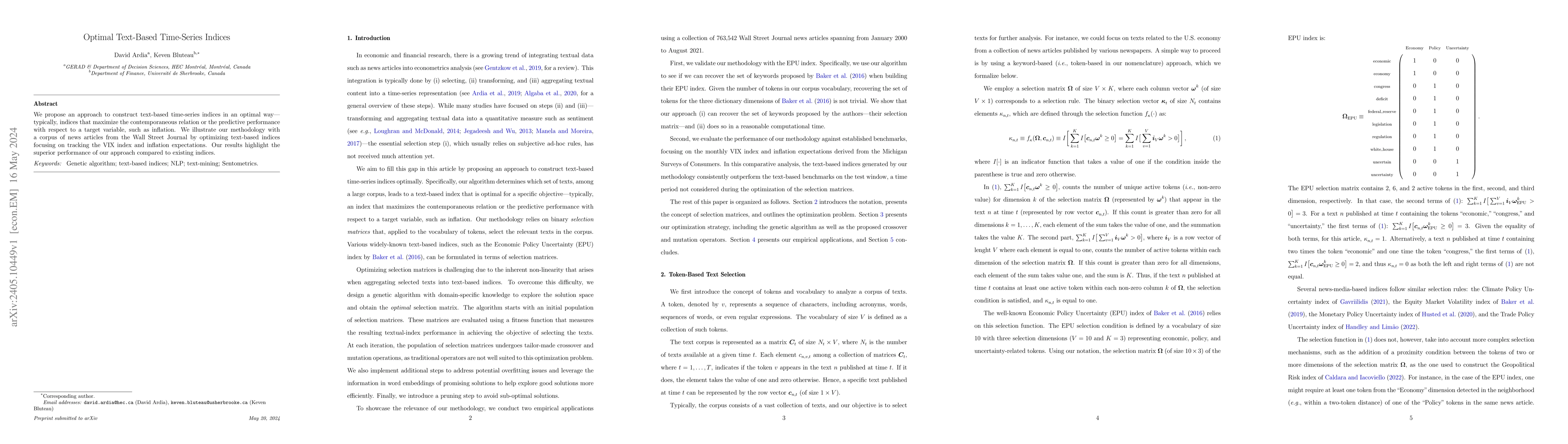

We propose an approach to construct text-based time-series indices in an optimal way--typically, indices that maximize the contemporaneous relation or the predictive performance with respect to a ta...

We examine the influence of Twitter promotion on cryptocurrency pump-and-dump events. By analyzing abnormal returns, trading volume, and tweet activity, we uncover that Twitter effectively garners a...

Using the peer-exposure ratio, we explore the factor exposure heterogeneity in green and brown stocks. By looking at peer groups of S&P 500 index firms over 2014-2020 based on their greenhouse gas e...

We explore the realized alpha-performance heterogeneity in green and brown stocks' universes using the peer performance ratios of Ardia and Boudt (2018). Focusing on S&P 500 index firms over 2014-20...

We study how the financial literature has evolved in scale, research team composition, and article topicality across 32 finance-focused academic journals from 1992 to 2021. We document that the fiel...

We provide a hands-on introduction to optimized textual sentiment indexation using the R package sentometrics. Textual sentiment analysis is increasingly used to unlock the potential information val...

We conduct a tone-based event study to examine the aggregate abnormal tone dynamics in media articles around earnings announcements. We test whether they convey incremental information that is usefu...