Academic Profile

Statistics

Similar Authors

Papers on arXiv

This paper studies the optimization of Markov decision processes (MDPs) from a risk-seeking perspective, where the risk is measured by conditional value-at-risk (CVaR). The objective is to find a po...

Dynamic optimization of mean and variance in Markov decision processes (MDPs) is a long-standing challenge caused by the failure of dynamic programming. In this paper, we propose a new approach to f...

The bailout strategy is crucial to cushion the massive loss caused by systemic risk in the financial system. There is no closed-form formulation of the optimal bailout problem, making solving it dif...

CVaR (Conditional Value at Risk) is a risk metric widely used in finance. However, dynamically optimizing CVaR is difficult since it is not a standard Markov decision process (MDP) and the principle...

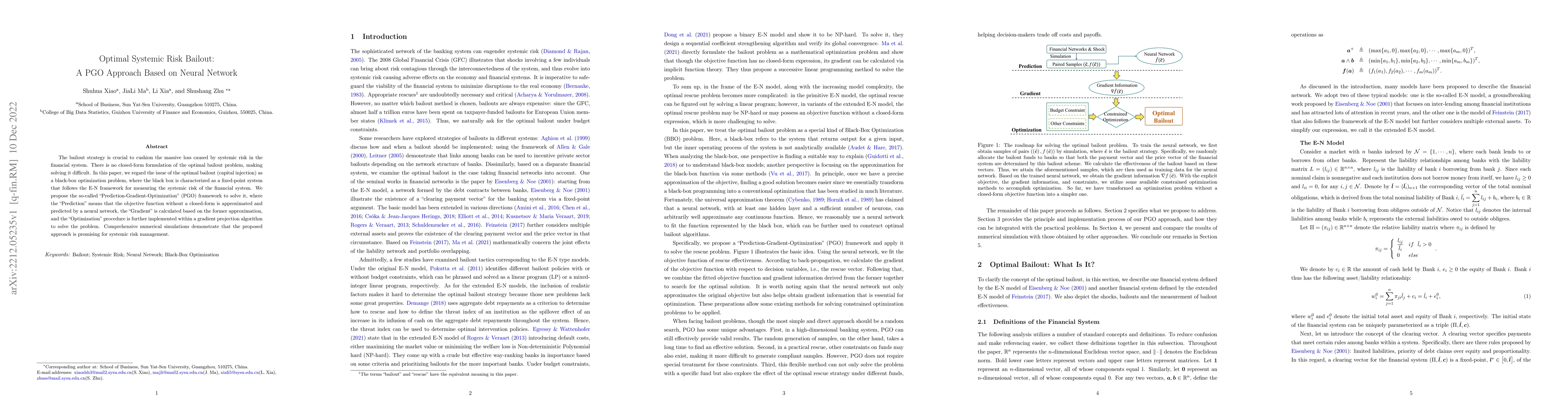

Among the reasons hindering reinforcement learning (RL) applications to real-world problems, two factors are critical: limited data and the mismatch between the testing environment (real environment...

We present a novel method to estimate the dominant eigenvalue and eigenvector pair of any non-negative real matrix via graph infection. The key idea in our technique lies in approximating the soluti...

Keeping risk under control is often more crucial than maximizing expected rewards in real-world decision-making situations, such as finance, robotics, autonomous driving, etc. The most natural choic...

This paper studies the risk-averse mean-variance optimization in infinite-horizon discounted Markov decision processes (MDPs). The involved variance metric concerns reward variability during the who...

Most of reinforcement learning algorithms optimize the discounted criterion which is beneficial to accelerate the convergence and reduce the variance of estimates. Although the discounted criterion ...

Semi-Markov model is one of the most general models for stochastic dynamic systems. This paper deals with a two-person zero-sum game for semi-Markov processes. We focus on the expected discounted pa...

We study a finite-horizon two-person zero-sum risk-sensitive stochastic game for continuous-time Markov chains and Borel state and action spaces, in which payoff rates, transition rates and terminal...

This paper investigates the optimization problem of an infinite stage discrete time Markov decision process (MDP) with a long-run average metric considering both mean and variance of rewards togethe...

For a Markov decision process with countably infinite states, the optimal value may not be achievable in the set of stationary policies. In this paper, we study the existence conditions of an optima...

The option framework has shown great promise by automatically extracting temporally-extended sub-tasks from a long-horizon task. Methods have been proposed for concurrently learning low-level intra-...

