Academic Profile

Statistics

Similar Authors

Papers on arXiv

In this paper, by using matrix product codes, several classes of new quantum codes are obtained. Moreover, some of them have better parameters than the previous quantum codes available.

Multivariate long-term time series forecasting is of great application across many domains, such as energy consumption and weather forecasting. With the development of transformer-based methods, the...

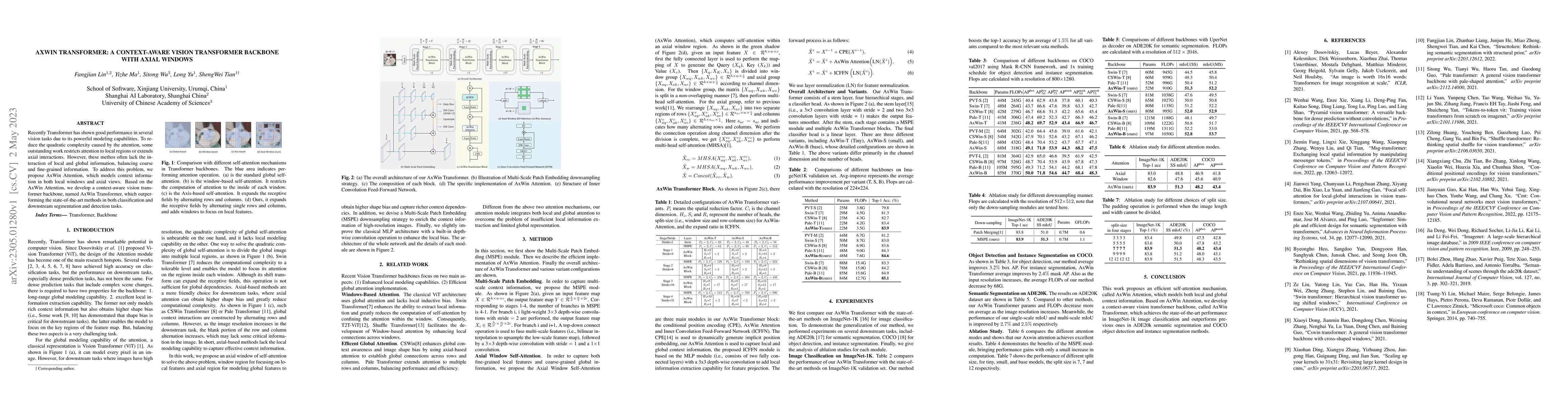

Recently Transformer has shown good performance in several vision tasks due to its powerful modeling capabilities. To reduce the quadratic complexity caused by the attention, some outstanding work r...

The lightweight MLP-based decoder has become increasingly promising for semantic segmentation. However, the channel-wise MLP cannot expand the receptive fields, lacking the context modeling capacity...

We consider the extreme eigenvalues of the sample covariance matrix $Q=YY^*$ under the generalized elliptical model that $Y=\Sigma^{1/2}XD.$ Here $\Sigma$ is a bounded $p \times p$ positive definite...

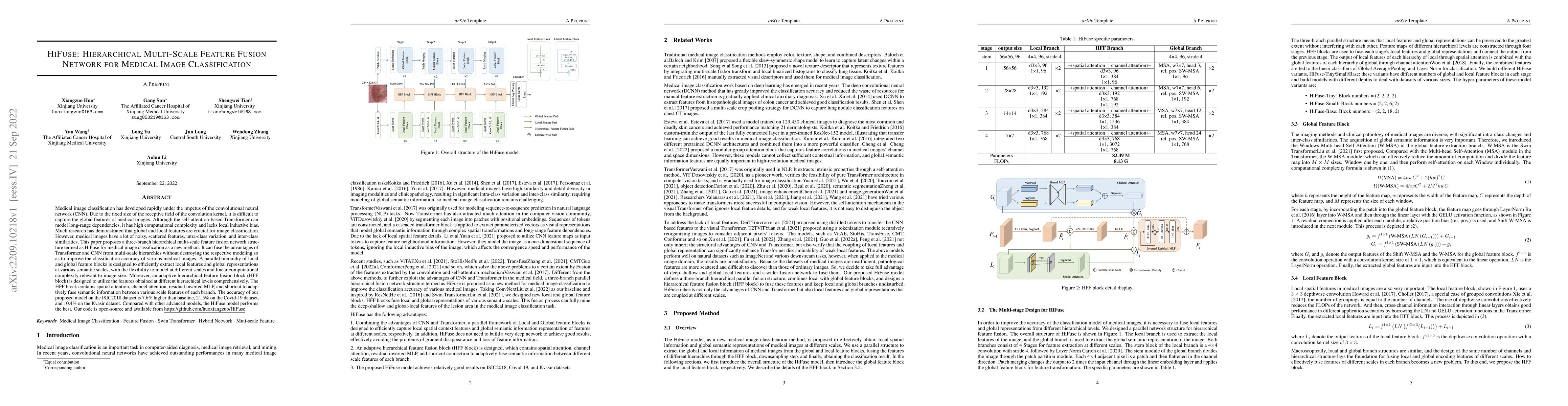

Medical image classification has developed rapidly under the impetus of the convolutional neural network (CNN). Due to the fixed size of the receptive field of the convolution kernel, it is difficul...

