Academic Profile

Statistics

Similar Authors

Papers on arXiv

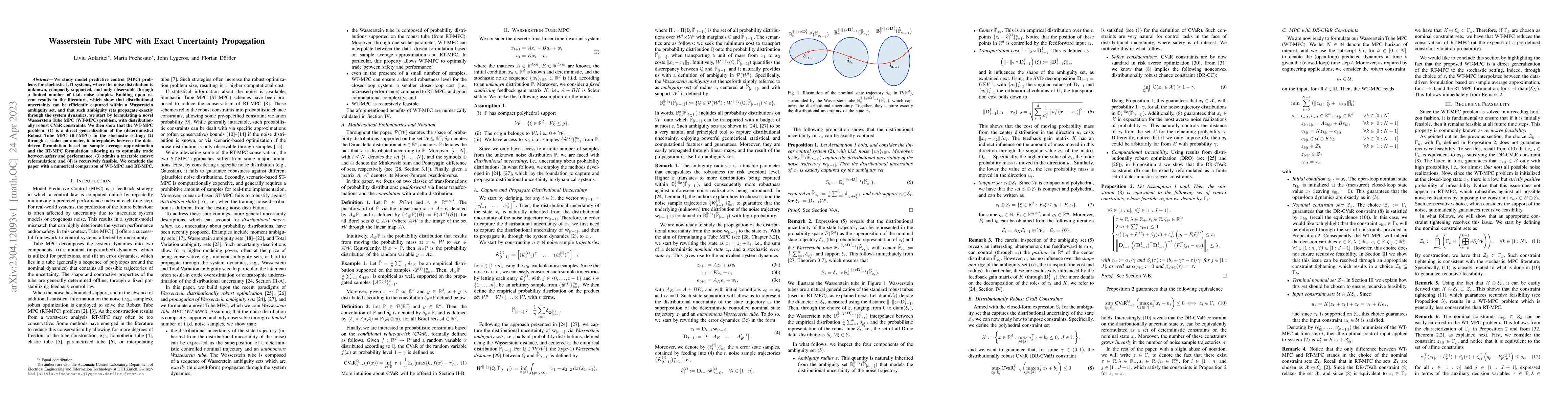

We study model predictive control (MPC) problems for stochastic LTI systems, where the noise distribution is unknown, compactly supported, and only observable through a limited number of i.i.d. nois...

We study stochastic dynamical systems in settings where only partial statistical information about the noise is available, e.g., in the form of a limited number of noise realizations. Such systems a...

We study optimal transport-based distributionally robust optimization problems where a fictitious adversary, often envisioned as nature, can choose the distribution of the uncertain problem paramete...

Wasserstein distributionally robust optimization has recently emerged as a powerful framework for robust estimation, enjoying good out-of-sample performance guarantees, well-understood regularizatio...

This paper addresses the limitations of standard uncertainty models, e.g., robust (norm-bounded) and stochastic (one fixed distribution, e.g., Gaussian), and proposes to model uncertainty via Optima...

Conformal prediction provides a powerful framework for constructing prediction intervals with finite-sample guarantees, yet its robustness under distribution shifts remains a significant challenge. Th...

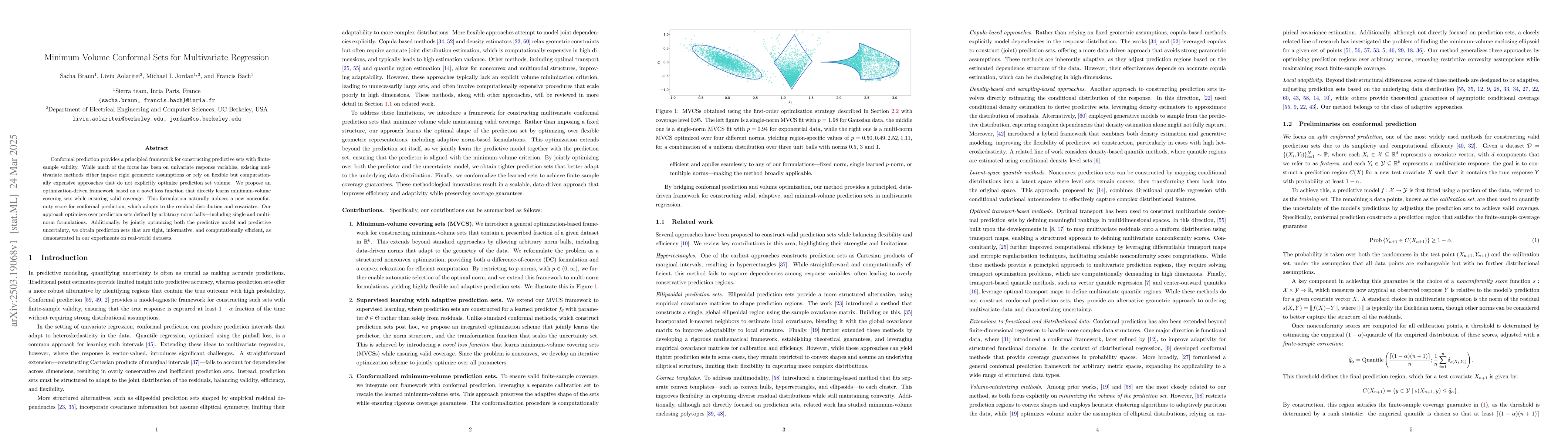

Conformal prediction provides a principled framework for constructing predictive sets with finite-sample validity. While much of the focus has been on univariate response variables, existing multivari...