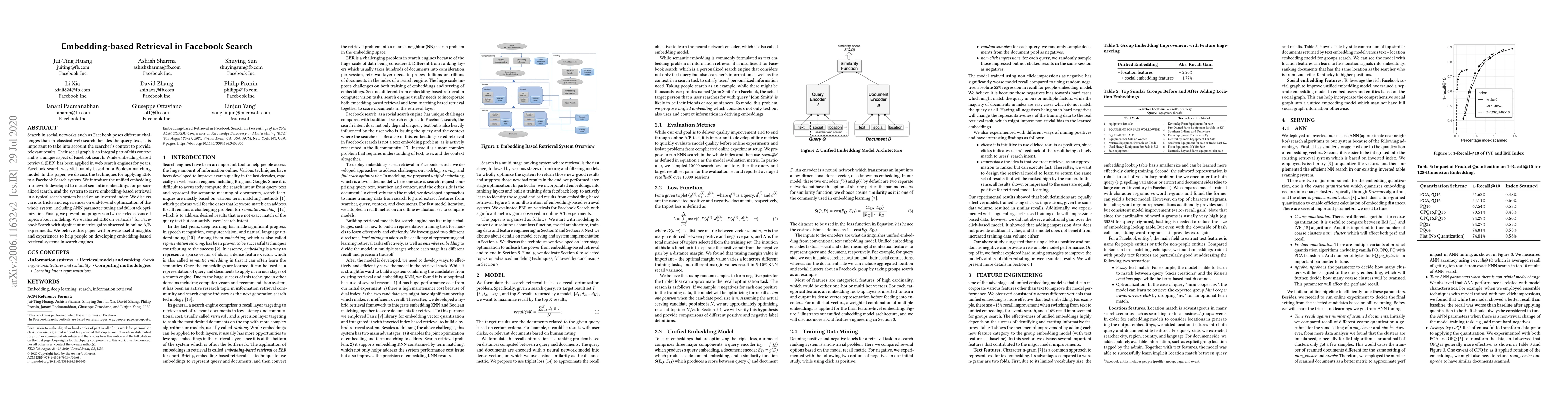

Search in social networks such as Facebook poses different challenges than in classical web search: besides the query text, it is important to take into account the searcher's context to provide rel...

Markov decision processes (MDPs) in queues and networks have been an interesting topic in many practical areas since the 1960s. This paper provides a detailed overview on this topic and tracks the e...

In this paper, we use a Markov decision process to find optimal asynchronous policy of an energy-efficient data center with two groups of heterogeneous servers, a finite buffer, and a fast setup pro...

We study a long-run mean-variance team stochastic game (MV-TSG), where each agent shares a common mean-variance objective for the system and takes actions independently to maximize it. MV-TSG has two ...

Value-at-risk (VaR), also known as quantile, is a crucial risk measure in finance and other fields. However, optimizing VaR metrics in Markov decision processes (MDPs) is challenging because VaR is no...

In this paper, we study a subclass of n-player stochastic games, in which each player has their own internal state controlled only by their own action and their objective is a common goal called team ...

Multi-period mean-variance optimization is a long-standing problem, caused by the failure of dynamic programming principle. This paper studies the mean-variance optimization in a setting of finite-hor...

This paper studies partially observable two-person zero-sum semi-Markov games under a probability criterion, in which the system state may not be completely observed. It focuses on the probability tha...

Sharpe ratio (also known as reward-to-variability ratio) is a widely-used metric in finance, which measures the additional return at the cost of per unit of increased risk (standard deviation of retur...

Federated Learning (FL) preserves privacy by keeping raw data local, yet Gradient Inversion Attacks (GIAs) pose significant threats. In FedAVG multi-step scenarios, attackers observe only aggregated g...

