Academic Profile

Statistics

Similar Authors

Papers on arXiv

We propose a new, data-driven approach for efficient pricing of - fixed- and float-strike - discrete arithmetic Asian and Lookback options when the underlying process is driven by the Heston model d...

We propose a methodology to sample from time-integrated stochastic bridges, namely random variables defined as $\int_{t_1}^{t_2} f(Y(t))dt$ conditioned on $Y(t_1)\!=\!a$ and $Y(t_2)\!=\!b$, with $a,...

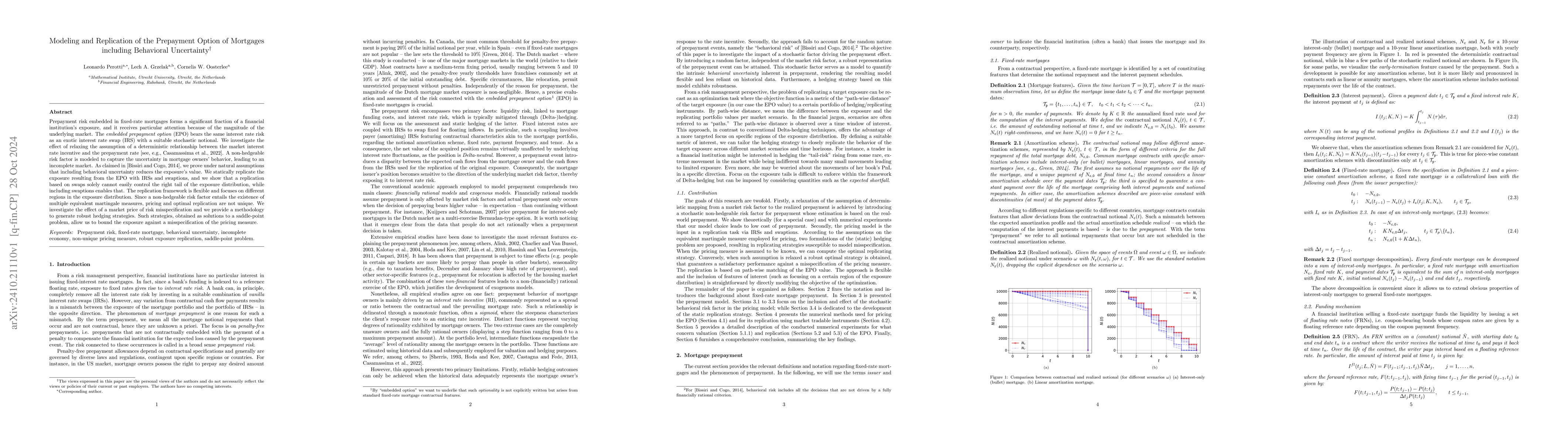

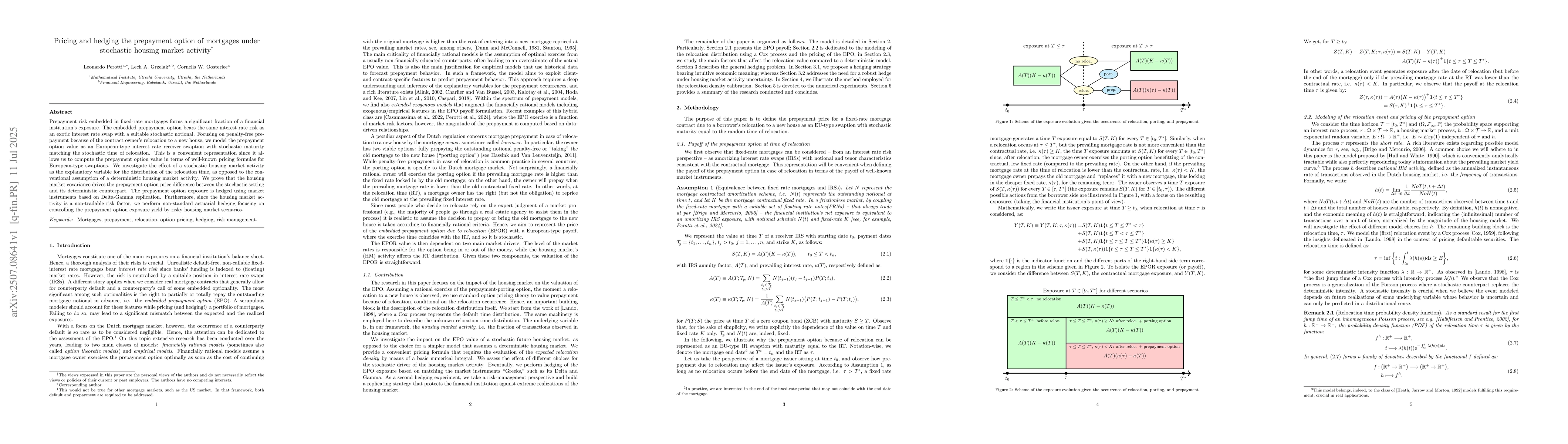

Prepayment risk embedded in fixed-rate mortgages forms a significant fraction of a financial institution's exposure, and it receives particular attention because of the magnitude of the underlying mar...

It is a market practice to express market-implied volatilities in some parametric form. The most popular parametrizations are based on or inspired by an underlying stochastic model, like the Heston mo...

Prepayment risk embedded in fixed-rate mortgages forms a significant fraction of a financial institution's exposure. The embedded prepayment option bears the same interest rate risk as an exotic inter...