Academic Profile

Statistics

Similar Authors

Papers on arXiv

Modern evolvements of the technologies have been leading to a profound influence on the financial market. The introduction of constituents like Exchange-Traded Funds, and the wide-use of advanced te...

This paper builds the clustering model of measures of market microstructure features which are popular in predicting stock returns. In a 10-second time-frequency, we study the clustering structure o...

The paper proposes a new asset pricing model -- the News Embedding UMAP Selection (NEUS) model, to explain and predict the stock returns based on the financial news. Using a combination of various m...

The purpose of this paper is to test the time-invariance of the beta coefficients estimated by the Adaptive Multi-Factor (AMF) model. The AMF model is implied by the generalized arbitrage pricing th...

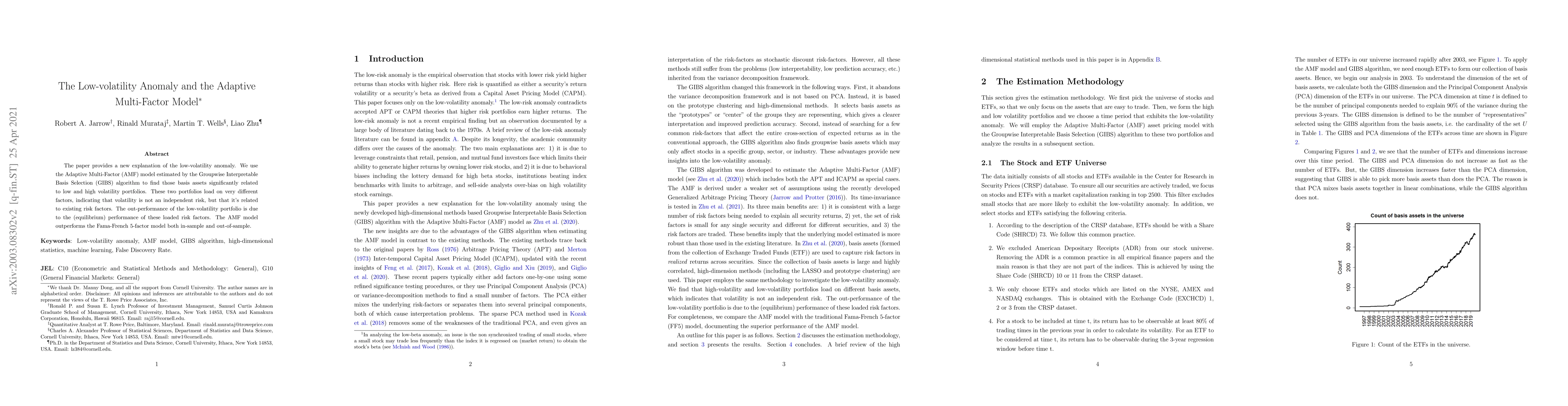

The paper provides a new explanation of the low-volatility anomaly. We use the Adaptive Multi-Factor (AMF) model estimated by the Groupwise Interpretable Basis Selection (GIBS) algorithm to find tho...

The paper proposes a new algorithm for the high-dimensional financial data -- the Groupwise Interpretable Basis Selection (GIBS) algorithm, to estimate a new Adaptive Multi-Factor (AMF) asset pricin...

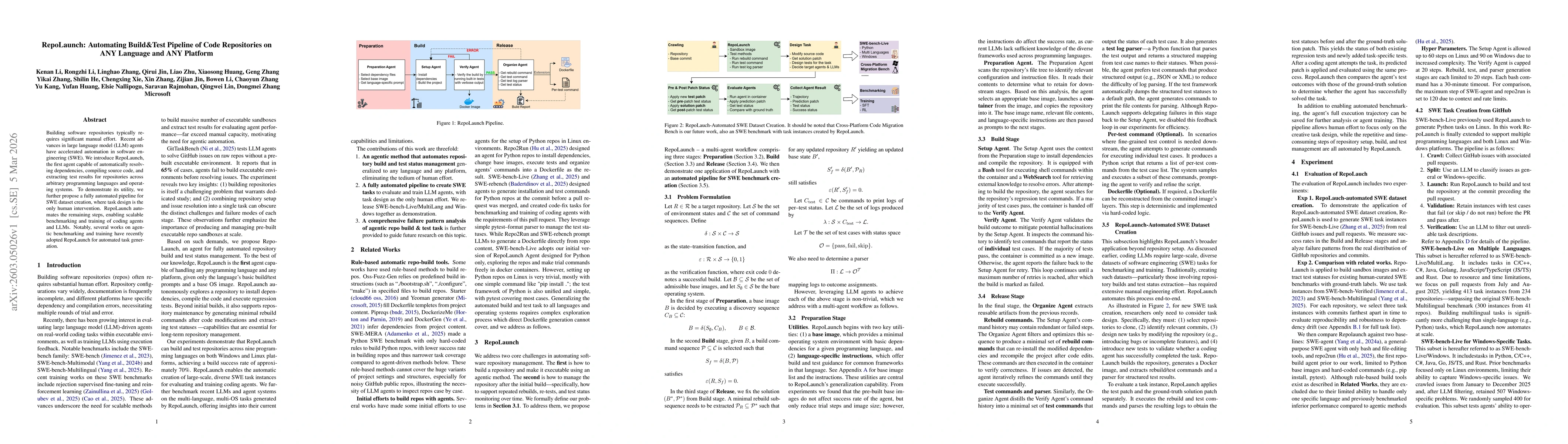

Building software repositories typically requires significant manual effort. Recent advances in large language model (LLM) agents have accelerated automation in software engineering (SWE). We introduc...

Recent advances in language model (LM) agents have significantly improved automated software engineering (SWE). Prior work has proposed various agentic workflows and training strategies as well as ana...