Academic Profile

Statistics

Similar Authors

Papers on arXiv

High-dimensional penalized rank regression is a powerful tool for modeling high-dimensional data due to its robustness and estimation efficiency. However, the non-smoothness of the rank loss brings ...

We aim to develop simultaneous inference tools for the mean function of functional data from sparse to dense. First, we derive a unified Gaussian approximation to construct simultaneous confidence b...

It is of importance to investigate the significance of a subset of covariates $W$ for the response $Y$ given covariates $Z$ in regression modeling. To this end, we propose a significance test for th...

We develop a novel methodology for detecting abrupt break points in mean functions of functional time series, adaptable to arbitrary sampling schemes. By employing B-spline smoothing, we introduce $\m...

In this paper, we investigate the adequacy testing problem of high-dimensional factor-augmented regression model. Existing test procedures perform not well under dense alternatives. To address this cr...

In this paper, we present a general framework for testing relevant hypotheses in functional time series. Our unified approach covers one-sample, two-sample, and change point problems under contaminate...

In this paper, we investigate federated learning for quantile inference under local differential privacy (LDP). We propose an estimator based on local stochastic gradient descent (SGD), whose local gr...

We establish a strong Gaussian approximation for high-dimensional non-degenerate U-statistics with diverging dimension. Under mild assumptions, we construct, on a sufficiently rich probability space, ...

We study asymptotic anytime-valid confidence sequences for degree-two U-statistics under continuous monitoring. In the nondegenerate case, Hoeffding's projection reduces the problem to a time-uniform ...

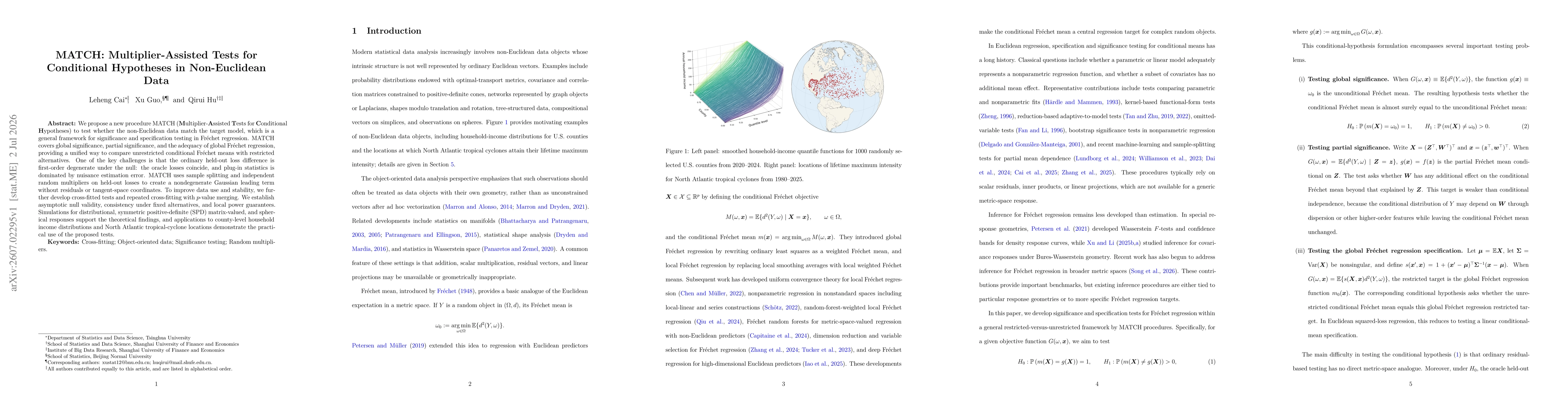

We propose a new procedure MATCH (Multiplier-Assisted Tests for Conditional Hypotheses) to test whether the non-Euclidean data match the target model, which is a general framework for significance and...