Academic Profile

Statistics

Similar Authors

Papers on arXiv

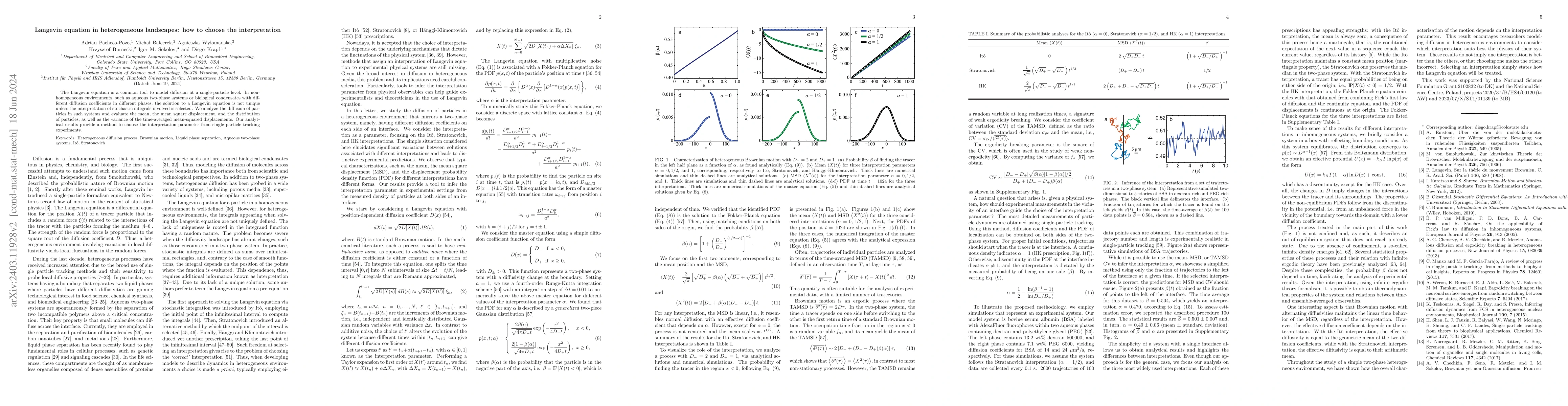

The Langevin equation is a common tool to model diffusion at a single-particle level. In non-homogeneous environments, such as aqueous two-phase systems or biological condensates with different diff...

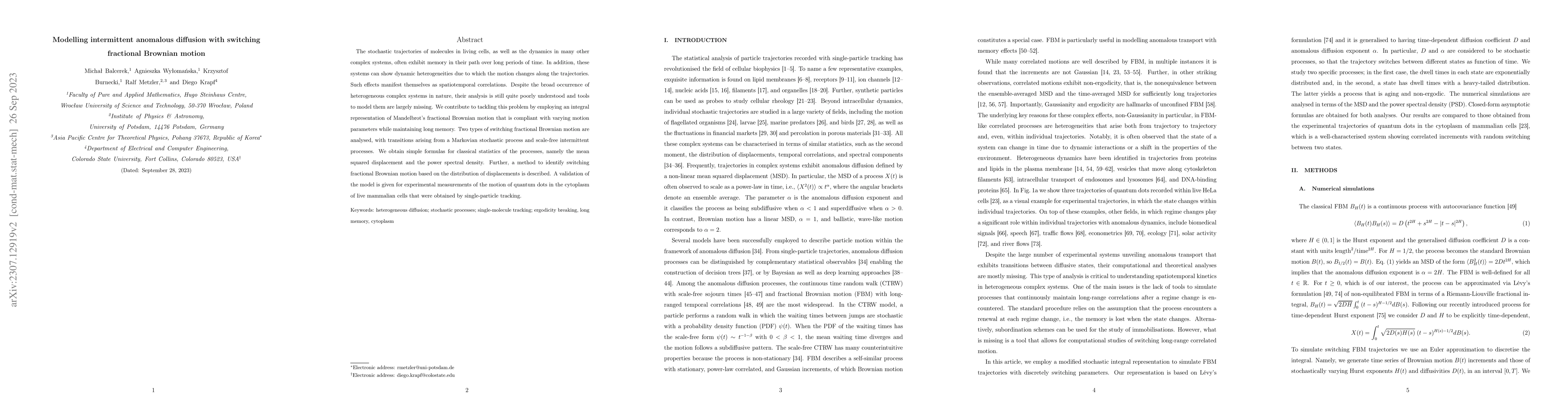

The stochastic trajectories of molecules in living cells, as well as the dynamics in many other complex systems, often exhibit memory in their path over long periods of time. In addition, these syst...

