Academic Profile

Statistics

Similar Authors

Papers on arXiv

We revisit the generalized hyperbolic (GH) distribution and its nested models. These include widely used parametric choices like the multivariate normal, skew-t, Laplace, and several others. We also...

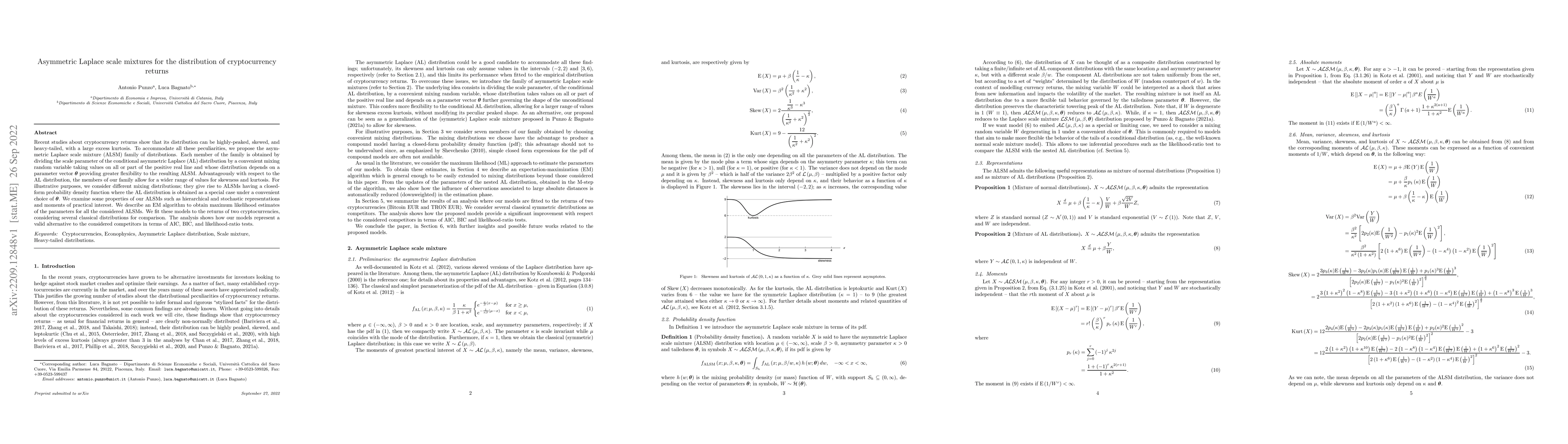

Recent studies about cryptocurrency returns show that its distribution can be highly-peaked, skewed, and heavy-tailed, with a large excess kurtosis. To accommodate all these peculiarities, we propos...

This paper introduces the multivariate tail-inflated normal (MTIN) distribution, an elliptical heavy-tails generalization of the multivariate normal (MN). The MTIN belongs to the family of MN scale ...

Many statistical problems involve the estimation of a $\left(d\times d\right)$ orthogonal matrix $\textbf{Q}$. Such an estimation is often challenging due to the orthonormality constraints on $\text...