Academic Profile

Statistics

Similar Authors

Papers on arXiv

In this paper, we develop two families of sequential monitoring procedure to (timely) detect changes in a GARCH(1,1) model. Whilst our methodologies can be applied for the general analysis of change...

We propose a family of CUSUM-based statistics to detect the presence of changepoints in the deterministic part of the autoregressive parameter in a Random Coefficient AutoRegressive (RCA) sequence. ...

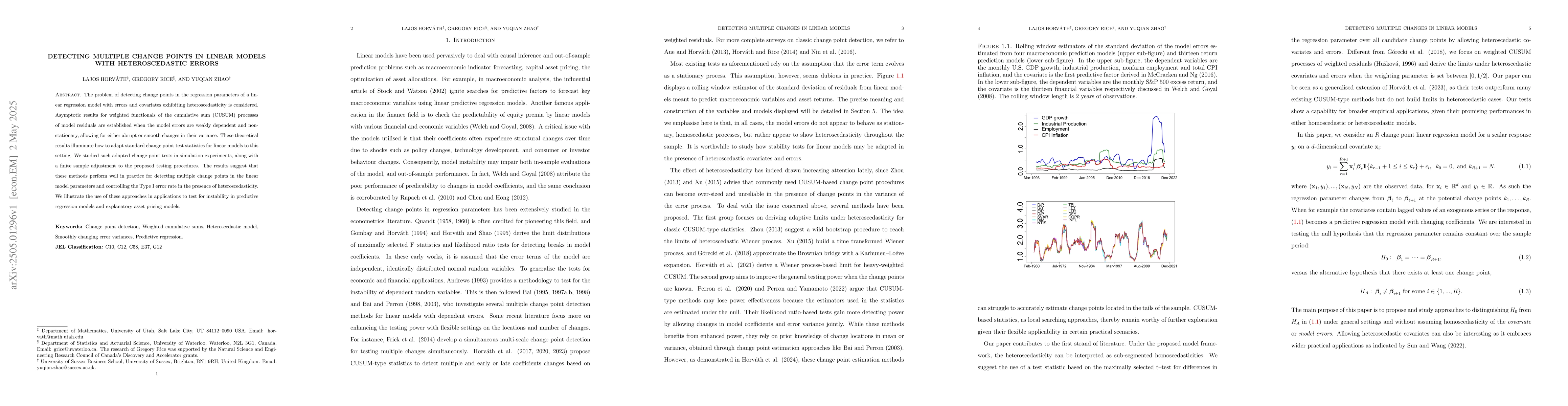

The problem of detecting change points in the regression parameters of a linear regression model with errors and covariates exhibiting heteroscedasticity is considered. Asymptotic results for weighted...

We investigate the online detection of changepoints in the distribution of a sequence of observations using degenerate U-statistic-type processes. We study weighted versions of: an ordinary, CUSUM-typ...