In this paper, we generalise the results presented in the literature for the ruin probability for the insurer--reinsurer model under a pro-rata reinsurance contract. We consider claim amounts that a...

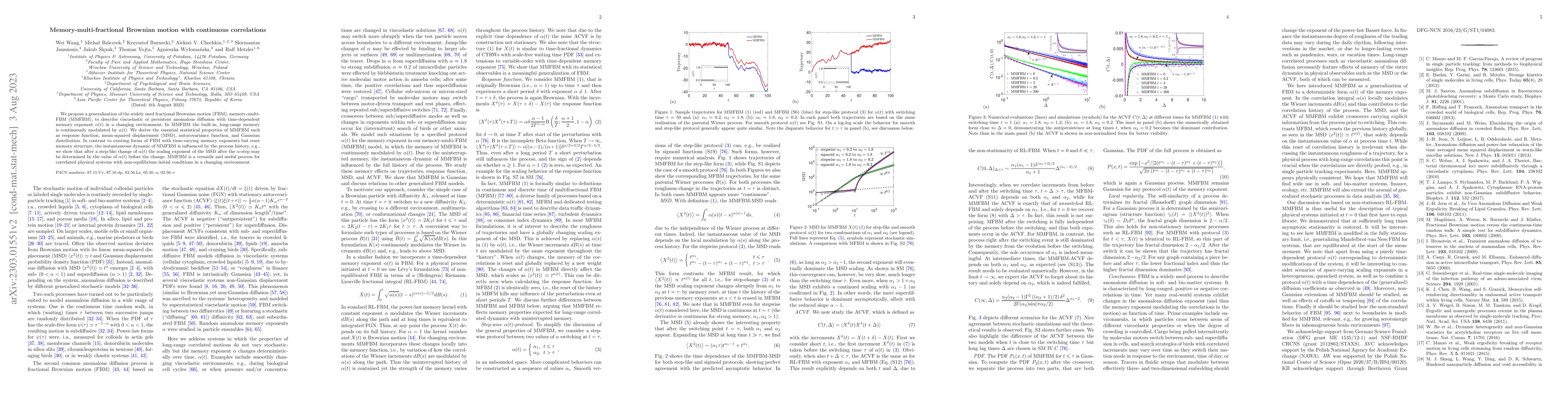

We propose a generalization of the widely used fractional Brownian motion (FBM), memory-multi-FBM (MMFBM), to describe viscoelastic or persistent anomalous diffusion with time-dependent memory expon...

Fractional Brownian motion, a Gaussian non-Markovian self-similar process with stationary long-correlated increments, has been identified to give rise to the anomalous diffusion behavior in a great ...

Fractional Brownian motion (FBM) is the only Gaussian self-similar process with stationary increments. Its increment process, called fractional Gaussian noise, is ergodic and exhibits a property of ...

