Academic Profile

Statistics

Similar Authors

Papers on arXiv

Spatial birth-and-death processes with time dependent rates are obtained as solutions to certain stochastic equations. The existence, uniqueness, uniqueness in law and the strong Markov property of ...

We prove that under certain general conditions on the birth and death rates the Lebesgue-Poisson measure is a maximal irreducibility measure for the spatial birth-and-death process.

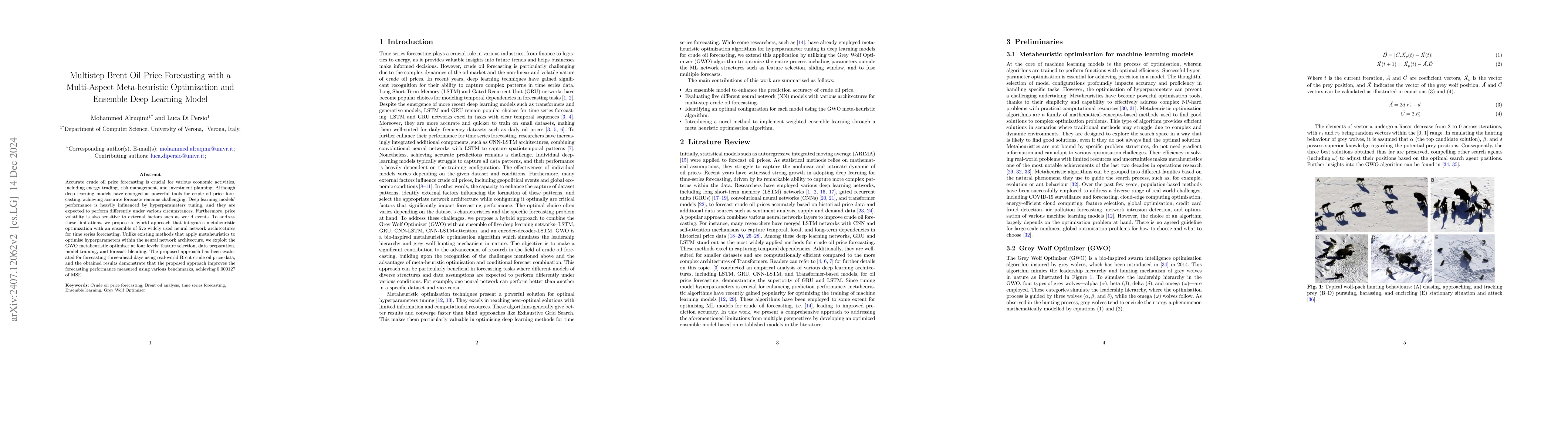

Accurate crude oil price forecasting is crucial for various economic activities, including energy trading, risk management, and investment planning. Although deep learning models have emerged as power...

Despite numerous research efforts in applying deep learning to time series forecasting, achieving high accuracy in multi-step predictions for volatile time series like crude oil prices remains a signi...

This article presents an innovative approach to integrating port-Hamiltonian systems with neural network architectures, transitioning from deterministic to stochastic models. The study presents nove...

We study a general class of interacting particle systems over a countable state space $V$ where on each site $x \in V$ the particle mass $\eta(x) \geq 0$ follows a stochastic differential equation. ...

In this article, we analyse the existence of an optimal feedback controller of stochastic optimal control problems governed by SDEs which have the control in the diffusion part. To this end, we cons...

We study classical continuous systems with singular distributions of velocities. These distributions are given by Radon measures with the infinite mass. Positions of particles, in such systems, are ...

We consider a generalization of classical results of Freidlin and Wentzell to the case of time dependent dissipative drifts. We show the convergence of diffusions with multiplicative noise in the ze...

We introduce a framework that allows to employ (non-negative) measure-valued processes for energy market modeling, in particular for electricity and gas futures. Interpreting the process' spatial st...

We consider a system of Forward Backward Stochastic Differential Equations (FBSDEs), with time delayed generator and driven by L\`evy-type noise. We establish a non linear Feynman Kac representation...