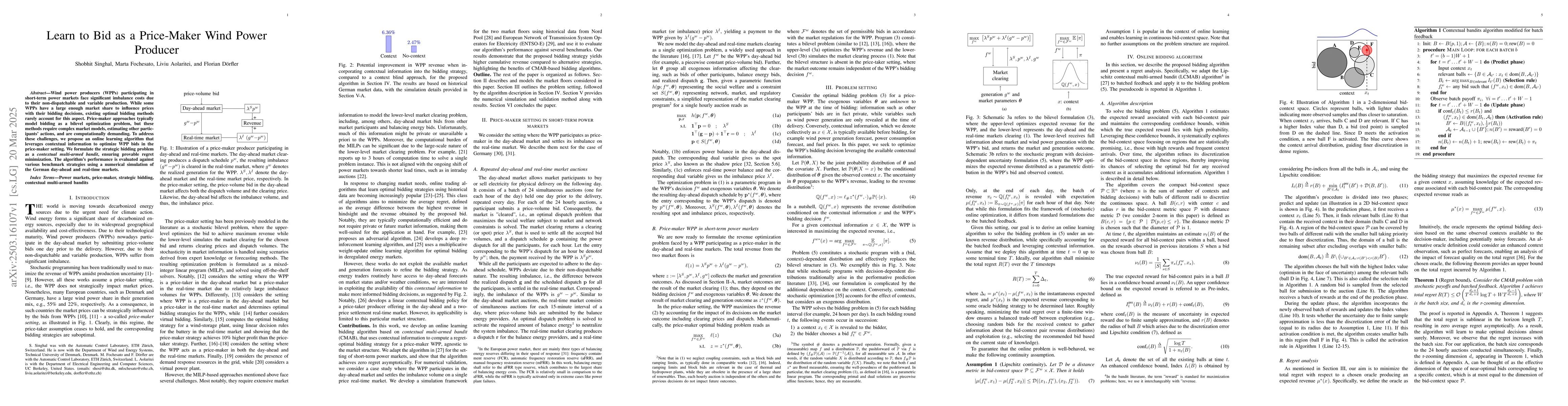

Wind power producers (WPPs) participating in short-term power markets face significant imbalance costs due to their non-dispatchable and variable production. While some WPPs have a large enough market...

Importance Sampling (IS) is a widely used variance reduction technique for enhancing the efficiency of Monte Carlo methods, particularly in rare-event simulation and related applications. Despite its ...

We revisit the problem of mean estimation on $\ell_p$ balls under additive Gaussian noise. When $p$ is strictly less than $2$, it is well understood that rate-optimal estimators must be nonlinear in t...

Conformal prediction offers a distribution-free framework for constructing prediction sets with coverage guarantees. In practice, multiple valid conformal prediction sets may be available, arising fro...

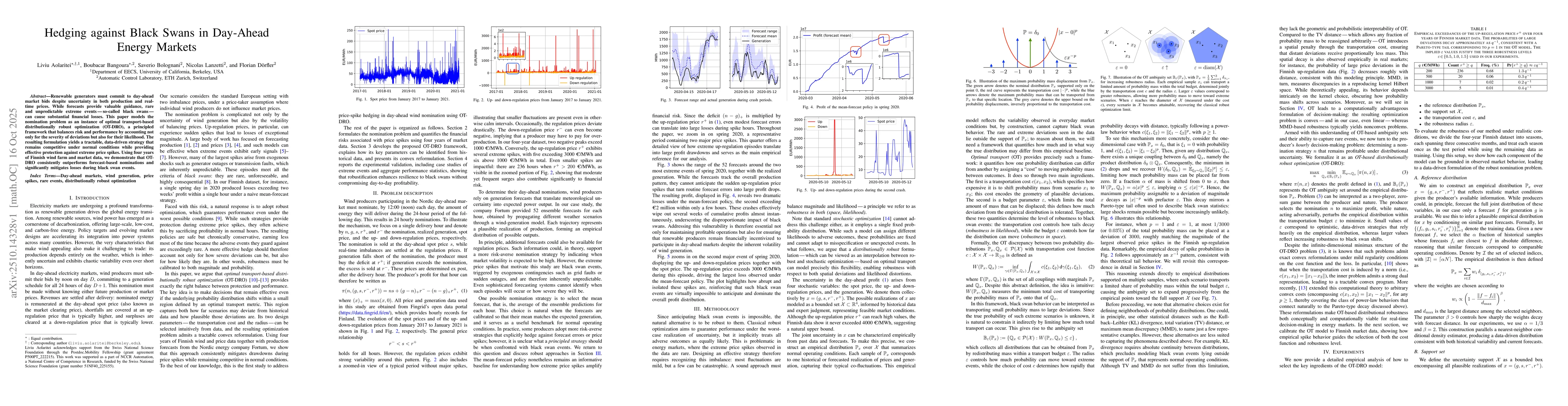

Renewable generators must commit to day-ahead market bids despite uncertainty in both production and real-time prices. While forecasts provide valuable guidance, rare and unpredictable extreme events ...

We study stopping rules for stochastic gradient descent (SGD) for convex optimization from the perspective of anytime-valid confidence sequences. Classical analyses of SGD provide convergence guarante...

We introduce a diffusion-based uncertainty model for robust optimization on directed graphs, in which perturbations of edge weights propagate along adjacent edges and satisfy conservation constraints ...