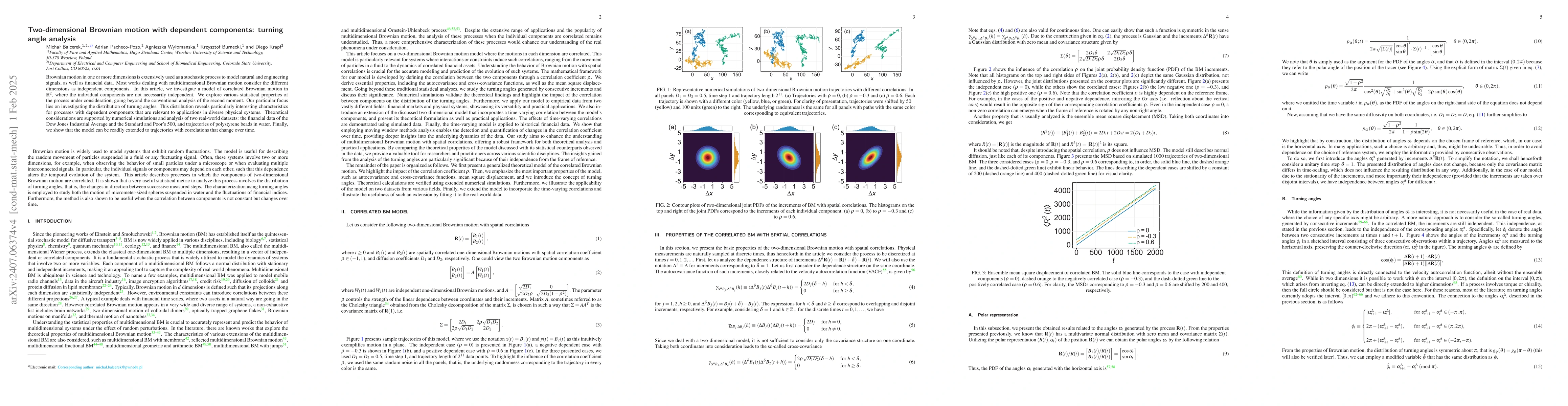

Brownian motion in one or more dimensions is extensively used as a stochastic process to model natural and engineering signals, as well as financial data. Most works dealing with multidimensional Brow...

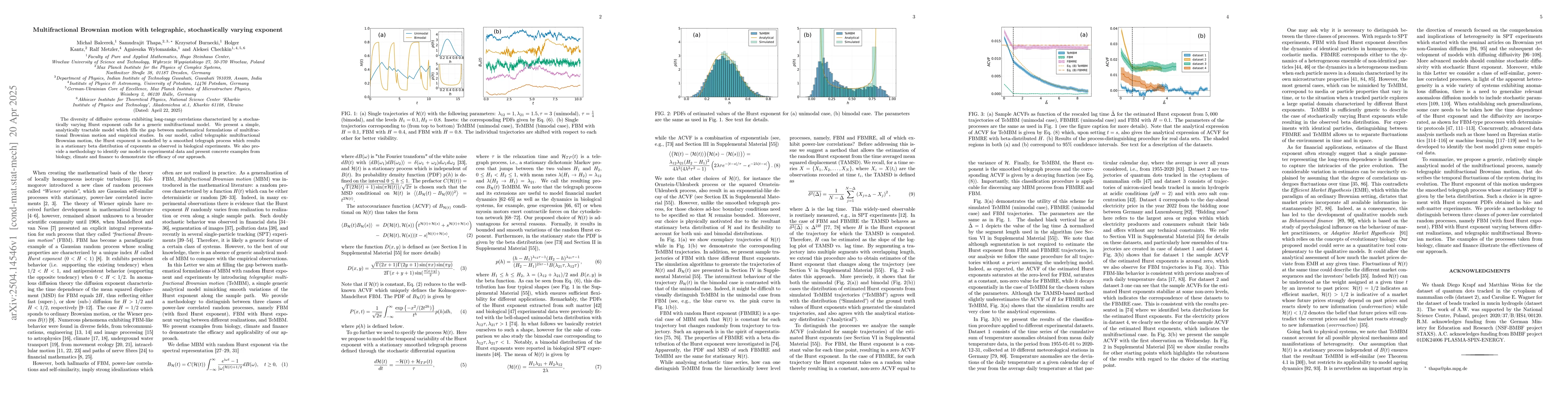

The diversity of diffusive systems exhibiting long-range correlations characterized by a stochastically varying Hurst exponent calls for a generic multifractional model. We present a simple, analytica...

