Academic Profile

Statistics

Similar Authors

Papers on arXiv

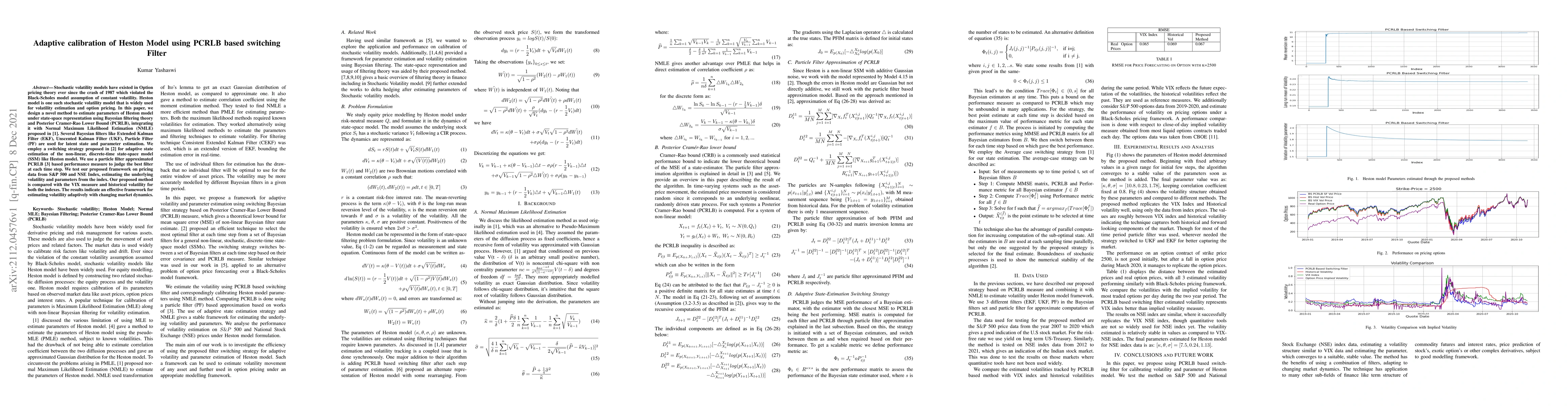

Stochastic volatility models have existed in Option pricing theory ever since the crash of 1987 which violated the Black-Scholes model assumption of constant volatility. Heston model is one such sto...

The use of Bayesian filtering has been widely used in mathematical finance, primarily in Stochastic Volatility models. They help in estimating unobserved latent variables from observed market data. ...

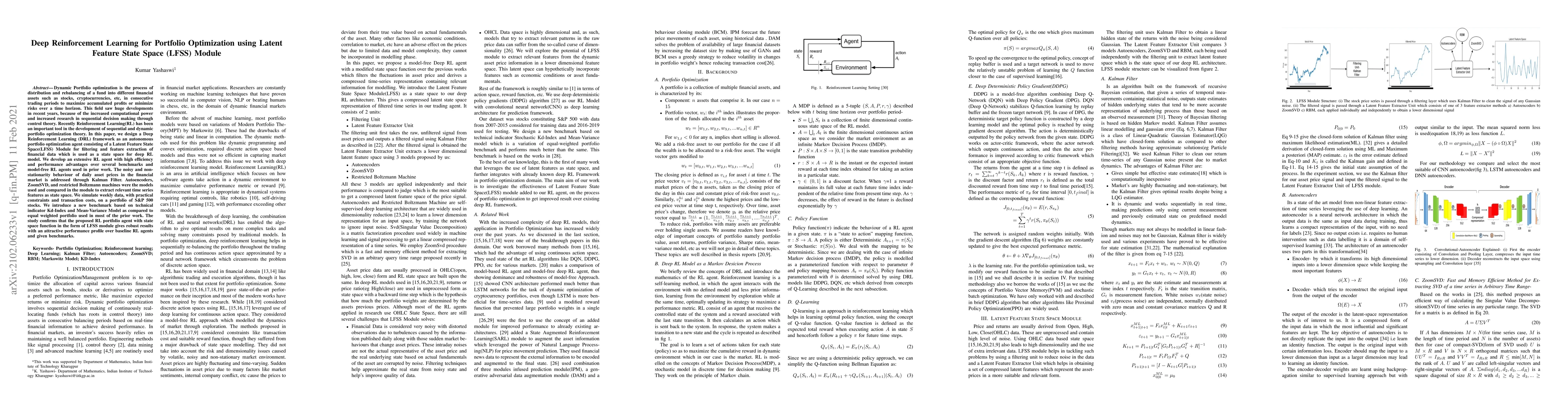

Dynamic Portfolio optimization is the process of distribution and rebalancing of a fund into different financial assets such as stocks, cryptocurrencies, etc, in consecutive trading periods to maxim...