We study stochastic differential equations(SDEs) with a small perturbation parameter. Under the dissipative condition on the drift coefficient and the local Lipschitz condition on the drift and diff...

We analyze the Master Equation and the convergence problem within Mean Field Games theory considering a bounded domain with homogeneous Dirichlet conditions. This framework characterizes N-players d...

We consider the continuous-time frog model on $\mathbb{Z}$. At time $t = 0$, there are $\eta (x)$ particles at $x\in \mathbb{Z}$, each of which is represented by a random variable. In particular, $(...

The present work address the problem of energy shaping for stochastic port-Hamiltonian system. Energy shaping is a powerful technique that allows to systematically find feedback law to shape the Ham...

In this paper, we derive a representation for the value process associated to the solutions of FBSDEs in a jump-diffusion setting under multiple probability measures. Motivated by concrete financial...

In this paper we estimate the minimal controllability time for a class of non-linear control systems with a bounded convex state constraint. An explicit expression is given for the controllability t...

We prove the existence and uniqueness of the solution of a BSDE with time-delayed generators in the small delay setting (or equivalently small Lipschitz constant), which employs the Stieltjes integr...

The aim of this work is to demonstrate that the continuous-time frog model can spread arbitrary fast. The set of sites visited by an active particle can become infinite in a finite time.

We consider the existence and first order conditions of optimality for a stochastic optimal control problem inspired by the celebrated FitzHugh-Nagumo model, with nonlinear diffusion term, perturbed...

We consider a one-dimensional discrete-space birth process with a bounded number of particle per site. Under the assumptions of the finite range of interaction, translation invariance, and non-degen...

The present paper is devoted to the study of a bank salvage model with finite time horizon and subjected to stochastic impulse controls. In our model, the bank's default time is a completely inacces...

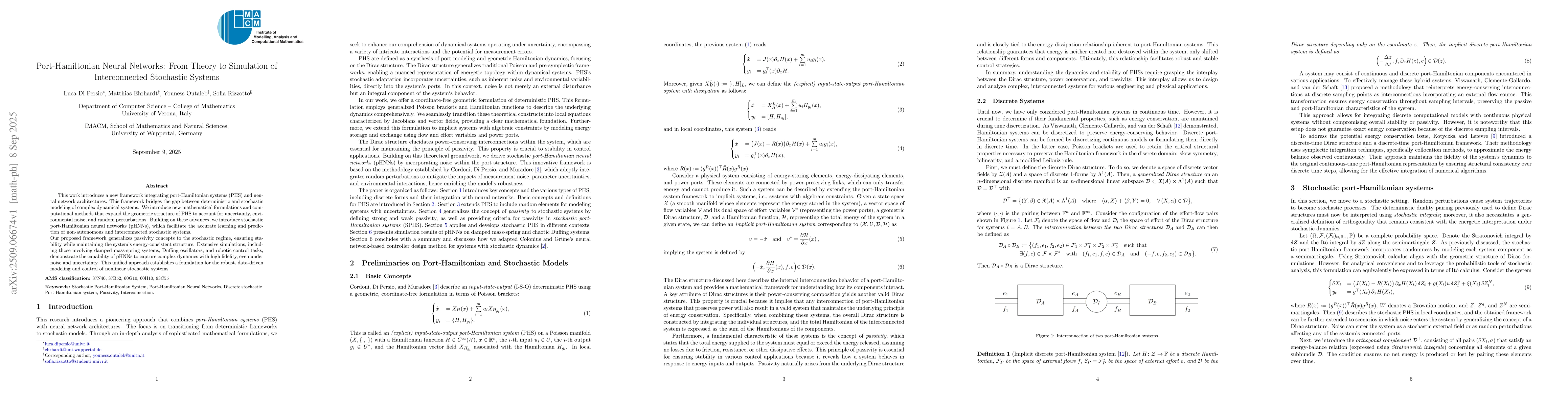

In the present work we formally extend the theory of port-Hamiltonian systems to include random perturbations. In particular, suitably choosing the space of flow and effort variables we will show ho...

We consider the speed of propagation of a {continuous-time continuous-space} branching random walk with the additional restriction that the birth rate at any spatial point cannot exceed $1$. The dis...

