Academic Profile

Statistics

Similar Authors

Papers on arXiv

We study a robust utility maximization problem in a general discrete-time frictionless market. The investor is assumed to have a random, nonconcave and nondecreasing utility function, which may or m...

We study a robust utility maximization problem in a general discrete-time frictionless market under quasi-sure no-arbitrage. The investor is assumed to have a random and concave utility function def...

We investigate an expected utility maximization problem under model uncertainty in a one-period financial market. We capture model uncertainty by replacing the baseline model $\mathbb{P}$ with an ad...

In the frictionless discrete time financial market of Bouchard and Nutz (2015), we propose a full characterization of the quasi-sure super-replication price: as the supremum of the mono-prior super-...

When uncertainty is modelled by a set of non-dominated and non-compact probability measures, a notion of essential supremum for a family of real-valued functions is developed in terms of upper semi-...

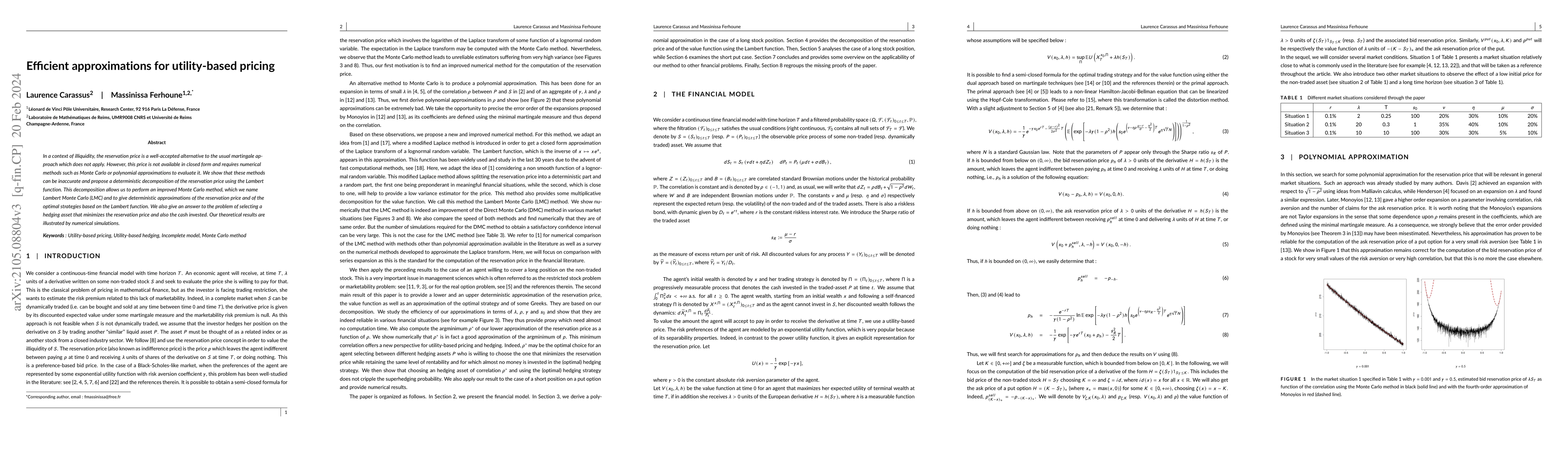

In a context of illiquidity, the reservation price is a well-accepted alternative to the usual martingale approach which does not apply. However, this price is not available in closed form and requi...

In a discrete time setting, we study the central problem of giving a fair price to some financial product. For several decades, the no-arbitrage conditions and the martingale measures have played a ...

We study the most famous example of a large financial market: the Arbitrage Pricing Model, where investors can trade in a one-period setting with countably many assets admitting a factor structure. ...

We consider infinite dimensional optimization problems motivated by the financial model called Arbitrage Pricing Theory. Using probabilistic and functional analytic tools, we provide a dual characte...

In a discrete time and multiple-priors setting, we propose a new characterisation of the condition of quasi-sure no-arbitrage which has become a standard assumption. This characterisation shows that...

Drawing from set theory, this article contributes to a deeper understanding of the no-arbitrage principle in multiple-priors settings and its application in mathematical finance. In the quasi-sure d...

We study projective functions. We prove that projective functions generalise lower and upper-semianalytic ones while being stable by composition and difference. We show that the class of projective fu...

We consider an investor who, while maximizing his/her expected utility, also compares the outcome to a reference entity. We recall the notion of personal equilibrium and show that, in a multistep, gen...