Translation-based knowledge graph embedding has been one of the most important branches for knowledge representation learning since TransE came out. Although many translation-based approaches have a...

This paper introduces a matrix quantile factor model for matrix-valued data with a low-rank structure. We estimate the row and column factor spaces via minimizing the empirical check loss function o...

In this article, we first propose generalized row/column matrix Kendall's tau for matrix-variate observations that are ubiquitous in areas such as finance and medical imaging. For a random matrix fo...

This paper studies the impact of bootstrap procedure on the eigenvalue distributions of the sample covariance matrix under a high-dimensional factor structure. We provide asymptotic distributions fo...

This paper proposes a novel methodology for the online detection of changepoints in the factor structure of large matrix time series. Our approach is based on the well-known fact that, in the presen...

In this article, we study large-dimensional matrix factor models and estimate the factor loading matrices and factor score matrix by minimizing square loss function. Interestingly, the resultant est...

This paper investigates the issue of determining the dimensions of row and column factor spaces in matrix-valued data. Exploiting the eigen-gap in the spectrum of sample second moment matrices of th...

Kronecker product covariance structure provides an efficient way to modeling the inter-correlations of matrix-variate data. In this paper, we propose testing statistics for Kronecker product covaria...

A general three-dimensional (3D) non-stationary massive multiple-input multiple-output (MIMO) geometry-based stochastic model (GBSM) for the sixth generation (6G) communication systems is proposed i...

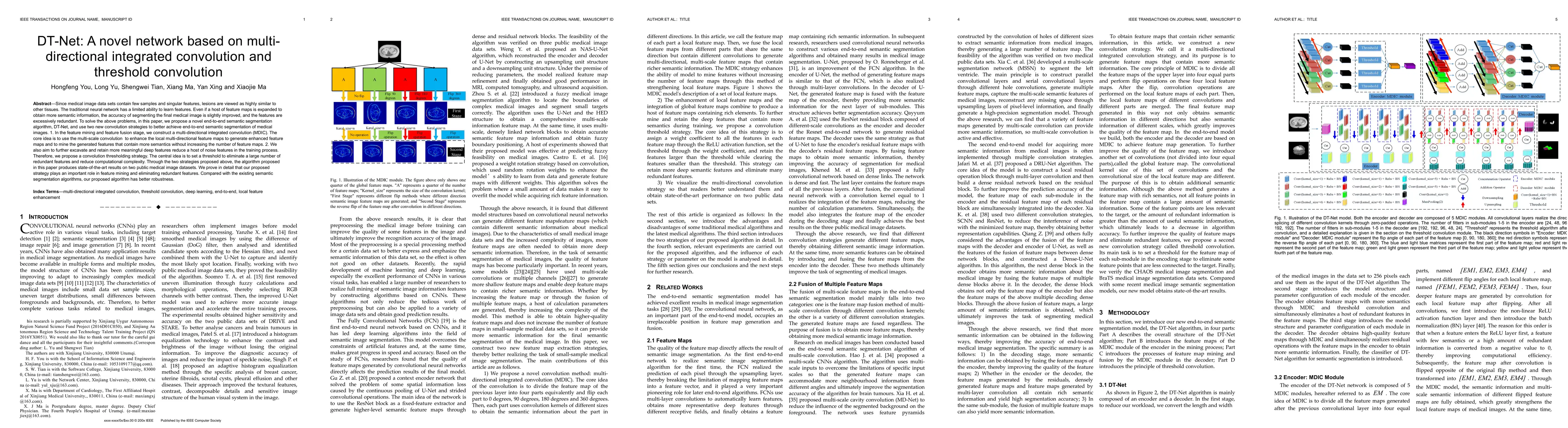

Since medical image data sets contain few samples and singular features, lesions are viewed as highly similar to other tissues. The traditional neural network has a limited ability to learn features...

To better retain the deep features of an image and solve the sparsity problem of the end-to-end segmentation model, we propose a new deep convolutional network model for medical image pixel segmenta...

In this study, we propose a projection estimation method for large-dimensional matrix factor models with cross-sectionally spiked eigenvalues. By projecting the observation matrix onto the row or co...

Network structure is growing popular for capturing the intrinsic relationship between large-scale variables. In the paper we propose to improve the estimation accuracy for large-dimensional factor m...

