Academic Profile

Statistics

Similar Authors

Papers on arXiv

This paper presents the R package GAS for the analysis of time series under the Generalized Autoregressive Score (GAS) framework of Creal et al. (2013) and Harvey (2013). The distinctive feature of ...

GAS models have been recently proposed in time-series econometrics as valuable tools for signal extraction and prediction. This paper details how financial risk managers can use GAS models for Value...

The Minimum Covariance Determinant (MCD) approach robustly estimates the location and scatter matrix using the subset of given size with lowest sample covariance determinant. Its main drawback is th...

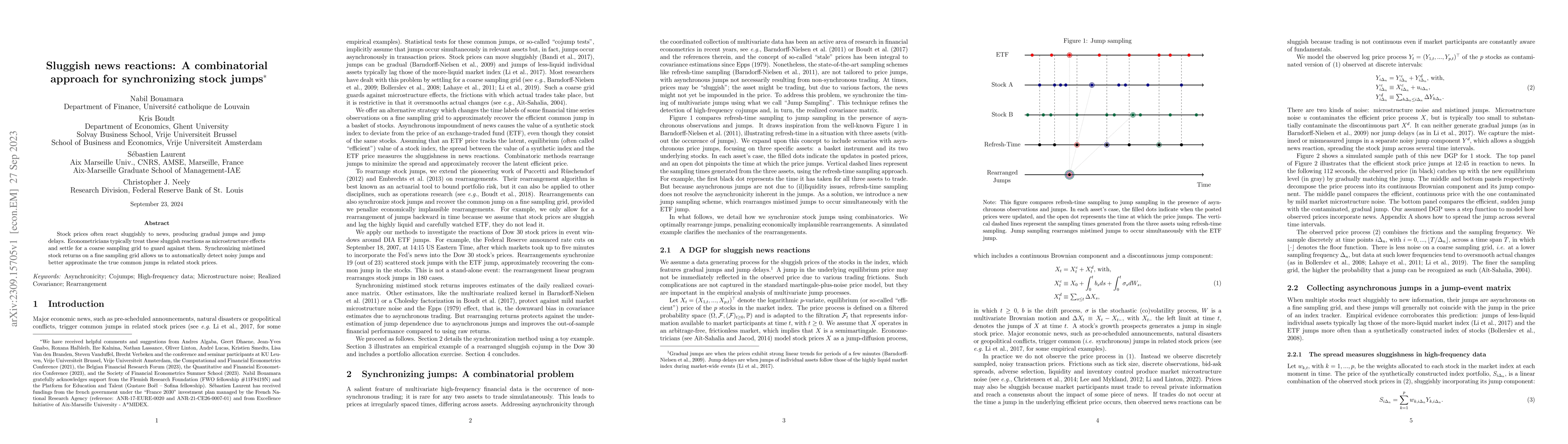

Stock prices often react sluggishly to news, producing gradual jumps and jump delays. Econometricians typically treat these sluggish reactions as microstructure effects and settle for a coarse sampl...

A novel generative machine learning approach for the simulation of sequences of financial price data with drawdowns quantifiably close to empirical data is introduced. Applications such as pricing d...

We provide a hands-on introduction to optimized textual sentiment indexation using the R package sentometrics. Textual sentiment analysis is increasingly used to unlock the potential information val...

We conduct a tone-based event study to examine the aggregate abnormal tone dynamics in media articles around earnings announcements. We test whether they convey incremental information that is usefu...