In a day-ahead market, energy buyers and sellers submit their bids for a particular future time, including the amount of energy they wish to buy or sell and the price they are prepared to pay or recei...

This paper investigates the optimal control problem for a class of parabolic equations where the diffusion coefficient is influenced by a control function acting nonlocally. Specifically, we consider ...

We consider a gas whose each particle is characterised by a pair $(x,v_x)$ with the position $x\in \mathbb R^d$ and the velocity $v_x\in \mathbb R^d_0= \mathbb R^d\setminus \{0\}$. We define Gibbs mea...

This work introduces a new framework integrating port-Hamiltonian systems (PHS) and neural network architectures. This framework bridges the gap between deterministic and stochastic modeling of comple...

This paper investigates an optimal integration of deep learning with financial models for robust asset price forecasting. Specifically, we developed a hybrid framework combining a Long Short-Term Memo...

We study a system of Forward-Backward Stochastic Differential Equations (FBSDEs) with time-delayed generators. The forward process includes a reflection component expressed via a Stieltjes integral, w...

Stochastic port-Hamiltonian systems represent open dynamical systems with dissipation, inputs, and stochastic forcing in an energy based form. We introduce stochastic port-Hamiltonian neural networks,...

We present a one-month-ahead conditional probabilistic framework for wind-power forecasting at ten-minute resolution. Monthly Weibull shape and scale parameters are estimated from serially dependent S...

We study a mean field game (MFG) of state and control with state dynamics described by stochastic differential equations driven by both idiosyncratic and common noise, and subject to the constraint th...

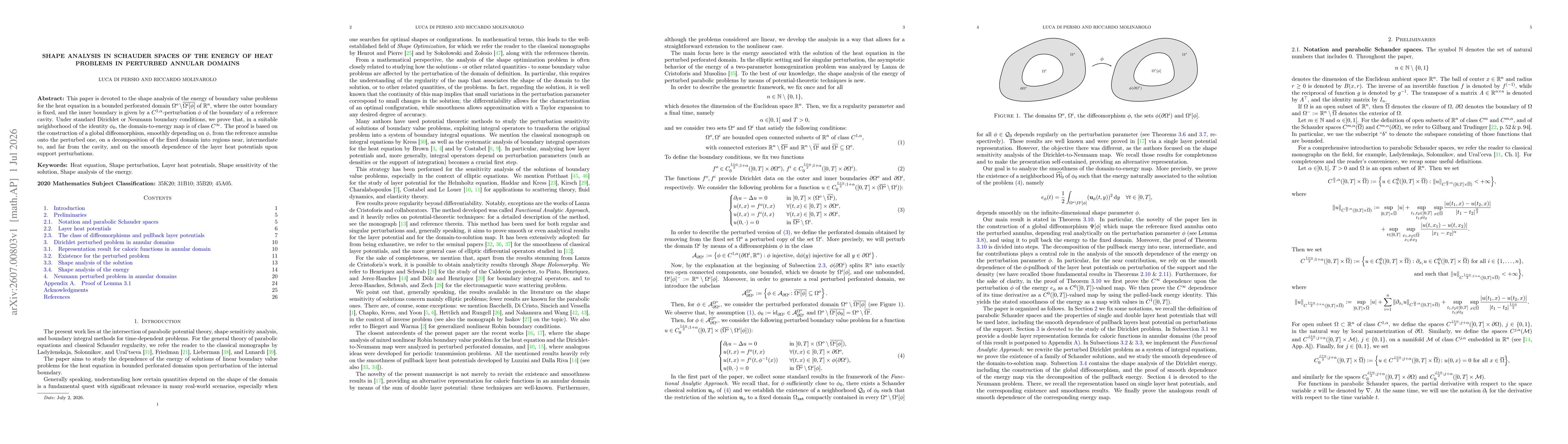

This paper is devoted to the shape analysis of the energy of boundary value problems for the heat equation in a bounded perforated domain $Ω^o \setminus \overline{Ω^i[φ]}$ of $\mathbb{R}^n$, where the...