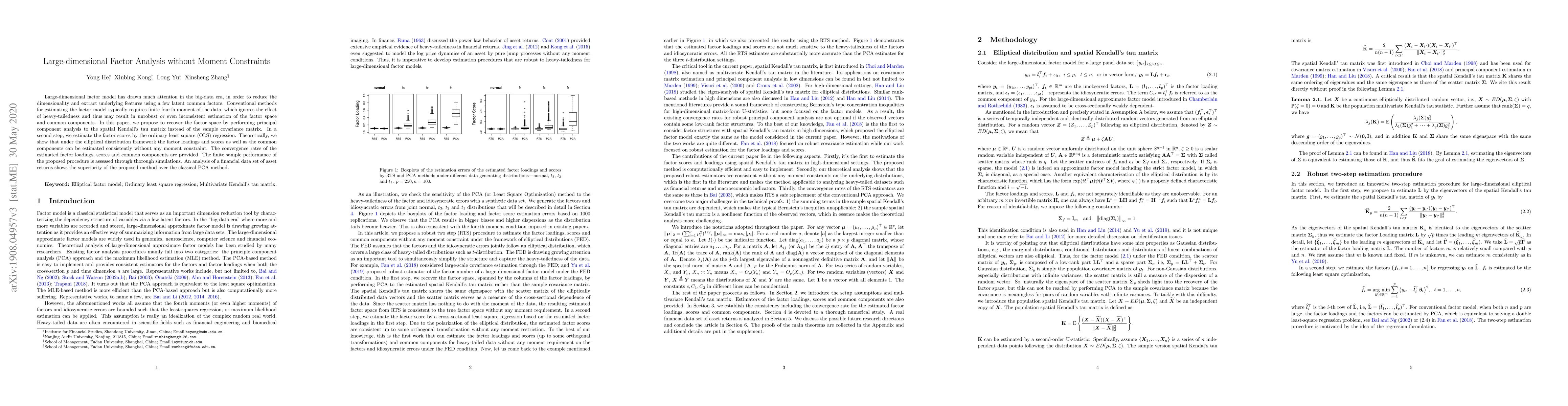

Large-dimensional factor model has drawn much attention in the big-data era, in order to reduce the dimensionality and extract underlying features using a few latent common factors. Conventional met...

Multimodal Large Language Models (MLLMs) are of great application across many domains, such as multimodal understanding and generation. With the development of diffusion models (DM) and unified MLLMs,...

Chamfer Distance (CD) comprises two components that can evaluate the global distribution and local performance of generated point clouds, making it widely utilized as a similarity measure between gene...

The performance of image generation has been significantly improved in recent years. However, the study of image screening is rare and its performance with Multimodal Large Language Models (MLLMs) is ...

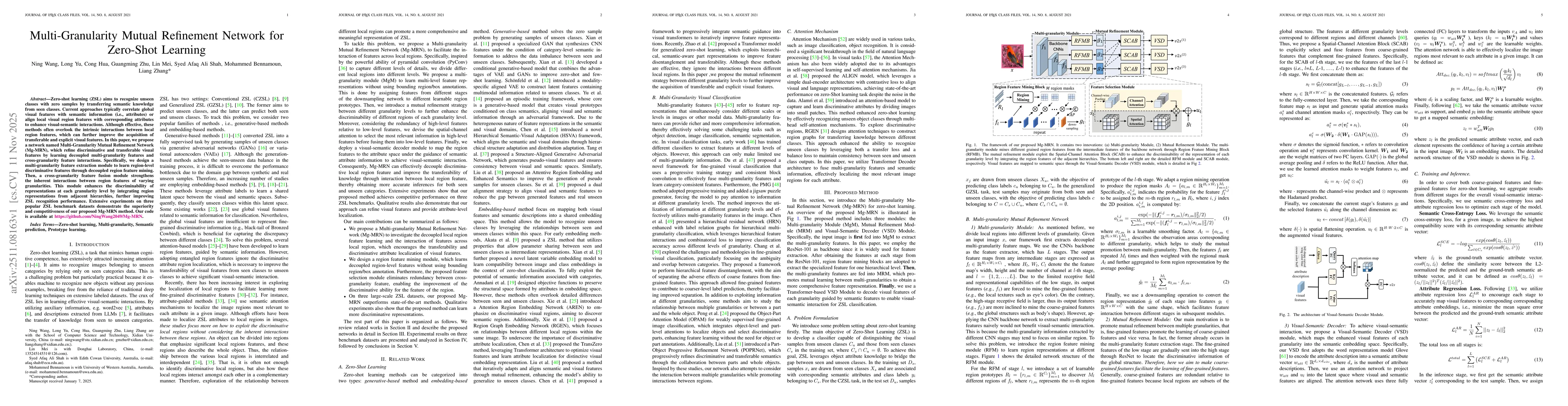

Zero-shot learning (ZSL) aims to recognize unseen classes with zero samples by transferring semantic knowledge from seen classes. Current approaches typically correlate global visual features with sem...

Existing point cloud completion methods struggle to balance high-quality reconstruction with computational efficiency. To address this, we propose PPC-MT, a novel parallel framework for point cloud co...

We adopt the canonical polyadic (CP) decomposition to model high-dimensional tensor time series. Our primary goal is to identify and estimate the factor loadings in the CP decomposition. We propose a ...