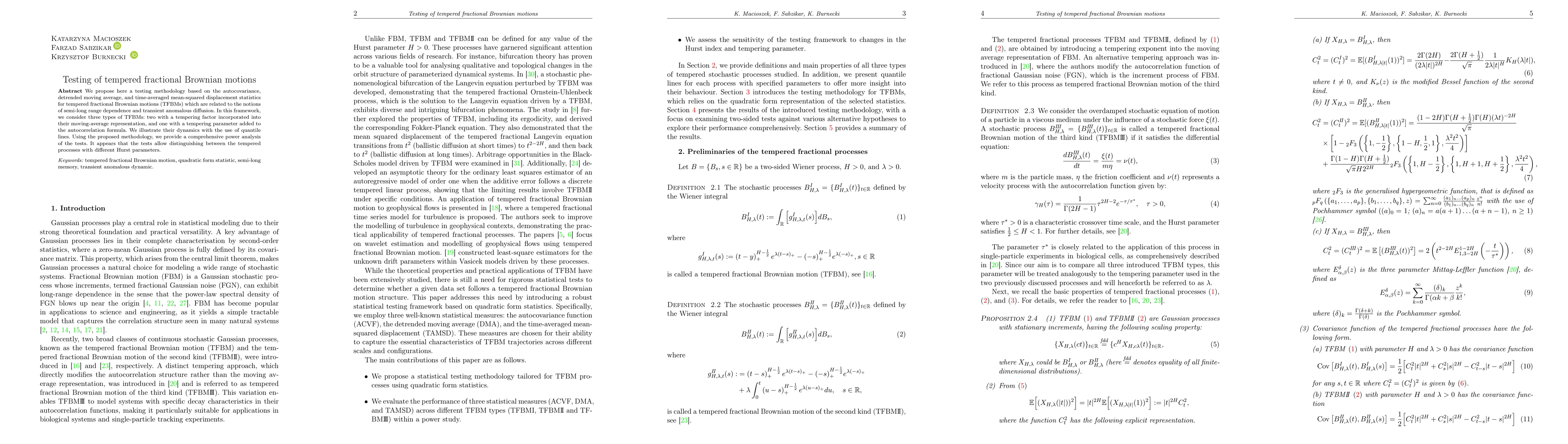

We propose here a testing methodology based on the autocovariance, detrended moving average, and time-averaged mean-squared displacement statistics for tempered fractional Brownian motions (TFBMs) whi...

This article introduces a novel construction of the two-dimensional fractional Brownian motion (2D fBm) with dependent components. Unlike similar models discussed in the literature, our approach uniqu...

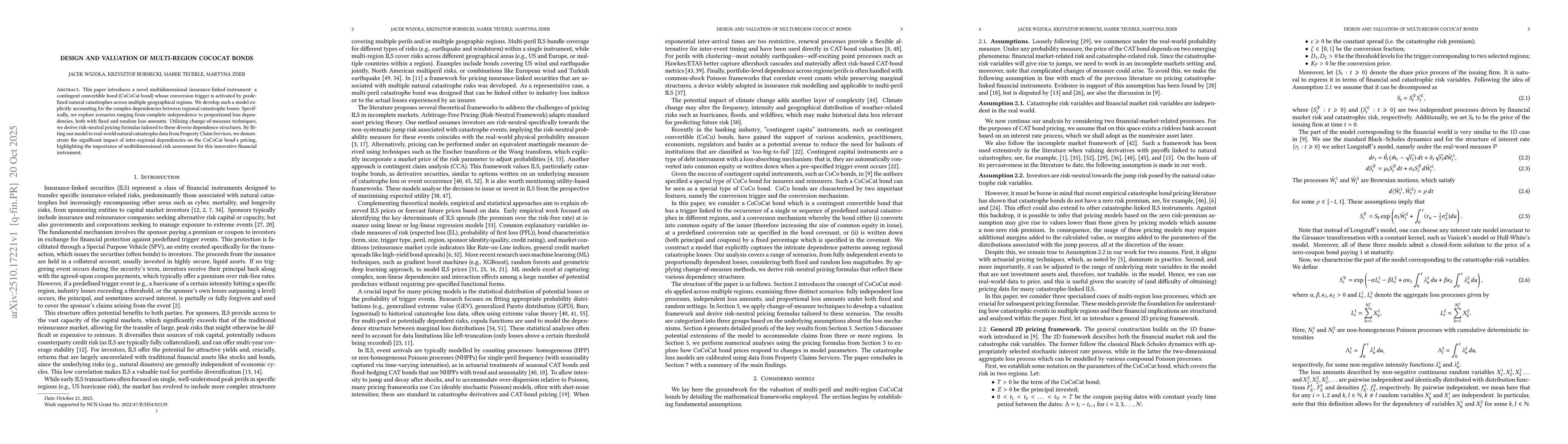

This paper introduces a novel multidimensional insurance-linked instrument: a contingent convertible bond (CoCoCat bond) whose conversion trigger is activated by predefined natural catastrophes across...

The insurance-linked securities (ILS) market, as a form of alternative risk transfer, has been at the forefront of innovative risk-transfer solutions. The catastrophe bond (CAT bond) market now repres...

In recent years, the growing frequency and severity of natural disasters have increased the need for effective tools to manage catastrophe risk. Catastrophe (CAT) bonds allow the transfer of part of t...