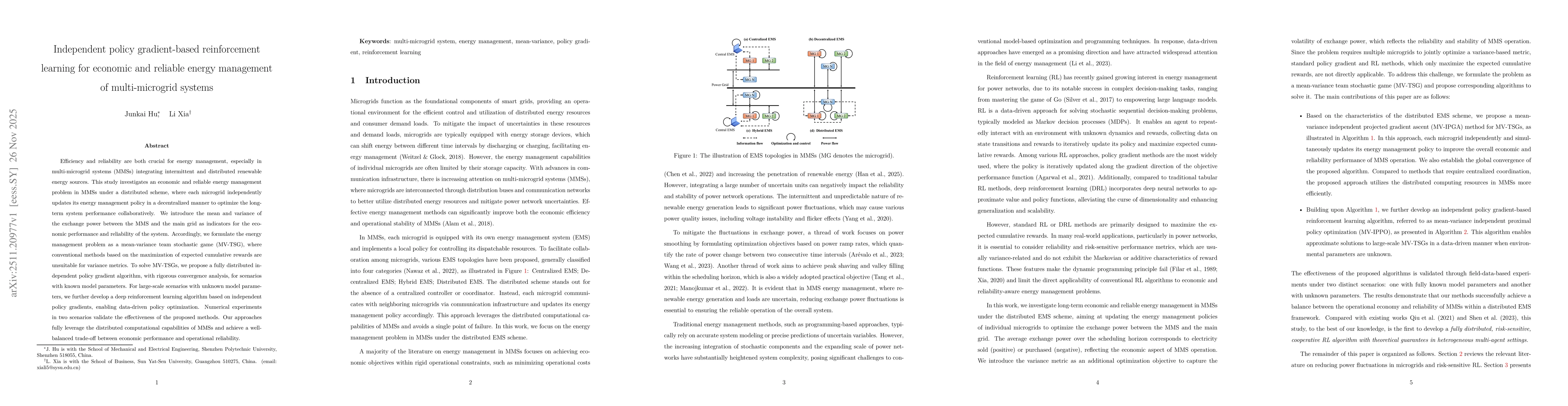

Efficiency and reliability are both crucial for energy management, especially in multi-microgrid systems (MMSs) integrating intermittent and distributed renewable energy sources. This study investigat...

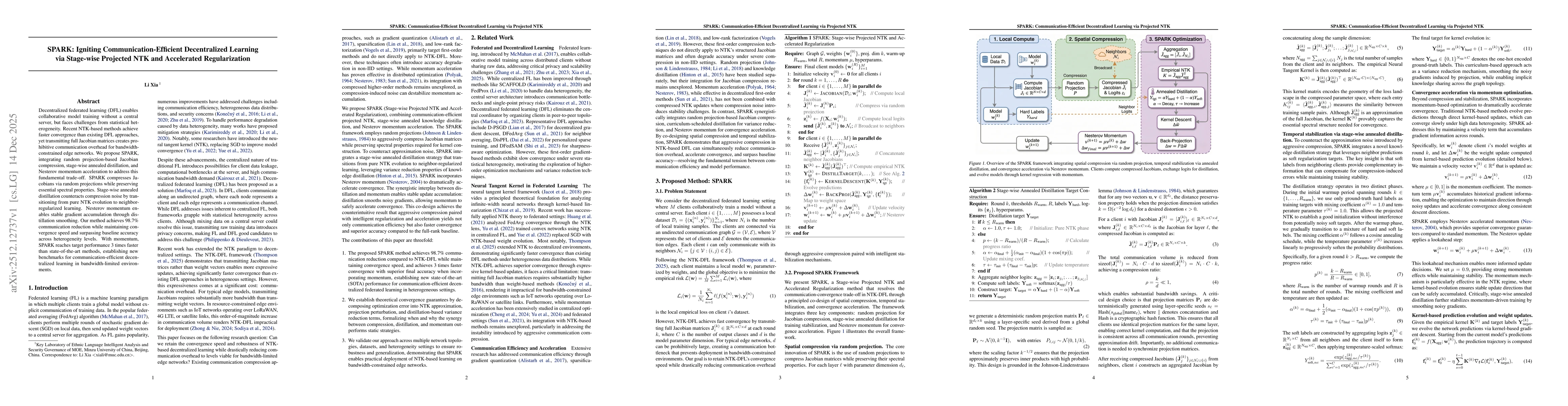

Decentralized federated learning (DFL) faces critical challenges from statistical heterogeneity and communication overhead. While NTK-based methods achieve faster convergence, transmitting full Jacobi...

Based on the 2000–2023 China High-Resolution Air Pollution (CHAP) near-surface air pollutant dataset, wintertime atmospheric pollution events in the cities along the northern slope of the Tianshan Mou...

Conditional value-at-risk (CVaR) is a prominent risk measure in financial engineering, energy systems, and supply chain management. In these domains, Markov decision processes (MDPs) with a long-run C...

Scientific discovery saturates when new hypotheses cease to provide independent information, even if the nominal hypothesis space remains large. We study hybrid discovery systems that combine structur...